February 19, 2014

Today’s target is the usually astute Ryan Avent. Writing in the Economist, Ryan tells readers:

“Two rich economies, relatively similar in structure, reacted very differently to the global financial shock of late 2008. In America output sank sharply but then rebounded to new highs. Employment, by contrast, fell dramatically and has recovered much more slowly; it has yet to regain the pre-crisis peak. In Britain the trends were reversed; employment is setting new highs while output suffered an L-shaped recovery.”

The piece goes on to explain that because of a drop in real wages, firms in the U.K. hired more workers. By contrast, in the U.S. firms went the route of adopting productivity enhancing technology.

The problem with this story is that employment has actually followed a similar path in the U.K. and the U.S. in the upturn. According to OECD data, in the U.K. between 2010 and the third quarter of 2013, the employment to population ratio for workers between the ages of 16 to 64 rose from 69.5 percent in 2010 to 70.8 percent. That’s a rise of 1.3 percentage points. By contrast, in the U.S. the increase was from 69.7 percent to 70.4 percent, a rise of 0.7 percentage points.

While 1.3 percentage points is more than 0.7 percentage points, it doesn’t describe a qualitatively different situation. Furthermore, the gap would largely disappear if we looked at hours worked. The OECD data shows the average number of hours per worker increasing by 0.6 percent in the U.S. between 2010 and 2012 compared to a rise of just 0.1 percent in the UK. In other words, the story that firms in the U.K. are turning to hiring labor because it is cheaper simply is not true. The labor might be cheaper, but isn’t lead to more hiring.

I actually think there is a great deal to Ryan’s larger point, that productivity is to a large extent a response to wages. In the U.S. we have lots of low productivity jobs that exist because people are desperate for work, such as the midnight shift at convenience stores. If wages were higher, these jobs would disappear, leading to a rise in productivity. So the story is reasonable, it just doesn’t apply to the situation being examined.

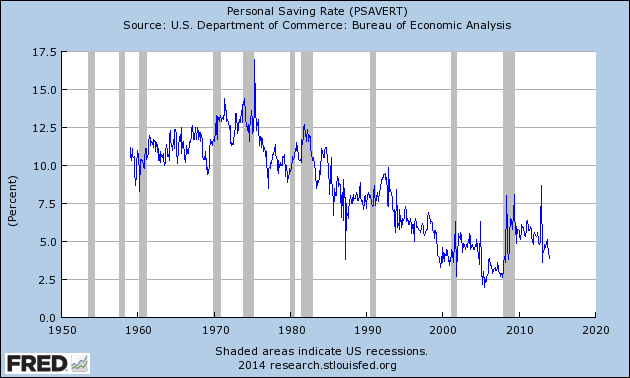

Since I am on the topic of explaining things that didn’t happen, I will turn to my favorite, the weak consumption in the wake of the downturn. We have had endless tracks explaining why people are not spending as much in the recovery as they did before the downturn. Most of this centers on debt overhangs and the like. I would hate to destroy so much job creating potential for economists, but it is worth pointing out that people actually are spending.

Here’s the simple story, the saving rate is actually relatively low right now, which means that consumption is relatively high.

The current saving rate is near 4.0 percent. That’s higher than the lows hit at the peaks of housing bubble in the last decade or the stock bubble in the 1990s, but it is considerably lower than the averages for the 1960s, 1970s, 1980s, and even the 1990s.

This means that people are actually spending an unusually high share of their income. They are not spending as high a share of they did in 1999-2000 or 2004-2007, but that’s because they had trillions of dollars of bubble generated wealth in those years. The concept of a wealth effect, whereby people spend based in part on their wealth, goes back at least 80 years, so economists should be familiar with it.

Anyhow, just because there is no falloff in consumption doesn’t mean lots of economists can’t devote their time to explaining it. After all, what else do they have to do?

Comments