March 02, 2017

February 2017, Eileen Appelbaum

Testimony of Eileen Appelbaum, PhD, Senior Economist, Center for Economic and Policy Research (CEPR)

Miller Senate Building, 3rd Floor

11 Bladen St., Annapolis, MD 21411

February 28, 2017

Good afternoon. Thank you for the opportunity to testify in support of SB0605. I am Eileen Appelbaum, Senior Economist at the Center for Economic and Policy Research (CEPR). I formerly held full professor positions at Temple University in Philadelphia, PA and Rutgers University in New Brunswick, NJ. I am the coauthor of P. The book has been reviewed many times and found to be a fair and balanced account of the industry. In August 2016, it was chosen by the prestigious Academy of Management (the professional academic association for business schools and their faculty) as one of the four best books published in the two-year period 2014–2015 and was a finalist for the George R. Terry Book Award.

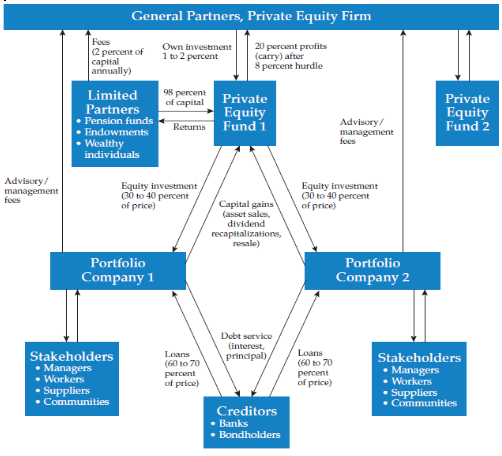

I would like to begin with a brief description of the private equity business model. A private equity firm sponsors a private equity fund and appoints one of the firm’s partners or a committee of partners — known as the general partner — to manage the PE fund’s investments and transactions. The general partner then recruits investors — pension funds, endowments, wealthy individuals and others, known as the limited partners — to invest in the fund and provide it with capital. The general partner typically contributes just 1 to 2 percent of the fund’s equity. The remaining 98 percent or more is contributed by the fund’s limited partners. The limited partners pay a management fee to the general partner of 1.5 to 2 percent of the capital they have committed to the fund. This fee covers the costs and salaries of the general partner. Net of expenses, this is income received by the general partner and is taxed as such. The general partner uses the equity in the PE fund to acquire Main Street companies for the fund’s portfolio. Often, the general partner collects advisory and transaction fees from these companies as well.

Purchases of portfolio companies are typically financed with 70 percent debt that the portfolio company (not the PE firm) is obligated to repay and with 30 percent equity from the private equity fund. As the general partner has contributed only 2 percent of the equity in the private equity fund, and the purchase is accomplished with 30 percent equity, the GP has less than 1 percent of the purchase price of the portfolio company at risk (.02*.30 = .006 or 0.6 percent). So, the general partner, who makes all the decisions about what to buy and how much debt to use, has put up a small fraction of the purchase price and has little to lose. Yet the upside gains realized by the PE fund accrue disproportionately to the GP. When the portfolio company is sold, the PE firm typically collects 20 percent of the profit! This 20 percent profit share is the so-called carried interest and for tax purposes it is treated as a capital gain.

The private equity business model is illustrated in the figure below.

Source: Appelbaum and Batt (2014).

To recap: The PE fund’s general partner receives a disproportionate share of the PE fund’s profits as so-called carried interest. Carried interest is, thus, a form of profit sharing — or performance-based pay — which the GP receives as a result of its success in managing the PE fund’s investments.

Including a profit share as a form of incentive pay in employee compensation is a fairly common practice in various U.S. industries, not just private equity. The United States Steel Corporation provided employees who held positions of responsibility with a share of the company’s profits as early as 1903. Today, the company’s unionized workforce receives a share of the company’s profits. Earnings of these workers are tied to the performance of the enterprise, and the profit share provides an incentive for employees to focus on helping the business succeed. Performance based pay — whether CEO bonuses, sales commissions of real estate brokers or shoe salesmen, or carried interest — is at-risk pay. It depends on how the enterprise performs and there is no guarantee that it will be forthcoming. In every one of these cases with the exception of carried interest, it is taxed as ordinary income. Carried interest is the private equity version of a performance fee.

