Ralph Nader is nearly 80 years old. And he is probably as sharp as anyone in Washington half of his age. So where does Linda DePillas get off implying that he is senile in his efforts to keep Fannie Mae and Freddie Mac from being eliminated? The piece begins:

“It’s not often in Washington that you see wealthy, conservative investor types and their lawyers sitting down with professional affordable housing advocates. But on Wednesday morning, anti-corporate crusader Ralph Nader — now stooped and gray, nearing his 80th birthday — brought them together.

“Their cause? Saving Fannie Mae and Freddie Mac from obliteration.

“It’s a herculean effort. Democrats and Republicans don’t agree on much these days, but a broad consensus — from Rep. Jeb Hensarling to the White House — has coalesced around the conclusion that the now-hated housing finance agencies need to be junked, and something else built in their place. A bipartisan bill pushed by Senators Mark Warner and Bob Corker and framed around proposals put forward by center-left groups has taken on an air of inevitability, just waiting for a legislative window to move forward.”

Wow, a “bipartisan bill,” a “broad consensus” of Democrats and Republicans, we probably have not seen so much coming together since the bipartisan support for the deregulation of the 1990s and the celebration of the soaring rates of homeownership during the housing bubble years. That little product of Washington and Wall Street ingenuity now looks destined to cost us more than $24 trillion according to the latest projections from the Congressional Budget Office. What sort of senile old fool could question that?

The Corker-Warner bill touted in the piece makes the financial deregulation of the 1990s looks like a model of cautious reform by comparison. Instead of having Fannie Mae and Freddie Mac, which are now essentially government-run companies, guaranteeing mortgage backed securities (MBS), it would allow private financial institutions to issue MBS with a government guarantee. The only protection is that the investors would have to eat the first 10 percent of the losses.

Goldman Sachs, Citigroup, and the rest of the wall Street gang had no problem passing off their dreck in the housing bubble years when investors could not count on any guarantee. Now the Post is telling us that only a senile old fool would question the wisdom of setting the same crew lose again, but this time being able to tell investors that in a worst case scenario they could only lose ten percent. If questioning the wisdom of that approach is senility, we could use a lot more of it in this town.

Here‘s the more complete picture.

Ralph Nader is nearly 80 years old. And he is probably as sharp as anyone in Washington half of his age. So where does Linda DePillas get off implying that he is senile in his efforts to keep Fannie Mae and Freddie Mac from being eliminated? The piece begins:

“It’s not often in Washington that you see wealthy, conservative investor types and their lawyers sitting down with professional affordable housing advocates. But on Wednesday morning, anti-corporate crusader Ralph Nader — now stooped and gray, nearing his 80th birthday — brought them together.

“Their cause? Saving Fannie Mae and Freddie Mac from obliteration.

“It’s a herculean effort. Democrats and Republicans don’t agree on much these days, but a broad consensus — from Rep. Jeb Hensarling to the White House — has coalesced around the conclusion that the now-hated housing finance agencies need to be junked, and something else built in their place. A bipartisan bill pushed by Senators Mark Warner and Bob Corker and framed around proposals put forward by center-left groups has taken on an air of inevitability, just waiting for a legislative window to move forward.”

Wow, a “bipartisan bill,” a “broad consensus” of Democrats and Republicans, we probably have not seen so much coming together since the bipartisan support for the deregulation of the 1990s and the celebration of the soaring rates of homeownership during the housing bubble years. That little product of Washington and Wall Street ingenuity now looks destined to cost us more than $24 trillion according to the latest projections from the Congressional Budget Office. What sort of senile old fool could question that?

The Corker-Warner bill touted in the piece makes the financial deregulation of the 1990s looks like a model of cautious reform by comparison. Instead of having Fannie Mae and Freddie Mac, which are now essentially government-run companies, guaranteeing mortgage backed securities (MBS), it would allow private financial institutions to issue MBS with a government guarantee. The only protection is that the investors would have to eat the first 10 percent of the losses.

