September 26, 2013

September 26, 2013, Dean Baker

I want to thank Chairman Carper and Ranking Member Coburn for giving me the opportunity to address the committee. I will use this opportunity to make two key points on the finances of the Postal Service.

-

The rate at which the Postal Service is being required to prefund its retiree health benefits has no obvious economic logic. The current pace of funding poses a serious threat to the Postal Service’s survival as an ongoing operation. This excessive burden could create a situation in which the Postal Service is unnecessarily forced into liquidation, leaving taxpayers with the burden of meeting retiree obligations.

-

While many have indicated a desire to have the Postal Service compete with private firms on a level playing field, this is not currently the case. In addition to being required to build up a funding level for its retiree health benefits that has little precedent in the private sector, the Postal Service is also required to invest both its pension fund and its retiree health fund exclusively in government bonds. By contrast, private companies invest their funds in a diversified portfolio. Given the size of the pension and retiree health funds, the difference in returns would translate into several billion dollars a year. This difference would have been sufficient to have eliminated the Postal Service’s losses over much of the last decade.

The Rate of Prefunding the Retiree Health Benefit Fund

The point I wish to make on the rate of prefunding set out in the Postal Accountability and Enhancement Act (PAEA) is a simple one. In the PAEA Congress decided to reverse the Postal Service’s method for financing retiree health benefits. Until the passage of the PAEA, retiree health benefits were essentially funded on a pay as you go basis, with the funding being treated as a current expense. This is in fact a common practice in the private sector.

While there are good reasons for prefunding retiree health benefits, the pace at which the targeted prefunding level is reached is to a large extent arbitrary. Congress opted to give the Postal Service 10 years to reach a 73 percent funding target by 2016. This target was expected to require contributions averaging $5.5 billion a year, an amount that is close to 8 percent of the system’s current revenue. This would be an extraordinary burden to suddenly place on any company. It is equivalent to imposing a tax of 8 percent on the Postal Service’s revenue. There are few businesses that would be able to survive if they were suddenly required to pay an 8 percent tax from which their competitors were exempted.

The goal of ensuring that taxpayers will not be left with the cost of providing health care for the Postal Service’s retirees is understandable, but it is not best accomplished by imposing a burden that is large enough to jeopardize the Postal Service’s viability. In fact, if this burden unnecessarily forces the liquidation of the Postal Service then the rapid rate of accumulation in the retiree health fund could have the opposite of its intended effect, forcing taxpayers to pick up a large amount of unfunded liabilities.

In this respect, it is important to note that the Postal Service’s underlying financial situation has improved substantially in the last two years. The Postal Service was hard hit both by the economic downturn and by technological developments that were leading consumers to rapidly replace first class mail with electronic means of communications. Postal Service revenue peaked at $75 billion in 2008, then fell sharply to $66 billion in 2011. The Postal Service expected revenue to continue to decline rapidly for the rest of decade, falling to $63 billion in 2013 and just $59 billion by 2020.1 However, this projection proved to be far too pessimistic. The rate of revenue decline slowed sharply in 2012 and has reversed this year, with 2013 revenue running somewhat ahead of the corresponding quarters in 2012.

This pattern is noteworthy because, contrary to what the 2011 projections might have implied, the Postal Service now appears quite capable of being a viable enterprise. It would be showing a profit in the current year if not for its contributions to the Retiree Health Benefit Fund (RHBF).2 If payments to the RHBF were stretched out over a longer period of time, it could help to ensure the Postal Service’s viability and reduce the risk that the taxpayers will be forced to accept this liability.

A delay in reaching the targeted rate of prefunding might seem especially appropriate in the wake of the 2007-2009 recession, which Congress surely did not anticipate at the time it approved the PAEA. While the pace of prefunding required under the PAEA would have been ambitious under any circumstances, it was clearly impossible to sustain in the context of the most severe downturn since the Great Depression. Given the extraordinary depth and duration of the downturn, it would be reasonable for Congress to adjust its prefunding targets to ensure that they do not interfere with the viability of the Postal Service.3 Given the large level of reserves that the Postal Service has already accumulated in the RHBF, there is no doubt that it will be able to meet all its obligations even if it is allowed to take a longer period of time to build up to its funding targets.