In steel, as in all industries where employees receive a profit share or other form of performance pay, such compensation is taxed as income. Steelworkers pay income tax on their share of the company’s profits. In sharp contrast to this, however, carried interest — the profit share or performance fee that private equity fund general partners receive for managing the fund — is treated as a long-term capital gain and taxed at the 20 percent capital gains tax rate rather than the 39.5 percent top income tax rate. There is no economic justification for this anomalous tax treatment of carried interest. It reduces the tax revenue received by the IRS by about $18 billion a year to the disadvantage of the tax-paying public, and it gives a huge boost to the after-tax income of private equity fund general partners. Carried interest is simply incentive compensation and should be taxed as income rather than treated as a capital gain. Passage of SB0605 will repatriate the tax revenue lost because of the federal tax treatment of carried interest to the state of Maryland, and will close this tax loophole, at least for Maryland taxpayers.

While PE partners would be loath to give up their tax break on carried interest, many observers sympathetic to the industry admit that this tax loophole is indefensible and should be eliminated. Carried interest does not represent a return on capital that GPs have invested because nearly all of the capital in the PE fund is put up by the fund’s limited partners. This disparity between GPs’ investments and returns led the industry publication, Private Equity Manager, to conclude that GPs’ disproportionate share of a PE fund’s gains is “more akin to a performance bonus than a capital gain” and to agree with the view “that a GP’s share of profits made on investor capital should be taxed as income, not capital gains.” In January 2016, the editorial board of the Financial Times labelled the carried interest loophole “a tax break that Wall Street cannot defend.” The Financial Times wrote:

“Private equity partners and fund managers do not, for the most part, have their own capital at risk when they make these investments. They are receiving payment for a service, namely to invest money on behalf of limited partners in the fund, while losses on investments fall on their clients alone.”

In calling for legislators in the U.S. and U.K. to tax carried interest as income, which it clearly is, the Financial Times notes that “it is an especially egregious break for the well-off at a time when they should be contributing more, not less.”

The hedge fund business model is very different from the private equity model, but they share some key characteristics. A financial investment firm sponsors a hedge fund that is managed by a general partner who recruits investors for the hedge fund. The fund’s investments are managed by the general partner. The general partner puts up a fraction of the equity in the fund, but collects a disproportionate share of the fund’s profits. It’s a stretch for hedge funds to treat this income as a capital gain since they are mainly managing other people’s money and not investing their own. Instead, this profit share or performance fee should be treated in the tax code as the ordinary income it really is. Unfortunately, as in the case of private equity, this income is characterized as carried interest and treated as a long-term capital gain for tax purposes.

This practice by private equity and hedge funds needs to end.

Leading politicians on both sides of the aisle — Donald Trump and Jeb Bush as well as Hillary Clinton and Bernie Sanders — have called for ending the carried interest tax giveaway. But Washington has been slow to act. States are now gearing up to lead the way. Maryland has an opportunity to close this tax loophole. Passage of SB0605 will require those in the state who receive income that is attributable to investment management services to pay their fair share of taxes. This will provide the state with much needed revenue to fund its priorities — schools, housing, jobs, clean energy, or whatever it chooses. Maryland has the chance to be the leader, but the state is not alone in addressing this issue. Initiatives are underway to close the carried interest tax loophole and legislation has been introduced in New York, New Jersey, Connecticut, Rhode Island, Massachusetts, and Illinois in addition to Maryland. Other states that have expressed interest in pursuing this issue include California, Minnesota, Ohio, Pennsylvania, Virginia and the District of Columbia.

I congratulate you on making this effort to close the carried interest tax loophole, and hope that SB0605 passes in the Senate and sister legislation passes in the House.

Thank you.

References:

Financial Times Editorial Board. 2016. “A Tax Break that Wall Street Cannot Defend.” Financial Times, January 4. http://www.ft.com/intl/cms/s/0/8b330a4a-babe-11e5-bf7e-8a339b6f2164.html#axzz3xuLVeIDe.

Fleischer, Victor. 2015. “How a Carried Interest Tax Could Raise $180 Billion.” DealBook, New York Times, June 5. http://www.nytimes.com/2015/06/06/business/dealbook/how-a-carried-interest-tax-could-raise-180-billion.html?_r=1

Private Equity Manager. 2013. “Carry May Be Ordinary Income.” PE Manager Yearbook 2012, January 3. http://www.privateequitymanager.com/Article.aspx?article=71006.