December 30, 2012

The Post had a major business section article promising that 2013 could be the year of a “rip-roaring” recovery, if nothing bad gets in the way. While there are reasons to think that 2013 could be better than the prior two years, it’s not clear that “rip-roaring” would be the right term to apply.

The high-end of growth forecasts is around 3.0 percent. This assumes that the budget standoff is resolved relatively quickly on terms that do little damage to the recovery. According to the Congressional Budget Office (CBO) the economy is currently operating about 6 percent below potential GDP. CBO puts potential growth at 2.4 percent, which means that if the economy does grow at a 3.0 percent rate we would be reducing the output gap by 0.6 percentage points.

At this pace it would take us 10 years to get back to potential GDP. When the economy has suffered severe downturns in the past, for example in 1974-75 and 1981-82, the economy had stretches of growth in the range of 7-8 percent. That sort of growth could reasonably be described as “rip-roaring,” 3.0 percent doesn’t really fit the bill.

There are a few other items that are not exactly right in this piece. It rightly notes the improvement in the housing sector, which is likely to continue into 2013, but neglects to mention the vacancy rate. While there has been a considerable decline in the vacancy rate from the record levels reached in 2010, the vacancy rate is still far above its pre-bubble level. This will be a drag on construction as many people forming their own household can turn to units that are currently vacant rather than newly constructed units.

The piece also holds out the hope that consumer spending will rebound based on the fact that consumers have paid down much of their debt from the bubble years. This claim is bizarre for two reasons. First, it is not just debt that affects spending. It is also wealth. A debt of $1 million would leave most of us struggling to meet our payments. By contrast, if Bill Gates had $1 million in debt it would not affect his consumption at all, because he also has $50 billion in assets. The story of the downturn in consumption is that households have lost close to $8 trillion in housing equity. This explains the downturn in consumption from its bubble peaks. The role of debt is very much secondary.

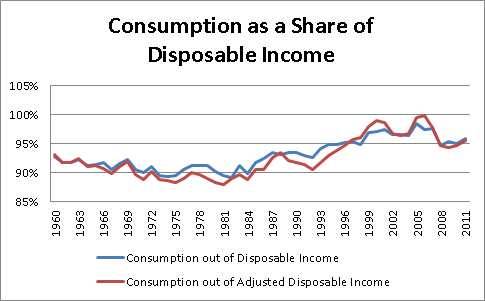

The other reason why the prediction of an upswing in consumption is bizarre is that consumption is already at an unusually high level relative to disposable income. If anything, it should be surprising that consumption is so high, given the loss of so much housing wealth.

Source: Bureau of Economic Analysis.

Finally, the piece seems to have reversed the relative impact on growth and unemployment associated with the ending of the payroll tax cut, telling readers:

“The CBO estimates that the end of the payroll tax holiday, combined with an extension of unemployment benefits, could cost the economy 0.7 percentage points of growth and increase the jobless rate by 0.8 percentage points over what it otherwise would have been.”

Usually the impact on growth is roughly twice the size of the impact on the unemployment rate. While it is plausible that CBO projected that the end of the payroll tax cut would slow growth by 0.7 percentage points, it is not plausible that this would be associated with a 0.8 percentage point rise in the unemployment rate.

Comments