Job Growth Remains Strong as Wage Growth Settles Within Inflation Target

The annual rate of wage growth over the last three months was just 3.9 percent.

The economy added 261,000 jobs in October, somewhat faster than most analysts had expected. Despite the rapid job growth, unemployment edged up slightly to 3.7 percent. Perhaps most importantly, it seems wage growth is settling down to a level consistent with the Fed’s 2.0 percent inflation target. Over the last three months, it has increased at a 3.9 percent annual rate. That compares to a 3.4 percent rate in 2019, when inflation was comfortably below the Fed’s target.

Job Growth Led by Health Care and Manufacturing

Job growth was strong across sectors, but it was especially strong in health care and manufacturing. Health care added 52,600 workers in October, and it has added 298,800 workers since May. This is largely catch-up since the sector’s employment had lagged earlier in the recovery. It is now 0.5 percent above the pre-pandemic level.

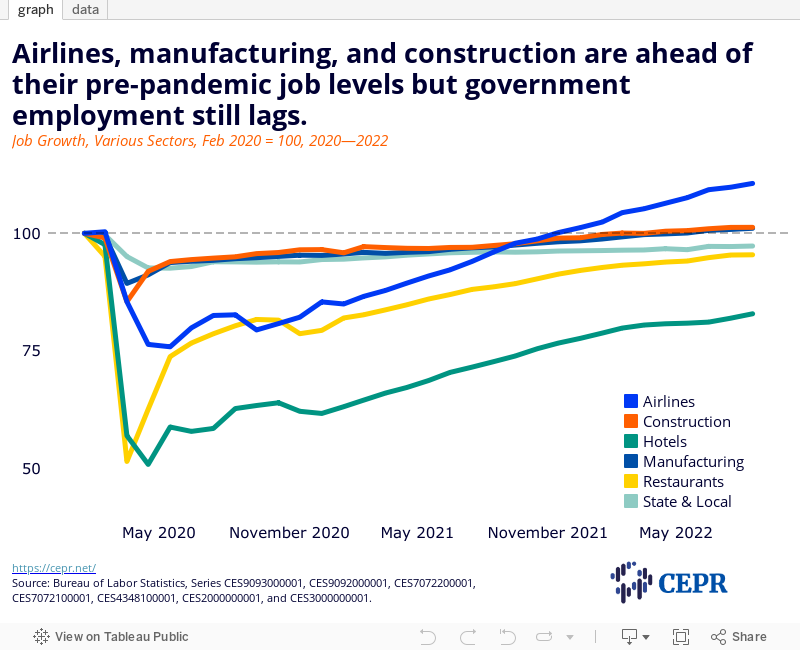

Manufacturing added 32,000 jobs in October, and employment in the sector is now 1.1 percent above the pre-pandemic level. Manufacturing is usually hit hard in a recession, but to date does not seem to have been much affected by the Fed’s rate hikes.

Construction Employment Edges Up, Jobs Related to Mortgage Financing Fall

Higher interest rates have certainly taken a toll on construction, as is most evident in the plunge in housing starts. Nonetheless, employment in the sector increased by 1,000 in October, with residential construction showing a small gain. Employment is now 1.3 percent above pre-pandemic levels. Workers are still needed to finish the many homes that are still under construction.

The impact on the credit intermediation sectors that are involved in mortgage issuance is easier to see. The number of people working in these sectors fell by 4,400 in October and is now down 36,600 from its April peak.

Airlines Add Jobs, Internet Retailers Lose Jobs

The airline industry added 4,200 jobs in October. Employment is now 10.6 percent above its pre-pandemic level, even though air travel is still below pre-pandemic levels. Employment at Internet retailers fell by 300 in October, as people are switching back to in-store shopping and also buying fewer goods. It is now down 0.6 percent from its peak last November, but still 10.6 percent above the pre-pandemic level.

Sectors Having Trouble Hiring Are Now Adding Jobs

Nursing homes added 4,100 jobs in October, while childcare centers added 4,900. Employment in the sectors is still down by 13.7 percent and 8.4 percent, respectively. The low pay in these sectors have made it difficult to get workers.

Local governments added 29,000 jobs in October, while state governments lost 7,000. They are now 3.3 percent and 1.1 percent below pre-pandemic employment levels, respectively.

Restaurants added just 6,000 jobs in October, but this followed an increase of 69,000 in September. This is likely just an error in the data rather than a sharp plunge in job growth. Employment is still 4.6 percent below the pre-pandemic level. Hotels added 19,900 jobs in October, but employment is still 17.1 percent below its pre-pandemic level.

Women Accounted for 66.1 Percent of Payroll Employment Growth in October

Women again accounted for the bulk of payroll job growth in October. They have accounted for 59.3 percent of job growth since May. They now are 49.91 percent of payroll employment. There were some months before the pandemic when women held more than 50.0 percent of payroll jobs.

Weekly Hours Stable in October

Average weekly hours were stable at 34.5 in October. This is down from a peak of 35.0 earlier in the recovery. This is another sign of the labor market normalizing. It suggests employers are not making workers put in more hours due to an inability to hire new workers.

Wage Growth Nears Noninflationary Pace

The annual rate of wage growth over the last three months is just 3.9 percent. This rate is very close to being consistent with the Fed’s 2.0 inflation target. (It is somewhat higher at 4.4 percent, using my preferred measure of taking the average wage for the last three months, compared to the average of the prior three months.)

Hourly wage growth was 3.4 percent in 2019, when inflation was comfortably below the Fed’s 2.0 percent target. By this measure, the Fed’s work is largely done.

Labor Force Participation Edges Down, Prime Age Participation Drops 0.2 Percentage Points

The overall labor force participation rate edged down 0.1 percent to 62.2. The participation rate for prime age workers fell 0.2 percentage points to 82.5 percent. This is 0.6 percentage points below the pre-pandemic peak, but equal to the average for 2019.

Share of Unemployment Due to Voluntary Quits Falls

The percentage of unemployment due to voluntary quits fell sharply in October to 14.6 percent. This number is erratic, but the October figure is consistent with a strong, but normal labor market.

Employment Rate for Workers with Disabilities Hits a New Record High

The employment rate for people with disabilities rose to 22.0 percent in October. This is a new record high. This is likely due to a combination of a strong labor market and a huge expansion in opportunities for work from home.

Average Duration of Unemployment Spells Rises

For the first time since April, both the average duration of unemployment spells and the share of long-term unemployed (more than 26 weeks) rose. The average duration rose from 20.2 weeks to 20.8 weeks, while the share of long-term unemployed rose from 18.5 percent to 19.5 percent. This is consistent with the modest rise in recent weeks in the number of people receiving unemployment benefits.

Strong Jobs Report with Inflationary Pressures Waning

On the whole, this is a very positive report. The job growth is somewhat higher than can be sustained over the long term, but not hugely so. Most importantly from an inflation perspective, wage growth is now very close to being at a noninflationary pace. Other items in this report, such as the drop in the share of unemployment due to voluntary quits and the stabilization of average weekly hours at pre-pandemic levels, are also consistent with a strong, but normal labor market.

We should never make too much of a single month’s data, but as the rate of wage growth falls back near a noninflationary pace, there is a reasonable case for the Fed pausing rate hikes to get a better picture of their impact to date.