August 16, 2012

In a Washington Post column today, Kevin Hassett and Glenn Hubbard, two of the top economists on Governor Romney’s economic team, rightly take President Obama to task for blaming the weakness of the economy since the downturn on the financial crisis. They cite a recent study from the Federal Reserve Bank of Cleveland as showing that recoveries following financial crises tend to be stronger not weaker than other recoveries.

While there are some questions that can be raised about this study (was the financial crisis in the 1990 recession really comparable to what we saw in the fall of 2008?) the basic point seems right. After all, we do know how to set an economy in motion again following a financial crisis. Argentina managed to regain all the ground lost after a complete financial meltdown in December of 2001 in just 1.5 years. Our financial policy crew can’t be that much less competent than the folks calling the shots in Argentina. The idea that a financial crisis puts a mysterious curse on an economy was always more than a bit suspect.

However the Cleveland Fed study doesn’t quite say that this recovery should be like any other recovery, as Hassett and Hubbard imply. The study goes on to note the extraordinary weakness in housing in this recovery and point out that this weakness could explain much of the weakness of the recovery.

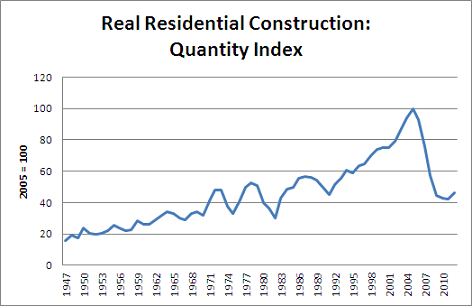

While the study notes that there are questions of causation (a weak recovery could lead to weakness in housing), there can be little doubt that if residential construction had returned to its pre-recession level, as had been the case by this point in all prior post-war recoveries, the economy would be back near full employment.

Source: Bureau of Economic Analysis.

Of course it is not hard to understand why housing has not recovered. The massive over-building of housing during the bubble years lead to an enormous over-supply of housing, which shows up in the data as a record vacancy rate in the years 2006-10. In the last couple of years the vacancy rate has begun to decline which can explain the recent uptick in housing over the last few quarters.

This housing story explains why we should have expected a long and drawn out recovery. There is no easy way to replace the massive loss in demand associated with the collapse of the housing sector. And, it is hard to blame the collapse on President Obama, since the overbuilding took place in the years 2000-2006 and the collapse was already well underway at the point where he took office.

The housing story also puts a kink in the three phases of stimulus story that Hassett and Hubbard outline, where the stimulus becomes contractionary when it is withdrawn after a short initial boost, and then slows the economy further after recovery as a result of a higher future tax burdens. The implication of the housing crash story is that we didn’t want a short initial boost, but rather needed a longer term stimulus that could sustain demand until some other component of consumption could fill the gap.

Obviously Hassett and Hubbard want us to believe that additional investment from the tax cuts proposed by Governor Romney would do the trick, however there is little evidence to believe that they would make much difference. With investment in equipment and software already pretty much back to its pre-recession share of GDP, we would have to see an unprecedented explosion in this category of investment to come close to making up the gap created by the falloff in residential construction. That doesn’t seem likely.

Ultimately we will need an increase in foreign demand, meaning a lower trade deficit, to fill the gap. This will require a lower valued dollar which will make U.S. goods more competitive internationally. Unfortunately, neither candidate seems willing to make the case for a lower valued dollar, which means that we can probably expect a weak economy for many years into the future, regardless of who gets elected.

Comments