October 26, 2018

October 26, 2018 (GDP Byte)

By Dean Baker

Nonresidential investment grew at just a 0.8 percent annual rate in the third quarter.

Gross Domestic Product (GDP) grew at a 3.5 percent annual rate in the third quarter, down from a 4.2 percent pace in the second quarter. Consumption was the main factor in third quarter growth, growing at a 4.0 percent annual rate and accounting for 2.69 percentage points of third quarter growth. Nonresidential fixed investment rose by just 0.8 percent, and housing fell at a 4.0 percent annual rate.

Inventory accumulation was a huge factor, adding 2.07 percentage points to growth, as final demand increased at a 1.4 percent annual rate in the quarter. The inventory rise was largely offset by a sharp rise in the trade deficit, which subtracted 1.78 percentage points from growth. In nominal dollars, the trade deficit stood at $646.5 billion in the third quarter, up from $557.3 billion in the same quarter last year.

Vehicles sales are fading as a source of growth, adding just 0.09 percentage points in the quarter. Nonetheless, durable goods still added 0.48 percentage points to third quarter growth, with televisions being the largest single factor.

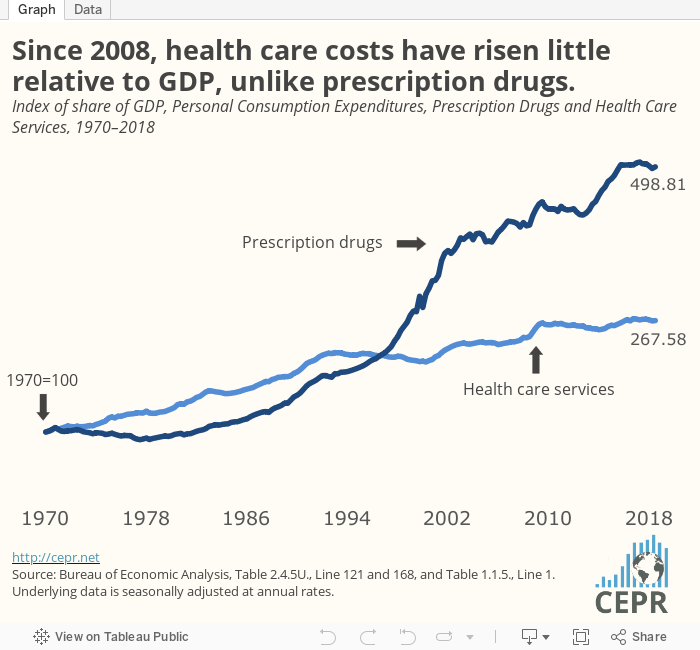

Nondurable consumption rose at a surprisingly rapid 5.2 percent rate, adding 0.72 percentage points to growth. Spending on prescription drugs was the biggest part of the story, rising in real dollars at an 8.6 percent annual rate. Spending on health care services also increased rapidly in the quarter, rising in real terms at a 4.6 percent annual rate and contributing 0.52 percentage points to the quarter’s growth.

The sharp rise in spending on health care services is somewhat of an anomaly, as growth has slowed sharply since 2008. The growth in prescription drug spending is also a jump from recent quarters, although it is less out of line.

The slowdown in nonresidential investment is the biggest story in the third quarter data, since the rationale for the corporate tax cut was supposed to be its impact on investment. Equipment investment grew at a 0.4 percent annual rate, while structure investment actually fell at a 7.9 percent rate. This is striking, since structures are longer-term investments that should be more sensitive to the higher post-tax cut rate of return. Investment in intellectual products grew at a modest 7.9 percent rate, with software being the major factor.

The 4.0 percent drop in residential construction was the third consecutive decline. This drop-off is likely to continue as higher mortgage rates are crimping demand. The September data showed a large falloff in sales of new homes and, more importantly, the highest inventory-to-sales ratio since early 2011. Since there was never a boom in housing like the bubble years, we are not at risk of the same sort of collapse, but it is likely to be a drag on growth in coming quarters.

The jump in the trade deficit is a predictable outcome of both rapid GDP growth and a higher dollar. The dollar has risen by more than 6.0 percent in real terms against the currencies of our trading partners, making US goods and services considerably less competitive internationally.

The government sector added 0.56 percentage points to third quarter growth. State and local government spending was the main factor, adding 0.35 percentage points to growth, the largest contribution since the first quarter of 2016.

One striking item in this report is a slowing of inflation. The core personal consumption expenditure (PCE) deflator (inflation measure targeted by the Federal Reserve) increased at just a 1.6 percent annual rate in the quarter. In spite of the low unemployment rate, there is little evidence of any acceleration in the inflation rate.

One other item worth noting in this report is that third quarter growth likely implies another quarter of strong productivity growth. Value-added in the nonfarm business sector rose at a 4.1 percent annual rate. With hours rising at close to a 1.0 percent rate, we should see productivity growth of close to 3.0 percent, which follows second quarter growth of 2.9 percent.

Productivity data are hugely erratic, so this may just be a blip. But it is possible that the tight labor market is forcing employers to find ways to better use their workers. More rapid productivity growth would be a great outcome, but it is important to point out that this is not a tax cut story. Nonresidential investment is up just 6.4 percent from the prior year, an amount that could only explain a tiny boost in productivity.

The data for third quarter GDP are pretty much the textbook story for a tax cut when the economy is near full employment. We saw a jump in consumption that is being offset by drops in housing and investment and a rising trade deficit. With the fourth quarter almost certain to be weaker, the growth boom looks to be even shorter than had been generally expected.