Goldman Sachs, Citigroup, and the rest of the wall Street gang had no problem passing off their dreck in the housing bubble years when investors could not count on any guarantee. Now the Post is telling us that only a senile old fool would question the wisdom of setting the same crew lose again, but this time being able to tell investors that in a worst case scenario they could only lose ten percent. If questioning the wisdom of that approach is senility, we could use a lot more of it in this town.

Here‘s the more complete picture.

Read More Leer más Join the discussion Participa en la discusión

It’s really great that we have National Public Radio. With the interest burden of the debt near a post-war low, and interest rates still at historically low levels, many of us might think that we could focus on other problems. (Netting out interest refunded by the Fed, interest payments are well below 1.0 percent of GDP.) After all, we have an economy that is still down close to 8 million jobs from trend levels, with long-term unemployment rates near post-World War II highs. As a result, millions of children are being raised by parents who lack the means to properly care for them. And of course we are wrecking the planet with greenhouse gas emissions.

Yes, many of us might be thinking about issues along these lines, but thankfully we have NPR to tell us:

“the national debt — how much the country owes from accumulating deficits from year to year — is still a huge problem. At 74 percent of GDP, it’s the highest since 1950, and it’s projected to grow.”

And how do we know this is a huge problem? Well, we heard it from Maya MacGuineas, president of the Committee for a Responsible Federal Budget. (The transcript tells us that MacGuineas “heads the campaign to fix the debt.” It should read “Campaign to Fix the Debt.” This is an organization of corporate CEOs who decided that the debt needs fixing. Fixing the debt is not some objective need that is universally recognized, as this description might imply.)

MacGuineas complains:

“”Because we’ve been so irresponsible for years, our hands are kind of tied as a country.”

Remember, the complaint about irresponsibility here is in reference to the deficit, not the housing bubble. According to the latest estimates from the Congressional Budget Office the collapse of the bubble will cost us more than $24 trillion ($80,000 per person) through the end of its budget horizon in 2024. NPR didn’t really have time to tell us about the housing bubble back in the days when it could have been pricked before its collapse would have been so dangerous. Instead it was telling us about how the deficit was a huge problem.

The theme that we can’t address problems of mobility and growth because of the debt is absurd on its face. The markets are telling us that we can borrow money at near zero real interest rates to fund whatever needs we perceive. If we can actually boost growth and increase mobility with such spending then it is our fear of deficits and debt — the opposite of the claims in this piece — that is the problem, not the debt.

It’s really great that we have National Public Radio. With the interest burden of the debt near a post-war low, and interest rates still at historically low levels, many of us might think that we could focus on other problems. (Netting out interest refunded by the Fed, interest payments are well below 1.0 percent of GDP.) After all, we have an economy that is still down close to 8 million jobs from trend levels, with long-term unemployment rates near post-World War II highs. As a result, millions of children are being raised by parents who lack the means to properly care for them. And of course we are wrecking the planet with greenhouse gas emissions.

Yes, many of us might be thinking about issues along these lines, but thankfully we have NPR to tell us:

“the national debt — how much the country owes from accumulating deficits from year to year — is still a huge problem. At 74 percent of GDP, it’s the highest since 1950, and it’s projected to grow.”

And how do we know this is a huge problem? Well, we heard it from Maya MacGuineas, president of the Committee for a Responsible Federal Budget. (The transcript tells us that MacGuineas “heads the campaign to fix the debt.” It should read “Campaign to Fix the Debt.” This is an organization of corporate CEOs who decided that the debt needs fixing. Fixing the debt is not some objective need that is universally recognized, as this description might imply.)

MacGuineas complains:

“”Because we’ve been so irresponsible for years, our hands are kind of tied as a country.”

Remember, the complaint about irresponsibility here is in reference to the deficit, not the housing bubble. According to the latest estimates from the Congressional Budget Office the collapse of the bubble will cost us more than $24 trillion ($80,000 per person) through the end of its budget horizon in 2024. NPR didn’t really have time to tell us about the housing bubble back in the days when it could have been pricked before its collapse would have been so dangerous. Instead it was telling us about how the deficit was a huge problem.

