February 17, 2013

Thomas Friedman is once again mass marketing misinformation on economics, something that he does all too frequently. Just about everything in the piece is 180 degrees wrong: the Friedman standard.

It begins by telling us that Tim Cook and Apple are sitting on $137 billion that they could be investing:

“Apple is currently sitting on $137 billion of cash in the bank. There are many reasons Apple has not spent its cash horde, but I’ll bet anything that one of them is the uncertain economic and tax environment in this country. Think about how much better we’d all be if Apple, and the many other companies sitting on cash, felt confident enough in the future to spend it. These are the most dynamic companies in the world. They don’t need any government help to innovate.”

Okay, Apple is so uncertain about the economic and tax environment in the U.S. that they don’t invest. (Funny how that works since they sell largely to a world market of which the U.S. is a substantial part, but not the majority.) Friedman goes on:

“Message: There is no doubt our economy is primarily being held back by the deleveraging and drop in demand that resulted from the 2008 financial crisis. But they are being reinforced today by uncertainty and worry that we do not have our political house in order and, therefore, our tax, regulatory, pension and entitlement frameworks are all in play. So businesses, investors and consumers all hold back just enough for us not to be able to move the growth and employment meters with any robust momentum.”

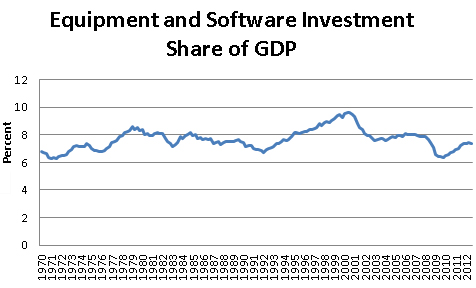

Okay, let’s imagine that one of Friedman’s cab drivers had access to the Internet and could go to the National Income and Product Accounts that the Commerce Department posts. The cab driver would explain to Friedman that investment in equipment and software is actually pretty healthy. Measured as a share of GDP it is almost back to its pre-recession level. Furthermore, apart from the tech bubble days of the late 90s it has never been much higher than it is today. Here’s the picture.

Source: Bureau of Economic Analysis.

In short there is no reason to expect investment to be much higher than it is currently. It doesn’t appear that uncertainty is very important in this picture.

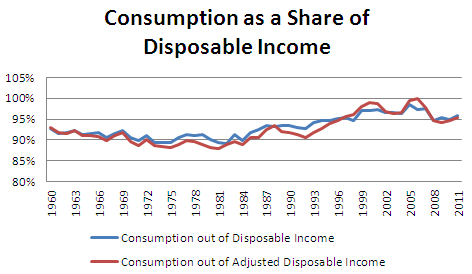

Friedman’s cab driver would then explain to him that he is also wrong about consumption. Consumers are actually spending at a high rate relative to their income, not the low rate he seems to believe. The Commerce Department also has data on consumption and saving rates (Table 2-1, the story on adjusted disposable income has to do with the statistical discrepancy in the national accounts).

Source: Bureau of Economic Analysis.

While consumption is not as high relative to disposable income as it was at the peak of the housing bubble, it is still much higher than its post-war average. It would be amazing if the loss of $8 trillion in housing bubble wealth did not reduce consumption. In the years before the stock and housing bubbles began to propel consumption the saving rate averaged more than 8.0 percent. Currently the saving rate is near 4.0 percent implying that people are consuming at an unusually rapid pace now that the wealth created by both bubbles has disappeared.

If the downturn is not being driven by lack of investment or lack of consumption what could explain the continuing weakness of demand? If our cab driver goes over to the Census Bureau’s data on vacancy rates she can explain to Friedman that vacancy rates, while down from the peaks in 2009-2010, are still near record highs. This continues to depress housing construction, which is down by close to 4 percentage points ($600 billion in annual demand) from its bubble peaks.

Our cab driver could also explain to Thomas Friedman how a trade deficit of 4 percent of GDP (also $600 billion in annual demand) affects the economy. The national income accounting that students learn in intro economics is that GDP = consumption + investment +government spending + net exports. If we have a trade deficit of $600 billion then we need to have the other categories fill that gap to get the economy back to full employment.

In the last decade the demand created by the housing bubble filled the gap created by the trade deficit. In the 1990s the demand created by the stock bubble filled the gap created by a somewhat smaller trade deficit. Now we have nothing to fill the gap. And if anything Friedman’s remedies go in the wrong direction.

Friedman calls for investment in infrastructure and early childhood education — good things — but then he tells readers:

“That would have to be married with a long-term fiscal restructuring, written into law, that slows the growth of both Social Security and Medicare entitlements, along with individual and corporate tax reform. Obama has hinted at his willingness to do all of these. They should be agreed upon in 2013 and phased in gradually, starting in 2014. … Otherwise, we will have little in reserve to fight the next economic crisis or 9/11 or Hurricane Sandy.”

Let’s see, we know that we are running up against the limits where there is nothing in reserve because of the 2.0 percent interest on 10-year treasury bonds? Perhaps it is the evidence from Japan where a debt to GDP ratio of more than 200 percent (three times the size of our ratio) means that the Japanese government must pay 1.0 percent interest on its long-term government debt. Yeah, well who needs evidence when you’re Thomas Friedman?

Friedman just keeps getting better:

“Our choice today is not ‘austerity’ versus ‘no austerity.’ That is a straw man argument offered by both extremes. It’s about whether we phase in — in the least painful way possible — a long-term plan that balances our need to protect the most vulnerable in this generation while funding the most opportunities for the next generation, and still creating growth. We can’t protect both generations in full anymore, but we must not sacrifice one for the other — favoring nursing homes over nursery schools — and that’s what we’re on track to do.”

You have to love the line:

“We can’t protect both generations in full anymore.”

Somehow Friedman missed the fact that the problem we are facing is a lack of demand. We need people to spend more not less. How does austerity reduce unemployment and get the economy back to full employment? It hasn’t worked in Ireland, Greece, Spain, the United Kingdom or anywhere else that can be identified. How on earth does the fact that we now face a huge gap in demand mean that we are less well-situated to “protect both generations.” (Of course he doesn’t say anything about income distribution.)

Again, if Friedman could be taught some intro economics it would be hugely helpful here. Suppose Friedman gets his wish for a grand bargain and everyone working today knew that they would be seeing sharply lower Social Security and Medicare benefits in the future. All of those consumers who Friedman thinks are paralyzed by uncertainty will suddenly realize that they can be certain that they will need more money to support themselves in retirement because the Thomas Friedmans of the world have taken away their Social Security and Medicare.

Insofar as possible, these people would drastically increase their savings. That means cutting back their consumption. Now that should lead to a rip-roaring recovery.

Okay, now for the teaching part of this post. We know that Thomas Friedman gets most of the information for his columns from cab drivers. Print out copies of the graphs here on the investment share of GDP and consumption as a share of disposable income. Next time you have to take a taxi be sure to share them with the driver. If enough people do this, at some point Friedman will come into contact with a cab driver who can show him the graphs. Then he may learn a little economics and we would no longer have to see painfully wrongheaded columns on the economy in the Sunday NYT.

Comments