November 10, 2022

On the whole, this is a very positive report. Not only did the Consumer Price Index (CPI) come in slightly lower than expected, we are seeing no evidence that inflation is becoming embedded in services, as many had predicted.

Inflation in medical services (a big chunk of non-shelter services) is very much under control.

The rent indexes seem to already be picking up some of the downward trends shown in private indexes of marketed units. The rate of inflation in the CPI indices will fall further in 2023.

We have turned the corner on most supply chain items, with rapid price declines in many areas. However, we still have to wait on new vehicle prices.

The Personal Consumption Expenditures should look even better, with auto insurance having a much lower weight (rent also) and medical care having a larger one. This CPI report helps bolster the case for a pause on rate hikes.

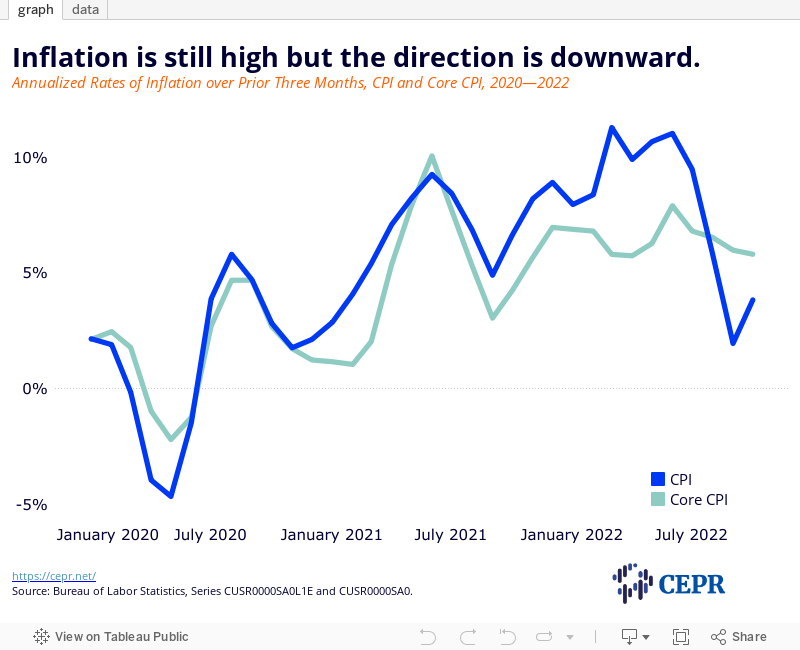

The core and overall CPI were slightly lower than expected in October. The core is 0.3 percent, and the overall is 0.4 percent; 6.3 percent and 7.7 percent year-over-year, respectively.

The medical care services index dropped 0.6 percent, driven by a 4.0 percent drop in the health insurance index.

Health care insurance has been a major driver of health care inflation, rising more than 28 percent in the year from September 2021 to 2022. The turnaround was predictable, even if not necessarily so dramatic.

Other data on the health care services index are also positive: professional medical services rose just 0.2 percent in October, now up 3.3 percent year-over-year; hospital services fell 0.2 percent in October, now up 3.4 percent year-over-year. This is very good news going forward.

Rent indexes slowed slightly, with rent proper rising 0.7 percent and owners’ equivalent rent rising 0.6 percent. Both rose 0.8 percent in September. This is very encouraging. Indexes of marketed units are now showing falling rents. The CPI lags these indices, but the general direction is clearly downward.

The car insurance index rose 1.7 percent in October, adding 0.05 percentage points to core inflation; it’s up 12.9 percent year-over-year. (This index has a far lower weight in the Personal Consumption Expenditures deflator.)

Store-bought food prices were up 0.4 percent in October, and restaurant meals were up 0.9 percent; up 12.4 percent and 8.6 percent year-over-year, respectively.

The prices of some food items are now falling. Beef prices were down 0.1 percent in October, 3.6 percent year-over-year. Milk prices fell 0.2 percent after dropping 1.3 percent in September, but are still up 14.5 percent year-over-year.

Supply chain items are finally doing a big turn. Apparel prices fell 0.7 percent in October but are up 4.1 percent year-over-year. Appliances fell 0.5 percent but are up 0.9 percent year-over-year.

Furniture prices fell 1.2 percent, up 8.3 percent year-over-year. Price declines on these items are virtually certain to continue. Imports are a large share of the market and import prices have been falling sharply in the last five months.

New vehicle prices rose 0.4 percent, up 8.4 percent year-over-year. New vehicles have still not hit the turning point. Used vehicle prices fell 2.4 percent, now up 2.0 percent year-over-year. Used vehicle price declines are virtually certain to continue.

The dogs are getting angry! Pet food prices were up 1.0 percent in October, now up 15.0 percent year-over-year.

College tuition was up 0.1 percent and childcare costs rose 0.2 percent in October, now rising 2.0 percent and 4.9 percent year-over-year, respectively.