May 04, 2011

This is what the Post was warning about in its article headlined, “The dollar, at risk: U.S. efforts to speed the economic recovery could transform currency’s slow decline into a precipitous fall,” although it is possible that no one at the paper knows the introductory economics that would allow them to make this connection.

Those who have been through an intro econ class know that the trade surplus is by definition equal to net national savings. This means that countries that have large trade deficits like the United States must by definition have negative net national savings.

The main determinant of the trade surplus (or deficit), given a level of GDP, is the value of the dollar. If the value of the dollar were to fall precipitously, which is presented here as a bad scenario, it would lead to a quick adjustment towards balanced trade through strong growth in net exports. Higher levels of net exports would boost the economy, leading to stronger private savings and a smaller budget deficit. So, the Washington Post headline is actually warning that if we are not careful, we will see stronger economic growth and a smaller budget deficit.

As a practical matter, the precipitous fall in the dollar warned about in the article is almost impossible for exactly this reason. The euro zone countries would not let the dollar fall to 2 dollars to a euro precisely because it would destroy Europe’s export market in the United States and make U.S. goods hyper-competitive in Europe. The same is true of Canada, Japan, China and other U.S. trading partners. If the dollar were for some reason go into a free fall all of these countries would almost certainly actively intervene in currency markets (as China already does) to limit the decline. This should be obvious to anyone who has reflected on the situation for even a minute.

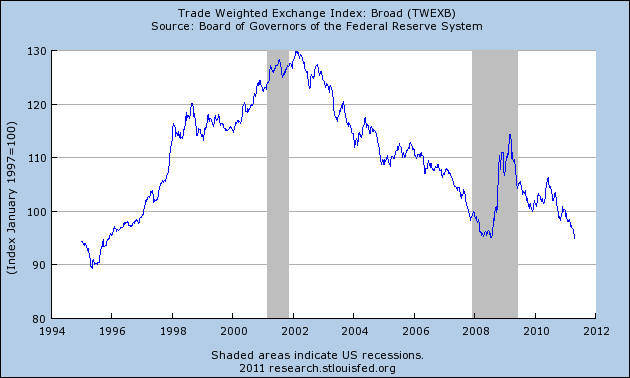

The article gets several other important points wrong. First, the fall in the dollar is only reversing the run-up in the dollar that began with Robert Rubin’s stint as Treasury Secretary. Rubin’s high dollar policy sent the country on the course of bubble driven growth of the late 90s and the 00s that led to record low private savings rate and in last few years, high budget deficits. The recent decline in the dollar is just reversing the Rubin run-up.

The other important fact that the Post got completely wrong was its assertion that:

“History is full of examples of countries where large budget deficits eventually led investors to lose faith, causing the currency to tumble. The Asian financial crisis, which rocked the likes of Thailand, Singapore and South Korea in the late 1990s, is one recent example.”

According to the IMF, in the year prior to the East Asian financial crisis, Thailand had a budget surplus equal to 2.7 percent of GDP. Singapore and South Korea had surpluses equal to 14.4 percent of GDP and 2.6 percent of GDP, respectively. These countries clearly do not support the claim in this article that large budget deficits lead to declining currency values.

Comments