January 09, 2013

By the conventional “peak to trough” measure, the recession that began in December 2007 ended 18 months later, in June 2009. But you’d be hard-pressed to find much evidence of “recovery” in the labor market. Job creation is barely keeping up with population growth. The marginal decline in the unemployment rate (from about 10 percent at its worst to just under 8 percent at the end of 2012) has been driven mostly by people dropping out of the labor force. And long-term unemployment remains stubbornly high.

All of this begs a bigger question: What would real recovery look like?

The first and simplest measure (see graphic below) is simply to chart our progress towards regaining the jobs lost during the downturn. This yields a flat threshold at the December 2007 employment levels, and a jobs deficit that pushed past 8 million in late 2009 and now sits at about 3 million.

This “struggling back to the surface” measure has some utility, especially in comparing the recovery trajectories of different recessions. But it becomes less useful the longer the downturn lasts, as population growth creates a new baseline for the labor force. Getting back to December 2007 employment has little meaning after five years of immigration, retirements, and high school and college graduations.

The second measure, the pre-recession unemployment rate of 4.7 percent, yields a more ragged threshold. This measure holds the unemployment rate constant, while allowing for both growth in the labor force and changes in rates of labor force participation. This is a starkly artificial measure, since rates of labor force participation and unemployment are closely related: People drop out of the labor force (stop looking for work, go back to school) when employment prospects are dim. But this, in effect, is the way job numbers are often reported, as if the unemployment was driven solely by a loss or gain in jobs.

The third measure, which holds both the unemployment and labor force participation rates at their December 2007 levels, offers a better (but more dismal) appraisal of where we are. It assumes not only that we want to return to the pre-recession levels of unemployment—but also that we want to return to pre-recession levels of labor force participation.

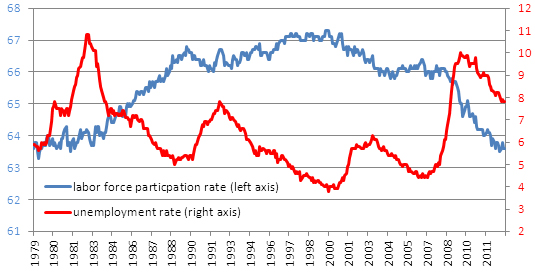

Labor force participation grew steadily across the latter third of the 20th century (driven largely by the entry of women into the labor force), peaking at just over 67 percent in the late 1990s (see Table 1). Some of the decline since then reflects long-term demographic trends, include the rising share of older workers (whose participation rates are lower) and higher rates of post-secondary enrollment. But most of that decline (about two-thirds by one estimate) is cyclical. Indeed, since the onset of the recession, the participation rate has declined more sharply than in any preceding 5-year period. The third measure allows for the natural (demographic) decline, and assumes a labor force participation rate unaffected by the economic conditions.

Table 1: unemployment and labor force participation, 1979-2012

Source: BLS (CPS) Series LNS14000000 and LNS11300000

The result is a jobs deficit (just over 8 million) that is not much less than it was at the recession’s trough, and a jobs threshold that we are unlikely to meet in the next decade.

But even this understates the damage. The December 2007 rates of employment and labor force participation were themselves hangovers from the previous (2001) recession. A better threshold would be that of effectively full employment, akin to the conditions we enjoyed in the late 1990s. As Jared Bernstein and Dean Baker have argued tirelessly, full employment—especially in a setting marked by weak labor standards and a tattered safety net—is the best defense against insecurity and inequality.

The fourth measure, then, uses the unemployment and labor force participation rates (the latter again adjusted to reflect only the cyclical decline) of the late 1990s as our benchmark. This raises the threshold even more. We start the business cycle a couple of million jobs behind, and the gap widens quickly, reaching—and sticking at—a jobs deficit on the order of 11 million.