November 23, 2015

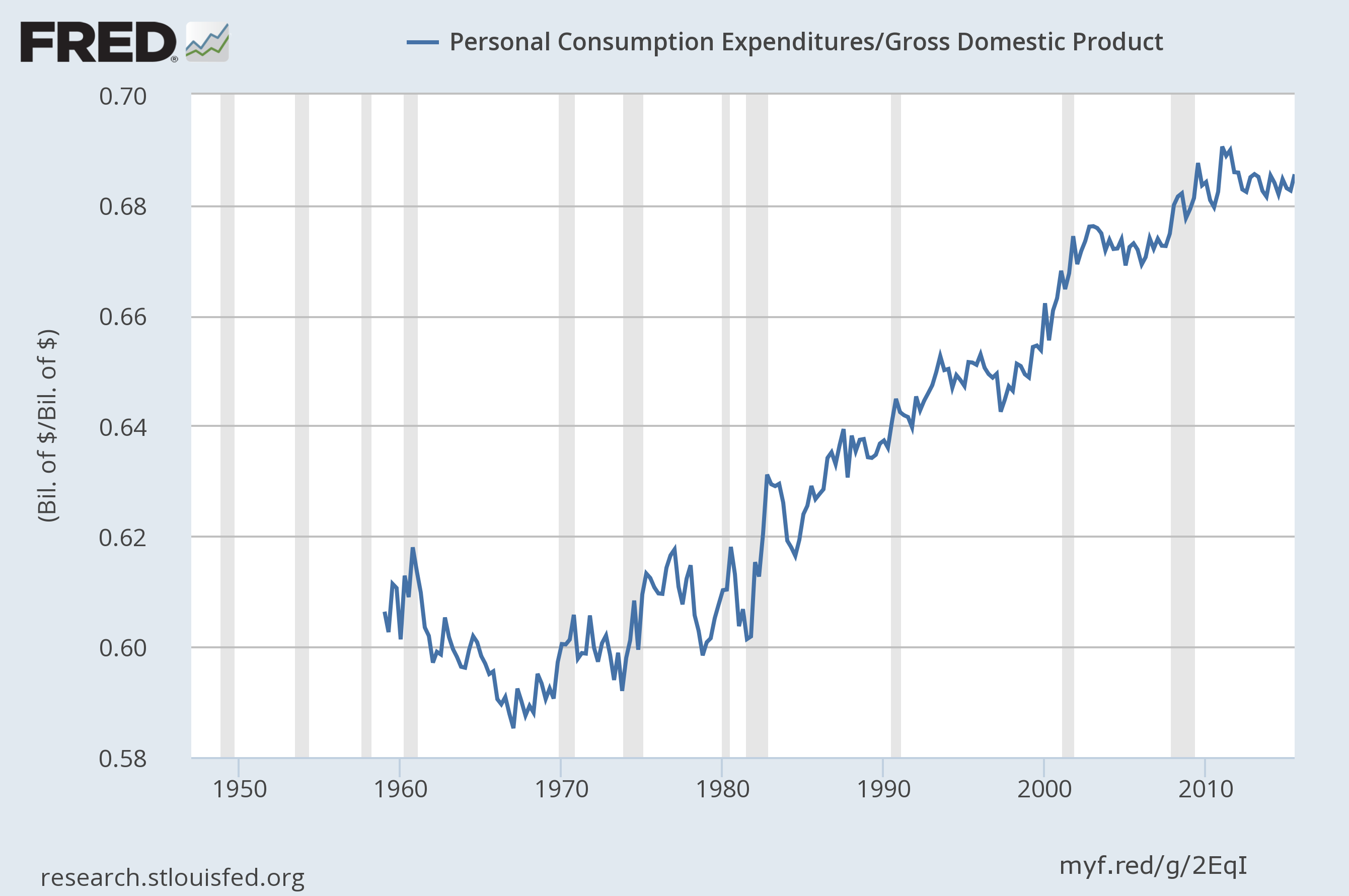

There is an ongoing myth about the downturn and the weak recovery that consumers unwillingness to spend has been a major factor holding back the recovery. An article in the Washington Post business section headlined, “heading into the holidays the retail industry faces a cautious consumer,” draws on this myth. The reality is that consumers have not been especially reluctant to spend in the downturn or the recovery as can be easily seen in this graph showing consumption as a share of GDP.

As can be seen, consumption is actually higher relative to GDP than it was before the downturn. It even higher relative to GDP than when the wealth created by the stock bubble lead to a boom in the late 1990s. The only time consumption was notably higher relative to GDP was in 2011 and 2012 when the payroll tax holiday on 2 percentage points of the Social Security tax temporarily boosted people’s disposable income relative to GDP.

(Those who see an upward trend need to think more carefully about what is being shown. Consumption can only continually rise as a share of GDP if investment and government spending continually fall and/or the trade deficit expands continually relative to the size of the economy. Standard models do not predict either event and both would be quite strange if true. It is also worth noting that the consumption share of GDP fell sharply in the 1960s due to the growth of investment and government spending.)

The weak consumption story is one of the myths that makes the housing bubble far more complicated that it actually is. The basic story is that housing construction, and the consumption driven by housing bubble generated equity, were driving the economy before the bubble burst in 2006–2008. When the bubble burst, the over-construction of the bubble years led to a huge falloff in construction and a temporary drop in consumption.

There was no component of demand that could easily fill this gap, which was on the order of six percentage points of GDP (@$1.1 trillion annually in today’s economy.) The stimulus went part of the way, but it was too small and faded back to near zero by 2011.

The problem of the continuing weakness of the economy is that we still have nothing to fill this demand gap. Housing has come back to near normal levels, but not the boom levels of the bubble years. If anything, consumption is unusually high, driven by house and stock prices that are above trend, even if not necessarily at bubble levels.

The one sure way to close the demand gap is to reduce the trade deficit, most obviously by getting down the value of the dollar. Unfortunately, the powers that be in Washington don’t talk about currency values, hence there are no provisions on currency in the Trans-Pacific Partnership. (There is an unenforceable side agreement.) We could try to get to full employment with shorter work weeks and years, through measures such as work sharing, paid family leave, and paid vacations, but this route is also largely off the agenda.

Anyhow, we don’t have cautious consumers and we don’t have any mysteries about the economy’s ongoing weakness. We just have a lot of confusion generated by the media in discussing the topic.

Comments