The theme that we can’t address problems of mobility and growth because of the debt is absurd on its face. The markets are telling us that we can borrow money at near zero real interest rates to fund whatever needs we perceive. If we can actually boost growth and increase mobility with such spending then it is our fear of deficits and debt — the opposite of the claims in this piece — that is the problem, not the debt.

Read More Leer más Join the discussion Participa en la discusión

That’s just in case you are like the vast majority of New York Times readers and have no clue how much $6 billion is. New York Times reporters do not have the ten seconds it takes to go to CEPR’s Responsible Budget Reporting calculator and make their stories informative to readers.

That’s just in case you are like the vast majority of New York Times readers and have no clue how much $6 billion is. New York Times reporters do not have the ten seconds it takes to go to CEPR’s Responsible Budget Reporting calculator and make their stories informative to readers.

Read More Leer más Join the discussion Participa en la discusión

Many people who should know better have been placing far too much emphasis on the weather as an explanation for weak economic data. Cold weather and snow do slow economic activity as people don’t like to go shopping or to restaurants in sub-zero weather or blizzards. But cold weather and snow are normal parts of a winter in the Northeast-Midwest. This means their impact is already included in the seasonal adjustment factors for December and January.

The weather will only have an impact on the data if this winter is notably worse than recent winters. I’m not a meteorologist, but that doesn’t seem so obviously the case to me. In other words, it’s not clear that the weather has had much impact on the data we have been seeing.

I’ll also add that it’s hard to understand the claim from Ian Shepardson that with last year’s seasonal adjustment factors (these change slightly year to year), we would have seen 265,000 jobs rather than the 113,000 reported by the Bureau of Labor Statistics (BLS). In the unadjusted data BLS showed a loss of 2,870,000 this year from December to January compared to a loss of 2,864,000 last year. Last January’s seasonally adjusted jobs number was 197,000.

Given the difference in the unadjusted numbers, at first glance that would look like we would have seasonally adjusted growth of 191,000 using last year’s factors. The actual number will not be simply additive because of differences in seasonal factors across sectors. Still is it hard to believe these differences would get us another 74,000 jobs.

Of course what seasonal factors give, they also take away. (On average, seasonal adjustments have to be zero.) In the seasonally adjusted data we created 149,000 fewer jobs in December of 2013 than in December of 2012. In the unadjusted data the difference was 194,000. If we want to say that we have the wrong seasonal factors so we should be happier about the January numbers, then we would have be more unhappy about weak December numbers.

Many people who should know better have been placing far too much emphasis on the weather as an explanation for weak economic data. Cold weather and snow do slow economic activity as people don’t like to go shopping or to restaurants in sub-zero weather or blizzards. But cold weather and snow are normal parts of a winter in the Northeast-Midwest. This means their impact is already included in the seasonal adjustment factors for December and January.

The weather will only have an impact on the data if this winter is notably worse than recent winters. I’m not a meteorologist, but that doesn’t seem so obviously the case to me. In other words, it’s not clear that the weather has had much impact on the data we have been seeing.

I’ll also add that it’s hard to understand the claim from Ian Shepardson that with last year’s seasonal adjustment factors (these change slightly year to year), we would have seen 265,000 jobs rather than the 113,000 reported by the Bureau of Labor Statistics (BLS). In the unadjusted data BLS showed a loss of 2,870,000 this year from December to January compared to a loss of 2,864,000 last year. Last January’s seasonally adjusted jobs number was 197,000.

Given the difference in the unadjusted numbers, at first glance that would look like we would have seasonally adjusted growth of 191,000 using last year’s factors. The actual number will not be simply additive because of differences in seasonal factors across sectors. Still is it hard to believe these differences would get us another 74,000 jobs.

