November 24, 2013

With the Fed promising to keep the overnight money rate at zero long into the future, while it throws $85 billion a month into the economy with its quantitative easing policy, many are no doubt wondering who is on watch against another outbreak of inflation.

Greg Mankiw gave us the answer to that question in his NYT column today. After noting that the job vacancy had risen to 2.8 percent, which Mankiw describes as “almost back to normal,” he tells readers;

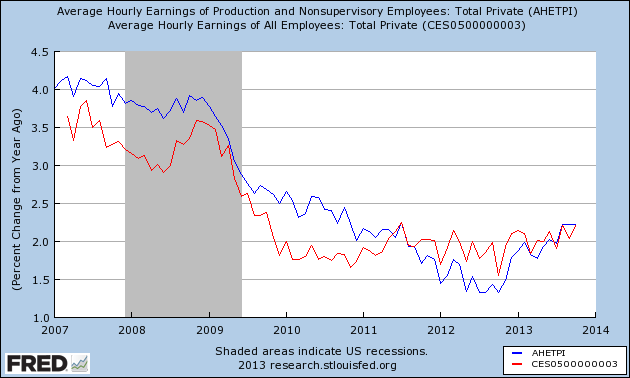

“Data on wage inflation also suggest that the labor market has firmed up. Over the past year, average hourly earnings of production and nonsupervisory employees grew 2.2 percent, compared with 1.3 percent in the previous 12 months. Accelerating wage growth is not the sign of a deeply depressed labor market.”

Let’s check this one out a bit more closely. The graph below shows the year over year growth in average hourly earnings for production and nonsupervisory workers (blue line) and all employees (red line). The former group comprises a bit more than 80 percent of the work force. The latter group tends to be more highly educated and is better paid on average.

If we look at the chart there is a modest acceleration in wage growth for production non-supervisory workers in 2013, but only because the rate of wage growth had continued to fall through 2012. If acceleration or deceleration is the measure of whether we have a fully utilized labor market we went quite quickly from a period of excess slack in 2012 when wages were falling to a period of tightness in the last year, even though employment growth has been rather tepid. That one seems a bit hard to accept.

Furthermore, if we use the broader measure of wage growth for all workers, we don’t see any evidence of acceleration at all. Wage growth has been hovering around 2.0 percent for the last two and a half years. It had been somewhat lower in 2010 (@ 1.6 percent), but there certainly is no upward pattern in this series.

A small upward tick in wage growth for production and non-supervisory workers, but no change in overall wage growth, is evidence of a shift in relative demand not excess aggregate demand. It would suggest that the demand for workers with more education and skills is weakening relative to the demand for less educated workers. Of course the difference is relatively modest and could easily be reversed in the months ahead, but that is how economists would ordinarily read this evidence. (It is also important to remember that with inflation running just a bit under 2.0 percent, this translates into an annual rate real wage growth of only around half a percentage point.)

It is also worth noting that Mankiw’s other measure of a fully employed labor force is also dubious. At 2.8 percent the vacancy rate is up from its low in 2010, but this is a series that does not move much. There were two months in 2012 where the vacancy rate was 2.8 percent also. In the 2001 downturn, the rate never fell below 2.3 percent. (It had been as high as 3.8 percent before the recession.) In contrast to the rise in the vacancy rate back to near pre-recession levels, the number of people looking for work is more than 50 percent higher than before the recession. That is hardly consistent with a story with the labor market being near full employment.

Comments