Article • Data Bytes

Homeowners Insurance: A Big Item Missing From the Consumer Price Index

Article • Data Bytes

Since 1983, the Consumer Price Index (CPI) has used a rental equivalence measure for owner-occupied housing. This is supposed to measure the rent that could be charged if the home was rented. We can think of this as what the homeowner is paying to themselves.

It might seem a strange idea, but the prior method — measuring the increase in house prices as part of the CPI — effectively implied that homeowners were worse off if the price of their house rose by 20 percent. The logic of the rental equivalence measure is to treat owner-occupied housing as a consumption good rather than an investment good.

In keeping with this approach, the CPI excludes the cost of homeowners insurance. The logic is that the insurance is bought to protect the value of an investment good. It only includes renters’ insurance and the small portion of homeowners insurance that covers personal possessions, not the value of the structure. As a result, the weight of this insurance in the CPI is 0.29 percent, a bit less than for household cleaning products.

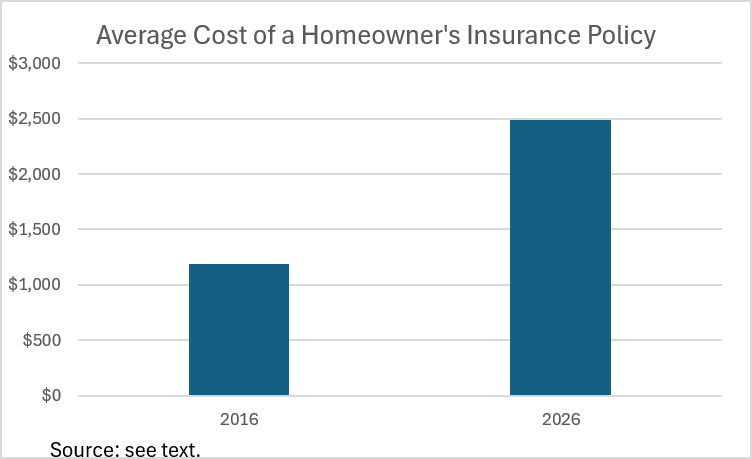

For the nearly two-thirds of households who are homeowners, insurance is a far larger and growing share of their spending. In 2016, the average cost of a homeowners insurance policy was $1,186. This had risen to $2,490 by 2026. This is an increase of 110 percent, compared to an increase in the overall CPI of 37.4 percent over this period.

The 2026 figure would be equal to a bit less than 3.0 percent of the median household income of $83,730. This is an imperfect comparison, since the median income for homeowners is higher than the overall median. Also, the average cost of an insurance policy will be higher than the median.

But the point is that for homeowners, insurance is a far higher share of their spending than is counted in the CPI, and it has been growing considerably more rapidly than the overall inflation rate. We can’t blame consumers if they don’t view this expense the way economists would like them to.

Article

Article

Article

Article

Article

Article

Article

Article