Of course what seasonal factors give, they also take away. (On average, seasonal adjustments have to be zero.) In the seasonally adjusted data we created 149,000 fewer jobs in December of 2013 than in December of 2012. In the unadjusted data the difference was 194,000. If we want to say that we have the wrong seasonal factors so we should be happier about the January numbers, then we would have be more unhappy about weak December numbers.

Read More Leer más Join the discussion Participa en la discusión

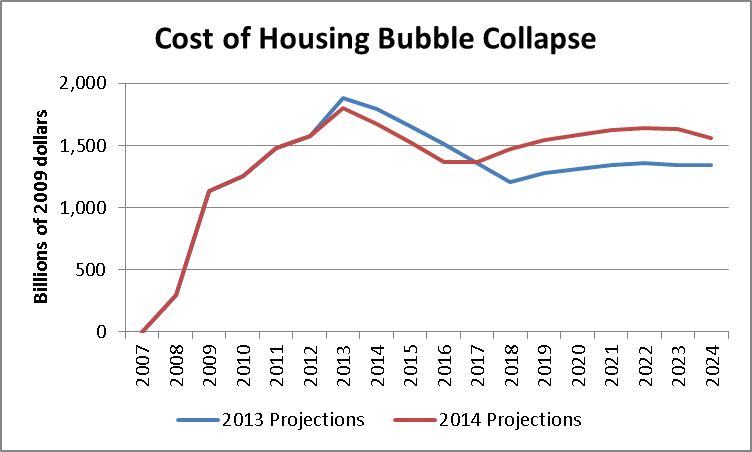

While the Congressional Budget Office’s (CBO) projections of the impact of the Affordable Care Act got the most attention after the release of its new Budget and Economic Outlook, CBO also implicitly raised its estimate of the cost of the crisis created by the collapse of the housing bubble by $1.4 trillion. This is due to the fact that it downgraded its growth projections for later in the decade, for reasons unrelated to the ACA, with the view that more of the impact of the downturn will be enduring long into the future.

The figure below shows the difference between the 2008 projections for annual GDP and the projections from both the 2013 Outlook and the 2014 Outlook. The calculations use CBO’s Long-Term Budget Projections for years beyond the budget horizon. The 2014 projections for GDP are adjusted upward for the negative impact that CBO expects the ACA to have on GDP. The 2014 figure is accordingly raised by 0.5 percent from the CBO projection, the 2015 figure is raised by 0.75 percent, and subsequent years by 1.0 percent. (In effect, these projections assume that policy changes other than the ACA have had a neutral effect on growth.)

The cumulative cost of the collapse through the 2024 budget horizon, measured as a gap between projected output in 2008 and the most recent projections, is now $24.6 trillion, as shown below. This is equal to $80,000 for every person in the United States.

Source: CBO and author’s calculations.

While the Congressional Budget Office’s (CBO) projections of the impact of the Affordable Care Act got the most attention after the release of its new Budget and Economic Outlook, CBO also implicitly raised its estimate of the cost of the crisis created by the collapse of the housing bubble by $1.4 trillion. This is due to the fact that it downgraded its growth projections for later in the decade, for reasons unrelated to the ACA, with the view that more of the impact of the downturn will be enduring long into the future.

The figure below shows the difference between the 2008 projections for annual GDP and the projections from both the 2013 Outlook and the 2014 Outlook. The calculations use CBO’s Long-Term Budget Projections for years beyond the budget horizon. The 2014 projections for GDP are adjusted upward for the negative impact that CBO expects the ACA to have on GDP. The 2014 figure is accordingly raised by 0.5 percent from the CBO projection, the 2015 figure is raised by 0.75 percent, and subsequent years by 1.0 percent. (In effect, these projections assume that policy changes other than the ACA have had a neutral effect on growth.)

The cumulative cost of the collapse through the 2024 budget horizon, measured as a gap between projected output in 2008 and the most recent projections, is now $24.6 trillion, as shown below. This is equal to $80,000 for every person in the United States.

Source: CBO and author’s calculations.

