Overall and Core CPI Both Rise 0.6 Percent in July as Price Reversals Continue

Rental inflation appears to be slowing, especially in high-priced cities.

The overall Consumer Price Index (CPI) rose 0.6 percent in July, the same as the rate in June. The core CPI rose 0.6 percent in July after rising 0.2 percent in June. Over the last year the indexes are up 1.0 percent and 1.6 percent, respectively.

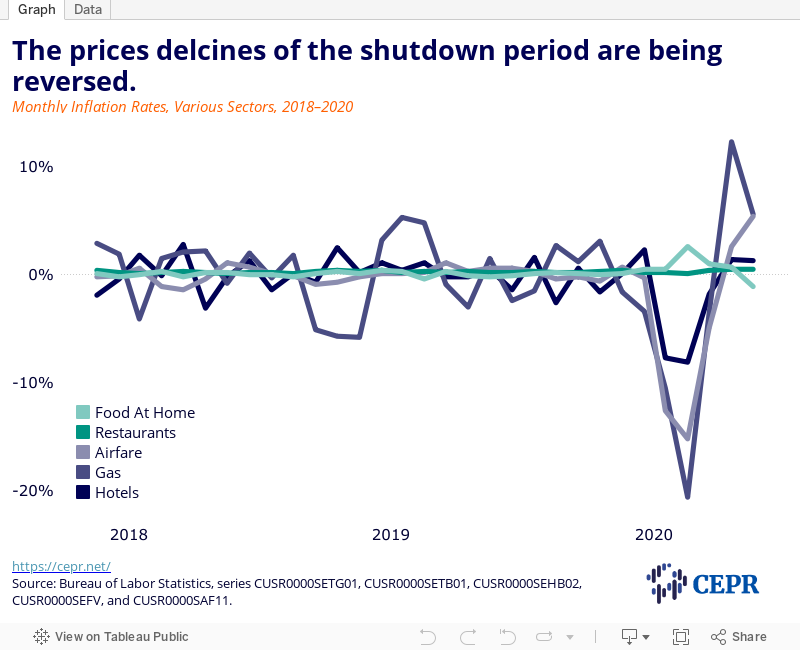

The inflation of the last two months is overwhelmingly a story of bounce-back with sharp price increases in these months reversing large price declines in the period of shutdown. To a lesser extent, higher prices in some areas likely reflect efforts to pass on pandemic-related costs (e.g., reduced capacity in restaurants or airplanes). These costs will largely disappear if the pandemic is brought under control.

Gas prices are probably the clearest example of this pattern. They rose 5.6 percent in July after rising 12.3 percent in June. This follows a cumulative price decline of 33.8 percent from January to May. Over the last year gas prices are still down by 20.3 percent.

In the core index, apparel prices are up 1.1 percent in July after rising 1.7 percent in June. They had fallen 8.8 percent from February to May. They are now down by 6.4percent over the last year. Airfares rose by 2.6 percent and 5.4 percent in June and July, respectively. This followed a price decline of 29.5 percent in the prior three months.

Auto insurance prices rose 9.3 percent in July following a 5.1 percent rise in June. This is after falling 14.9 percent from February to May. The index is down 1.9 percent over the last year.

The CPI auto insurance index (unlike the one used in the personal consumption expenditure deflator) is a gross spending index. It captures what people pay out for their insurance, without netting out claims. Not surprisingly, this gross index fell sharply in the shutdown period as insurers gave rebates due to the fact that people were driving much less and therefore having fewer accidents. The rise in the last two months is the ending of these rebates. The insurance index accounts for almost 1.9 percent of the core CPI.

Restaurant prices rose 0.5 percent in July after rising 0.4 percent and 0.5 percent in the prior two months. Before the pandemic, restaurant prices had been rising 1.0–1.5 percent more rapidly than the price of food at home, reflecting rising wages in the sector. This was reversed during the shutdown period. In March, restaurant prices rose 0.2 percent, while at-home food prices rose 0.5 percent. In April the respective increases were 0.1 percent and 2.6 percent, and in May 0.4 percent and 1.0 percent. The story was sharply reversed in July, as the 0.5 percent rise in restaurant prices went along with a drop of 1.1 percent in the price of food at home. Going forward, restaurant prices are likely to again outpace food prices.

There appears to be some slowing in the rate of rental inflation, with owners’ equivalent rent rising at an annual rate of 2.4 percent, comparing the average of the last three months (May, June, July) with the prior three months (February, March, April). That is down from a rate of 2.8 percent over the last year. For the rent proper index, the increases are 2.6 percent compared to 3.1 percent.

This slowdown is most visible in areas where rents had been rising rapidly. In Los Angeles the rent proper index was rising at an annual rate of 2.5 percent over the last three months, down from 3.6 percent over the last year. In San Francisco the index has fallen at an annual rate of 3.3 percent over the last three months compared to a rise of 2.6 percent over the last year.

The high inflation of June and July is not a surprise and should not be a basis for concern about ongoing problems with inflation. It is overwhelmingly attributable to reversals of sharp price declines during the shutdown period. In addition, there are sectors that are experiencing one-time and temporary cost pressures as a result of adjustments necessary to cope with the pandemic. We may see another month or two of high inflation, but there is little reason to believe that this is the start of an upward spiral.