November 24, 2009

November 24, 2009 (Housing Market Monitor)

By Dean Baker

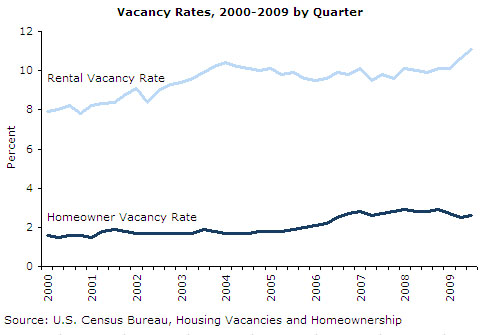

There continues to be enormous excess supply in the housing market; the overall vacancy rate is at an all-time high.

Existing home sales jumped 10.1 percent in October, while the Case-Shiller 20-City Index showed a rise of 0.3 percent for September, its fourth consecutive monthly increase. (The Case-Shiller data is a three month average centered on September.) Both increases were driven by the expiration of the first-time homebuyers tax credit at the end of November.

The surge in sales in October is consistent with earlier releases showing that pending home sales were sharply higher in August and September, as were purchase mortgage applications. However, the sharp rise in sales in October is coming at the expense of sales in future months. The Mortgage Applications Index has plummeted over the last 6 weeks, hitting its lowest level since 1997 last week. Sales are clearly headed sharply lower in the months ahead. The extension and expansion of the first-time buyers credit will have a positive impact, but it will not be sufficient to prevent a downturn.

The basic fact is that there continues to be enormous excess supply in the housing market. This is evidenced most immediately by the record vacancy rate in the housing market. While the vacancy rate for ownership units is down slightly from its peak earlier in the downturn, the rental vacancy rate is at an all-time high, pushing the overall vacancy rate to a new high.

Most immediately, the oversupply of housing is pushing down rents. Nominal rents are falling in the CPI for the first time on record. This is especially striking since CPI rents have much more inertia than market rents. The vast majority of rental units do not turn over in any given period. Landlords lower (or raise) rents for existing tenants much less than they do when a unit turns over. As a result, the CPI rental index generally shows much smaller changes than indexes that only examine rents in units on the market.

The drop in market rents will eventually put downward pressure on house prices. The amount that homebuyers are willing to pay for a home will inevitably adjust to rents in the market. Also, landlords will be more likely to put homes up for sale as rents drop.

While the 20-city index is increasing, there continues to be very different patterns across the country. Some of the bubble markets have at least temporarily stopped deflating. In Phoenix, prices have risen at a 13.1 percent annual rate over the last quarter. In Los Angeles, prices have risen at a 13.4 percent rate. In San Diego, the annual rate of increase has been 19.8 percent and in San Francisco, 32.5 percent. These increases follow very sharp price declines earlier this year and in 2008. It seems unlikely that these price rises will be sustained.

On the other hand, prices in Seattle have fallen at a 3.0 percent annual rate over the last quarter. Prices in Las Vegas continue to plummet, falling at a 14.3 percent rate, while prices in Cleveland fell at a 5.1 percent annual rate.

Dean Baker is Co-Director of the Center for Economic and Policy Research, in Washington, D.C. CEPR’s Housing Market Monitor is published weekly and provides an incisive breakdown of the latest indicators and developments in the housing sector.