The Handicaps the Post Service Faces in Competing With Private Companies

For the last four decades the Postal Service has been operating with a mandate under which it was expected to compete with private companies. The expectation has been that the Postal Service would be able to support its operations without the benefit of government subsidies. However, few intended for it to compete with private corporations while facing unique burdens that its private competitors do not share. In fact, this is exactly the situation that the Postal Service now faces, first and foremost because of the requirement that it invest its pension fund and the RHBF exclusively in government bonds rather than a diversified portfolio. (Arguably the Postal Service has been restricted in its ability to enter new lines of business. Given the enormous nationwide delivery system it has in place, this restriction is a considerable handicap.)

The restriction that the Postal Service retiree funds be invested exclusively in government bonds puts the system at major disadvantage compared with its private competitors since it requires the Postal Service to spend much more money to provide the same benefit. One of the Postal Service’s competitors, UPS, does in fact offer retiree benefits and is able to do so at a much lower cost than the Postal Service as a result of its freedom to invest in a diverse range of assets. However even if no competitors offered comparable benefits this rule would still put the Postal Service at a disadvantage since it means that it must make payments that private businesses would not be required to make.

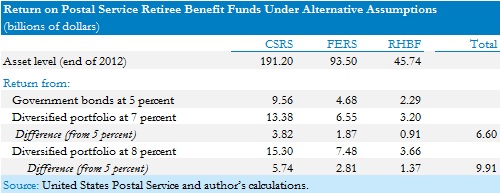

Since the Postal Service has prefunded these benefits to such a large extent, this difference in investment returns is a substantial penalty for the Postal Service. The table below shows the returns that the various Postal Service retiree funds would have had in calendar year 2013 under the assumption that they had been invested in a diversified portfolio compared with an assumed 5.0 percent nominal return on government bonds.

Source: United States Postal Service and author’s calculations.4

As can be seen the difference in returns if the pensions had been invested in a diversified portfolio that earned a 7.0 percent nominal rate of return would have been $6.6 billion in the current year, allowing the Postal Service to enjoy a healthy profit. If the a diversified portfolio had earned an 8.0 percent nominal return, the difference would have come to $9.9 billion in 2013, leading to a very substantial profit for the Postal Service in the current year.

There are reasons that Congress would not want to have the Postal Service invest its retirement funds in a diversified portfolio in the same way as a private corporation, most obviously because it would increase the government’s deficit as it is usually reported. However, it must recognize that it is imposing a very costly restriction on the Postal Service. As the table shows, the cost of this restriction is quite large relative to the profits and losses seen by the system in recent years.

Conclusion

In 2006 Congress decided to change the accounting rules under which the Postal Service operated, requiring that it prefund its retiree health benefits rather than treat them largely as a current expense. The legislation required the Postal Service to rapidly build up to it 73 percent targeted level of funding. This funding schedule would have imposed a large burden on the Postal Service under any circumstances; however the burden became unbearable in the context of the worst economic downturn since the Great Depression. Since Congress certainly not anticipate this sort of downturn when it passed the PAEA, it would be reasonable for it to re-examine the timeline for prefunding. There is little obvious risk to taxpayers if the target was stretched out over several decades.

While the Postal Service is ostensibly supposed to be competing on a level playing field with private corporations, it still faces many serious handicaps which its competitors do not share. Most importantly the requirement that it invest its retiree funds exclusively in government bonds makes retiree benefits far more expensive to the Postal Service than to private companies. The difference in returns could be close to $10 billion a year, given current asset levels. This difference is very large relative to the Postal Service’s recent profits and losses, implying that Congress is imposing a substantial penalty on the system by this requirement. If it really wants the Postal Service to be a level playing field with private competitors then it should take measures to address this difference in returns.

1 These figures are taken from Corbett, Joseph. 2011. “The USPS Financial Outlook: December 2011.” P 21.

2 Over the first nine months of 2013 the Postal Service reported a loss of $3,870, which is $330 million less than the $4,200 million it contributed to the RHBF. (UNITED STATES POSTAL REGULATORY COMMISSION, Third Quarter, 2013, Form 10-Q, p24)

3 It is also worth noting that the Postal Service assumes a much higher rate of health care cost growth than the economy has seen in recent years. The projections of liability assume a 7 percent annual rate of increase in per person health care costs. The most recent projections from Centers for Medicare and Medicaid Services assume cost growth averaging just 5.0 percent for the next decade (Centers for Medicare and Medicaid Services, 2012. “NHE Projections 2012-2022.” http://www.cms.gov/Research-Statistics-Data-and-Systems/Statistics-Trends-and-Reports/NationalHealthExpendData/Downloads/Proj2012.pdf

4 The assets for the various retirement funds can be found in the 2012 Postal Service’s Form 10-Q. The pension fund balances are on page 37, and the RHBF on page 42.