January 26, 2014

One of the reasons that the housing bubble caught so many people by surprise was that the media relied largely on people who had an interest in pushing housing as their sources in reporting. This still seems to be the case today as indicated by a NYT piece on the housing market.

At one point the piece cites economist Mark Zandi, telling readers:

“Tighter lending standards are shutting out close to 12.5 million consumers who would qualify in normal times.”

It’s difficult to attach any meaning to this statement. We currently have 75 million home owning households and 40 million renting households. Is Zandi saying that among the 40 million renting households we have 12.5 million people who would in other times qualify for mortgages but do not today? Many renters do now qualify for a mortgage. If we say that a quarter of renters could now buy a home if they wanted, then Zandi’s claim would be that 12.5 million of the 30 million remaining renters (42 percent) would in normal times be able to get mortgages but are unable to do so because of tight credit conditions today. That one is a bit hard to believe. (It’s possible that the number includes people who can’t refinance because they have little or no equity in their home, but that is a very different issue.)

In the same vein, the piece tells readers:

“Mortgages are roughly seven times harder to get than they were five years ago, according to the Mortgage Bankers Association’s credit availability index, and they show few signs of getting easier.”

The seven times harder refers to an index that the Mortgage Bankers Association constructed that is at one seventh of its value five years ago. It doesn’t mean that a person has one seventh the chance of getting a mortgage.

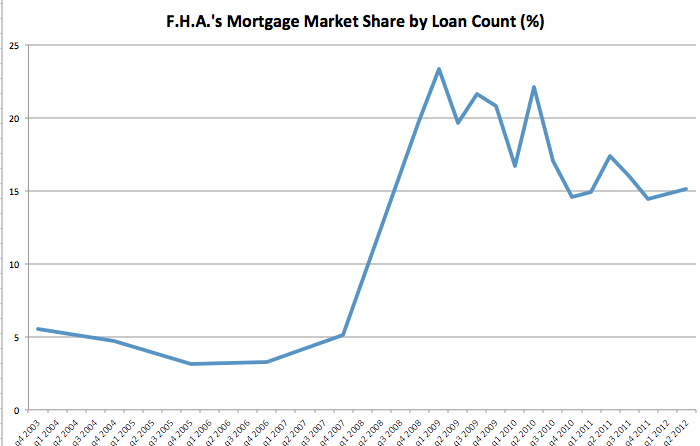

Incredibly this piece never mentions the role of the Federal Housing Authority (FHA). While the FHA virtually disappeared as a factor in the housing market at the peak of the housing boom, because it did not relax its standards, its role hugely expanded after the crash. When the housing market was bottoming out in 2009 and 2010 it guaranteed more than 20 percent of new mortgages. It still insures close to 15 percent. Many people who would not meet the standards for a Fannie Mae or Freddie Mac mortgages can get one insured by the FHA.

Source: Business Insider/HUD.

Comments