Article • Mark Weisbrot’s Columns

The International Monetary Fund’s Special Drawing Rights: Why a New Issuance is Necessary and Feasible at this Time, and Would Save Many Lives

Article • Mark Weisbrot’s Columns

Fact-based, data-driven research and analysis to advance democratic debate on vital issues shaping people’s lives.

Center for Economic and Policy Research

1611 Connecticut Ave. NW

Suite 400

Washington, DC 20009

Tel: 202-293-5380

Fax: 202-588-1356

https://cepr.net

Updated: October 21, 2024

1. The 2021 SDR issuance is estimated to have saved hundreds of thousands of lives, if we use, e.g., the Bank for International Settlements’ research on the relation between recessions and mortality.

2. Yet the US Treasury Department has “ruled out a new allocation of IMF Special Drawing Rights resources and said the Fund needed to stick to its core activities of strong surveillance, policy advice and reforms required in its lending.” But the world economy is vastly worse now than it was on August 2, 2021, when the SDR issuance was approved by the IMF.

The IMF predicts that global growth will slow to 3.2 percent in 2024 — about half that of 2021. About 80 low- and middle-income countries are in, or at risk of, debt distress. The most recent five-year growth projection from the World Economic Outlook was just 3.1 percent annually, the lowest projection since 1990. And IMF Managing Director Kristalina Georgieva has issued grave warnings about the high risks of global economic shocks, and the lack of a global economic safety net.

3. A new SDR issuance, which would come at no cost to the US taxpayer, could make a significant difference in the US economy in the immediate future by preventing some of the loss of export-related jobs here, as demand for US exports falls with recessions in other countries.

The US economy lost an estimated 2.2 million export-related jobs from January 2020 to May 2021 due to the loss of demand for US exports in the rest of the world because of the pandemic recession.1 While some of these have since been recovered, the risk of global economic disruption is high. SDRs could help to stabilize the world economy and protect export-related jobs for US workers.

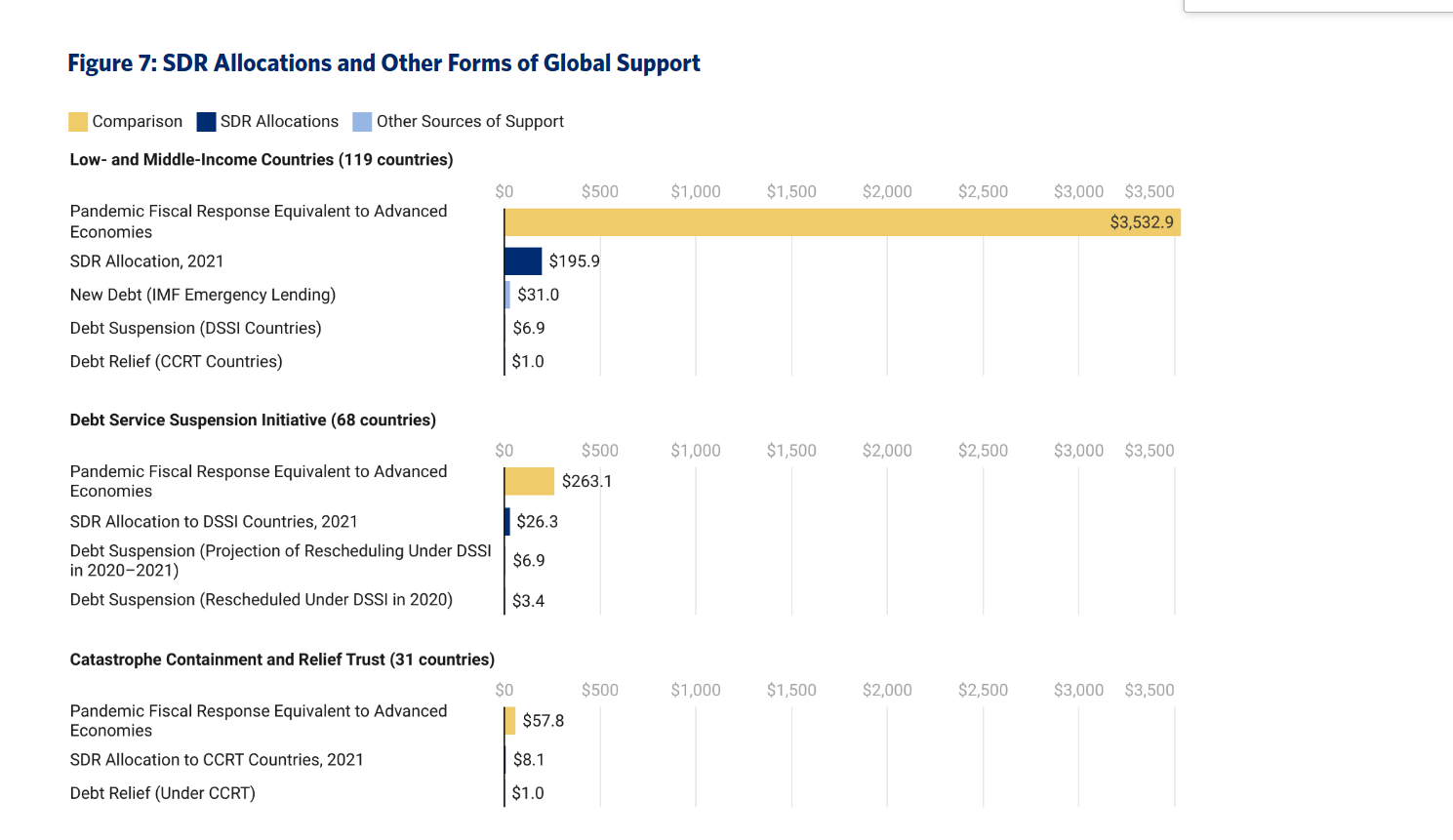

4. The 2021 SDR issuance was by far the largest source of any aid to developing countries in any year since the pandemic.

