October 31, 2012

Back in the 2000 presidential campaign, then Governor George W. Bush, described his plans for education and raised the famous question “is our children learning?” Unfortunately when it comes to former children who write on economic policy issues, the answer is a resounding “no!”

The Des Moines Registrar editorial encouraging readers to vote for Governor Romney managed to get just about every major aspect of the current economic situation wrong. For beginners, it told readers that:

“consumers must feel more confident about their own economic futures to begin spending on the products and services that power the economy.”

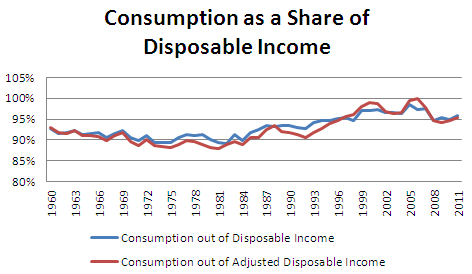

Sorry, folks that one is clearly not a problem. A quick trip to the Commerce Department’s website (Table 2.1, line 34 gives the saving rate, which is the percentage of income not consumed) will tell people that consumers are actually spending a much higher portion of their income than is typically the case. While the consumption share of income is not as high as the stock bubble driven peak of the late 90s or the housing bubble driven peak of the last decade, consumption is higher as a share of income now that it was in the 1960s, 1970s, 1980s, or even the 1990s.

Source: Bureau of Economic Analysis.

Then the editorial told readers:

“A renewed sense of confidence will spark renewed investment by American companies.”

This implies that investment has been seriously lagging. Again, folks who rely on data would not say such silly things. Investment in structures remains somewhat depressed because the bubble in non-residential real estate led to overbuilding in most categories of non-residential structures. Even in Washington, DC, which has escaped the worst of the downturn, there are signs everywhere advertising vacant office and retail space. No one in their right mind starts a big office building project or a new mall when the existing ones are half empty.

The area of investment where we might expect to see the impact of confidence right now is equipment and software. The data do not support the sagging confidence story. If we go back to the Commerce Department website (Table 1.1.5, line 11 divided by line 1) and look at investment in equipment and software as a share of GDP, we find that it is almost back to its pre-recession level. In fact, while it’s below the peaks reached during the Internet bubble, it’s pretty much back to the “morning in America” Reagan era levels.

Source: Bureau of Economic Analysis.

This level of investment is actually quite impressive given that large sectors of the economy still have huge amounts of excess capacity.

If consumption and investment are both pretty much back to normal why is the economy still in the doldrums? The answer is simple, we have nothing to replace the demand that was generated by the housing bubble. The overbuilding of residential housing led to a fall in construction of more than 4 percentage points of GDP (@ $600 billion in annual demand). While housing is creeping back, it will take a long time to work through the excess supply so that builders are again operating at normal levels. There is a similar but less important story with non-residential construction.

The other big part of the story is that while consumption is still healthy, it is below its bubble driven peak. The loss of $8 trillion in ephemeral housing bubble equity has led to a decline in annual consumption of $400-$500 billion. This also will not be easily replaced.

This gets us back to the Register’s other big complaint, the budget deficit. In the short-term, the deficit is the only source of demand holding up the economy. The Register is welcome to dislike government all it wants, but the reality is that if we did not have large deficits right now we would simply have less output and more unemployment. None of Governor Romney’s job creating friends invest based on the government’s decision to cut spending or raise taxes. That doesn’t make any sense and of course we’ve had the chance to test this theory. The U.K. generously agreed to throw its economy back into a recession just so that people in the United States could see that cutting a budget deficit in the middle of a downturn will slow growth and cost jobs. In the longer term we will have to look to get our trade deficit closer to balance to sustain demand, but for the immediate future, the government is the only game in town.

The final fact that all numerate people should know is that we have not had chronic deficit problems. (Both parties have wanted to promote this untruth for different reasons.) In fact, the deficits were relatively modest before the collapse of the housing bubble sank the economy. And they were projected to remain relatively modest as visitors to the Congressional Budget Office website can verify.

Source: Congressional Budget Office.

Source: Congressional Budget Office.

As can be seen, the deficits before the collapse were just over 1.0 percent of GDP and were projected to remain in that range until the expiration of the Bush tax cuts pushed the budget into surplus in 2012. This meant that the ratio of the debt to GDP was falling, we can run deficits of this size literally forever. In short, the tale of out of control deficits is utter nonsense. The large deficits are the result of the downturn caused by the collapsed housing bubble, end of story.

So the Register may still want to endorse Governor Romney for president, but its economic reasoning is 100 percent wrong. It may want brush up on some intro econ so it doesn’t mislead its readers again.

Comments