Article • Dean Baker’s Beat the Press

Land Value Taxes and Progressive Property Taxes: Two Great Taxes that Go Great Together!

Article • Dean Baker’s Beat the Press

The idea of a land value tax, a tax that only applies to the value of the land, has been floating around pretty much forever. It is most often associated with the 19th century economist and philosopher Henry George, although I suspect the history goes back further. The basic idea is to tax the value of land (including minerals), rather than the buildings constructed on it. In the strong version, this would be the only tax.

The great advantage of a land value tax is that it does not create negative incentives, like most taxes. For example, an income tax can discourage people from working by taxing away part of their earnings. A property tax gives people less incentive to improve their homes. But the value of land is largely fixed, independent of the decisions of whoever owns it. Therefore, it doesn’t affect the incentives they face.

One problem with a land value tax is that it would generally be regressive. If most of the value of more expensive properties is due to the buildings and not the land, a tax that is a fixed percentage of the land price would hit low and moderate-income people harder than high-income people who live in expensive homes.

This is where a progressive property tax comes in. We can restructure existing property taxes so that they hit higher income people harder. Instead of having a flat rate for all properties, there can be a higher marginal rate for more expensive homes. For example, if the overall rate is 1 percent, the rate on the value in excess of $1 million can be 1.5 percent, and 2.0 percent on the value in excess of $2 million.

It is important to recognize that this is a marginal rate that only applies to the value above the cutoffs. That means if a house just squeaks over the $1 million threshold, say at $1,020,000, the higher tax is only paid on the $20,000, not the full $1.020,000. This person would pay an extra $100 a year in this story. A nice feature of this tax is that we already have assessed values on the books. It would only be necessary to change the rates that apply, which can easily be done on an Excel spreadsheet.

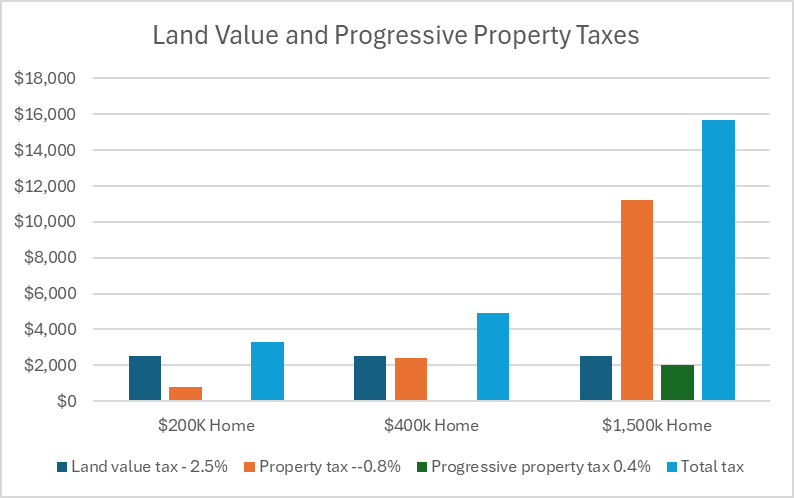

To see the dynamics, I’ll take a highly stylized example that illustrates the basic features. Let’s assume that the value of land is on average one-fifth the value of the property on the tax rolls, with the other four-fifths coming from the buildings on the land. This means that for a land value tax to produce the same revenue as the current property tax it would have to be five times as large. If the current property tax averages 1.0 percent, a land tax would have to be roughly 5 percent to produce the same revenue.

To see why this would be regressive, imagine someone has a relatively inexpensive house that is assessed at $200,000. Suppose half of this, or $100,000, is due to the value of the land. If there were a 5 percent land value tax, the homeowner would pay $5,000 in taxes on the value of their land, compared to the $2,000 tax bill they faced with a 1 percent property tax.

There is some argument for this being fair. If the person lives on a very desirable piece of land, why shouldn’t they pay a correspondingly high tax rate? They can always move to a less expensive property. But I suspect most people don’t find that logic very compelling. For this reason, in my example, I assume that the land value tax is 2.5 percent, half of what would be needed to replace a 1 percent property tax.

This tax would cost the homeowner with the inexpensive house $2,500 a year, as shown above. I have also shown a hypothetical medium-cost house with a value of $400,000 and an expensive home with a value of $1,500,000. For simplicity, I assume that the value of the land in each of the three cases is $100,000.

The next bar shows the normal property tax, which I have set at 0.8 percent. This applies to the non-land portion of the house value. For the inexpensive home, the 0.8% tax is on the $100,000 value of the home, coming to $800 a year. For the medium-priced home, it applies to the $300,000 value of the home, costing $2,400 a year. The tax is applied to $1,400,000 of housing value in the case of the expensive home, raising $11,200 a year.

The progressive portion of the property tax is straightforward. Since it only applies to the value of homes in excess of $1,000,000, the first two houses are not affected by it. The third home, with an assessed value of $1,500,000, would pay 0.4 percent of the $500,000 in excess of $1,000,000, or $2,000 with this tax rate. (I assumed the value of the land would be counted for the tax, but that is optional.)

The story from summing the three taxes is the owner of the inexpensive home would pay $3,300 in tax, considerably more than the $2,000 they would pay with a 1 percent property tax. The owner of the middle-priced house ends up paying $4,900, somewhat more than the $4,000 they pay with a 1 percent property tax. And the owner of the expensive property would pay $15,700, also somewhat more than the $15,000 they would pay with a 1 percent property tax.

As noted, these tax rates are all arbitrary; they can be made smaller or larger to hit various targets or meet some criterion of fairness. The point of the exercise is to show how these taxes can work.

Carrying the progressive property tax a step further, there can be higher marginal rates for even more expensive homes. For example, it could be 2.0 percent on the value in excess of $2 million or $2.5 million. In addition to raising money, the incentive provided by a progressive property tax is also beneficial. It discourages rich people from owning big expensive houses. The tax would be reduced by dividing it or not building such a big house in the first place. This could allow for more lower-cost housing.

States usually limit the flexibility of cities or counties in setting property tax rates, so it would require a modestly progressive state government to allow for these alternative ways to tax property. But we can at least start to get them on the table for discussion.

Article

Article

Article

Article

Article

Article

Article

Article