Read More Leer más Join the discussion Participa en la discusión

That is what readers of a piece discussing President Obama’s shift in emphasis from the word “inequality” to “opportunity” will undoubtedly think. The piece notes that President Obama is using the word “opportunity” more and downplaying talk of inequality. It presents comments from several people saying that “inequality” raises the specter of class war and that it eliminates the possibility of compromise with Republicans.

Incredibly the piece presents the Republicans’ official line uncritically, telling readers:

“Republicans generally argue that government should do little; a free market and a growing economy will create opportunity. Their ideas to overhaul education, job-training and safety-net programs often double as budget-cutting initiatives.”

Of course Republicans argue that the government should do lots of things to redistribute income upward, they just don’t highlight the fact that the government is doing these things. For example, they are strong supporters of government granted patent monopolies that increase drug prices by close to $300 billion a year, an amount that is roughly equal to 1.8 percent of GDP and almost four times the SNAP budget. They support keeping in place the protectionist measures that largely insulate doctors and lawyers and other highly paid professionals from the same sort of international competition faced by autoworkers and textile workers.

Republicans support keeping in place a tax code that is littered with tax breaks, the exploitation of which is the primary basis for the existence of the private equity industry. (See my colleague Eileen Appelbaum’s forthcoming book on this topic.) Republicans support a special exemption of the financial industry from the sort of taxes that apply to other industries. This implicitly means higher taxes on other sectors of the economy and allows people to get ridiculously rich in finance. And they support a budget policy that keep millions of people out of work and puts downward pressure on the wages of most workers.

In short, it is absurd to say that the Republicans want the government to do little; they want the government to intervene in huge ways to redistribute income upward. Of course they don’t openly say this, they would much rather pretend that all the policies they support that lead to an upward redistribution of income are just the natural workings of the market. In this way, the NYT has done them a great service in uncritically projecting the Republicans’ romanticized image to readers as reflecting reality. However this completely distorts the relevant issues at play.

The real question is whether either party is prepared to attack the policies that have shifted such a vast amount of income upward over the last three decades. For practical purposes, if these policies are not changed, the agenda on mobility is just silly happy talk and everyone knows it. If the current policies promoting inequality are left in place there is nothing that Washington can do that can affect in more than a trivial way the life prospects of those in the bottom half and especially the bottom quintile of the income distribution.

That is what readers of a piece discussing President Obama’s shift in emphasis from the word “inequality” to “opportunity” will undoubtedly think. The piece notes that President Obama is using the word “opportunity” more and downplaying talk of inequality. It presents comments from several people saying that “inequality” raises the specter of class war and that it eliminates the possibility of compromise with Republicans.

Incredibly the piece presents the Republicans’ official line uncritically, telling readers:

“Republicans generally argue that government should do little; a free market and a growing economy will create opportunity. Their ideas to overhaul education, job-training and safety-net programs often double as budget-cutting initiatives.”

Of course Republicans argue that the government should do lots of things to redistribute income upward, they just don’t highlight the fact that the government is doing these things. For example, they are strong supporters of government granted patent monopolies that increase drug prices by close to $300 billion a year, an amount that is roughly equal to 1.8 percent of GDP and almost four times the SNAP budget. They support keeping in place the protectionist measures that largely insulate doctors and lawyers and other highly paid professionals from the same sort of international competition faced by autoworkers and textile workers.

Republicans support keeping in place a tax code that is littered with tax breaks, the exploitation of which is the primary basis for the existence of the private equity industry. (See my colleague Eileen Appelbaum’s forthcoming book on this topic.) Republicans support a special exemption of the financial industry from the sort of taxes that apply to other industries. This implicitly means higher taxes on other sectors of the economy and allows people to get ridiculously rich in finance. And they support a budget policy that keep millions of people out of work and puts downward pressure on the wages of most workers.

In short, it is absurd to say that the Republicans want the government to do little; they want the government to intervene in huge ways to redistribute income upward. Of course they don’t openly say this, they would much rather pretend that all the policies they support that lead to an upward redistribution of income are just the natural workings of the market. In this way, the NYT has done them a great service in uncritically projecting the Republicans’ romanticized image to readers as reflecting reality. However this completely distorts the relevant issues at play.