Figure 1 shows how much larger the SDR allocation is for each group of developing countries, as compared with what was received (often adding to countries’ debt) by countries covered by other initiatives (the Debt Service Suspension Initiative, DSSI; and the Catastrophe Containment and Relief Trust).

Sources and Notes: Figure 2, Kevin Cashman, Andrés Arauz, and Lara Merling, “Special Drawing Rights: The Right Tool to Use to Respond to the Pandemic and Other Challenges,” Center for Economic and Policy Research, April 7, 2022.

While more than 70 countries are eligible for the G20 Common Framework for Debt Treatments, the debt restructuring process has proved to be very difficult to access and prone to delays. Just four countries have applied since it began in 2020, and negotiations have been protracted, the length of time in the process averaging two years and eight months.2 Unlike other forms of support, SDR issuances are rapid and uncomplicated; they do not require any budget expenditures or government appropriations from the United States (or other IMF member countries).3

5. SDRs create no debt and have no conditions attached, making them 100 percent net positive, unlike, e.g., IMF or other loans.

This is especially important right now, given the rise in sovereign debt since the pandemic. While rates are finally beginning to come down, the average coupon paid by developing countries on dollar-denominated debt is expected to continue to rise as existing debt is refinanced.4

Weak medium-term growth prospects make the current debt burden more damaging, as IMF Managing Director Kristalina Georgieva remarked at the opening of this year’s Annual Meetings (October 17):

medium-term growth is forecast to be lackluster—not sharply lower than pre-pandemic, but far from good enough. Not enough to eradicate world poverty. Nor to create the number of jobs we require. Nor to generate the tax revenues that governments need to service heavy debt loads while attending to vast investment needs, including the green transition.

6. The US Treasury Department (beginning with former secretary Steven Mnuchin, who immediately killed the proposal for a new allocation of SDRs at the IMF when it was first made by the managing director in March 2020), has offered only two arguments against an issuance of SDRs. First, they have argued that more than 60 percent of the issuance goes to high-income countries, and that therefore it is more reasonable to “rechannel” those SDRs rather than issue new ones. This argument is deeply flawed:

i. It has been more than three years since the last issuance of SDRs, and few SDRs have been effectively rechannelled. This is much too slow; 309 million people are now at risk of starvation, up from 135 million before the pandemic and from 276 million at the start of 2022. As soon as the Treasury Department gives the go-ahead to a new SDR issuance, they can be unlocked for transfer to IMF member countries within weeks.

ii. Unlike a new issuance, rechanneling the US’s SDRs requires congressional approval. In the current Congress, this is extremely unlikely, if not impossible.

iii. There is no waste, creation, or use of resources involved in the SDRs distributed to high-income countries, because these countries cannot use them under IMF rules. Nor can China use them, as it has more than $3 trillion in reserves.5 Only countries that can show need can make active use of the SDR allocation.

iv. Perhaps most importantly, the proposed rechanneling would convert SDRs from an international reserve asset that carries no debt and no conditions to a loan that both creates debt and has conditions attached.6

Second, the Treasury has recently put forth the argument that the Poverty Reduction and Growth Trust (PRGT) is a sufficient alternative to a new issuance since its interest rate is cheaper than the SDR interest rate. This argument is also seriously flawed:

i. Developing countries do not have to pay interest on SDRs unless they convert them to hard currency and fall below their original allocations but they receive substantial benefits even if they do not convert them to hard currency. The additional reserves that are received by member countries in a new issuance by themselves reduce the risk of balance of payments and other economic crises, as well as lowering borrowing costs.

ii. As they are substitutable for other reserves, SDRs can also free up other liquid reserves that can be sold and spent. They therefore help create badly needed fiscal space – including for necessities such as food, medicine, and life-saving health infrastructure, even if they are not converted directly to hard currency.

iii. The SDR interest rate is the weighted average of the short-term interest rates from the currencies in the SDR basket (US dollar, euro, Chinese renminbi, Japanese yen, and British pound). It rose because of tighter monetary conditions, but is now falling; it is down 0.6 percentage points since June, to 3.5 percent currently. This is still far cheaper than the coupon that most developing countries would pay elsewhere.

iv. The PRGT is an inadequate alternative to a new SDR issuance. In the past five years only $30 billion has been lent through this vehicle, which is also not accessible to middle income countries. In contrast, developing countries (excluding China) received $209 billion in SDRs from the 2021 issuance alone.

7. There is no downside risk to a new issuance, and no economists have put forth credible economic arguments against an issuance.

8. There is no cost to the US budget or the US taxpayer, at present, or in the future, from a new issuance.

9. Note: IMF-member countries under US sanctions (e.g., Iran, Venezuela, Russia, Myanmar, Belarus, Afghanistan, and Syria) have not been able to access their holdings of Special Drawing Rights.7

Article

Article

Article

Article

Article

Report

Article

Article