The real question is whether either party is prepared to attack the policies that have shifted such a vast amount of income upward over the last three decades. For practical purposes, if these policies are not changed, the agenda on mobility is just silly happy talk and everyone knows it. If the current policies promoting inequality are left in place there is nothing that Washington can do that can affect in more than a trivial way the life prospects of those in the bottom half and especially the bottom quintile of the income distribution.

Read More Leer más Join the discussion Participa en la discusión

The NYT was almost as bad as the Washington Post in its reporting on the farm bill. The NYT gets a few points for explaining how many people would be hit by the cuts in food stamps and what the cuts translated to in dollars per month.

But the main numbers still appeared as just really big numbers. No one knows what $1 trillion in spending means over the next decade and the article offers no context to provide meaning. So, this one will get a good humma, humma, humma, down at the budget reporters’ frat house, but provides almost no information to readers.

The NYT had committed itself to placing these numbers in context more than three months ago. What is going on? It really is not that hard.

The NYT was almost as bad as the Washington Post in its reporting on the farm bill. The NYT gets a few points for explaining how many people would be hit by the cuts in food stamps and what the cuts translated to in dollars per month.

But the main numbers still appeared as just really big numbers. No one knows what $1 trillion in spending means over the next decade and the article offers no context to provide meaning. So, this one will get a good humma, humma, humma, down at the budget reporters’ frat house, but provides almost no information to readers.

The NYT had committed itself to placing these numbers in context more than three months ago. What is going on? It really is not that hard.

Read More Leer más Join the discussion Participa en la discusión

Read More Leer más Join the discussion Participa en la discusión

The Washington Post gave us some good frat boy budget reporting in a front page story on the farm bill this morning. Frat boy budget reporting is when you write a piece that provides no information to the vast majority of readers but lets you go down to the budget reporters’ frat house and give each other the budget reporters’ secret handshake. In this case, the piece told us that the farm bill will cost $956.4 billion over the next decade, it will reduce spending on SNAP by $8 billion and save $16 billion in total.

Yes, this is really helpful. At least 0.1 percent of Washington Post readers have any clue what these numbers mean for the budget over the next decade. It is possible and easy to express these numbers in ways that would be meaningful.

CEPR’s extraordinary Responsible Budget Reporting Calculator would allow any budget reporters to determine in seconds that the total bill is 2.05 percent of projected spending, which immediately would give the vast majority of Post readers a clear idea of the farm bill’s importance to the budget. They could also quickly recognize that the cuts to the SNAP bill are 0.017 percent of projected spending and the total savings on the bill are 0.034 percent of projected spending.

It’s really not hard to do budget reporting in a way that provides information to its audience. However the Post simply chooses not to.

The Washington Post gave us some good frat boy budget reporting in a front page story on the farm bill this morning. Frat boy budget reporting is when you write a piece that provides no information to the vast majority of readers but lets you go down to the budget reporters’ frat house and give each other the budget reporters’ secret handshake. In this case, the piece told us that the farm bill will cost $956.4 billion over the next decade, it will reduce spending on SNAP by $8 billion and save $16 billion in total.

Yes, this is really helpful. At least 0.1 percent of Washington Post readers have any clue what these numbers mean for the budget over the next decade. It is possible and easy to express these numbers in ways that would be meaningful.

CEPR’s extraordinary Responsible Budget Reporting Calculator would allow any budget reporters to determine in seconds that the total bill is 2.05 percent of projected spending, which immediately would give the vast majority of Post readers a clear idea of the farm bill’s importance to the budget. They could also quickly recognize that the cuts to the SNAP bill are 0.017 percent of projected spending and the total savings on the bill are 0.034 percent of projected spending.

It’s really not hard to do budget reporting in a way that provides information to its audience. However the Post simply chooses not to.

Read More Leer más Join the discussion Participa en la discusión