March 25, 2018

Neil Irwin had an interesting piece arguing that Trump is fighting the last battle on trade in worrying about imports of steel and aluminum. His main point, that the millions of jobs we lost in manufacturing to trade in the last decade are not coming back, is largely correct. But there are a few points worth adding.

First, it would be worth having a little honesty about the impact of trade on the country’s workers. It is standard wisdom in political circles to say that trade really wasn’t what caused job loss in manufacturing, the real cause of job loss was productivity growth. This is true, but only in a way that is incredibly misleading.

Suppose a factory that was the major employer in a small city burned down, leaving all the workers unemployed. An economist can truthfully say that the major cause of the loss of manufacturing jobs in the city was productivity growth since over the last five decades the city almost certainly lost more manufacturing jobs from productivity growth than due to fire. At the same time, the people who are newly out of work are 100 percent right in blaming the fire.

This pretty well describes how many economists have been talking about the impact of trade in the last decade. Manufacturing has been falling as a share of total employment since the 1970s, but the total number of jobs in manufacturing had changed little, apart from cyclical ups and downs, until our trade deficit exploded in the last decade. (The sharp rise in the trade deficit actually began in 1997, but its impact was offset by the late 1990s boom.) In December of 1970, there were 17,300,000 jobs in manufacturing. In December of 2000 there 17,180,000, a drop of just 120,000. By comparison, in December of 2007, before the start of the Great Recession, manufacturing employment was down to 13,750,000, a drop of 3,430,000 jobs in just seven years.

This was overwhelmingly due to the rise in the trade deficit, which peaked at almost 6.0 percent of GDP in 2005 and 2006. We were seeing productivity growth in manufacturing during this whole time, so that was not something that was new in the years 2000 to 2007. What was new was the large trade deficit. The manufacturing job loss also had a secondary impact on communities across the Rust Belt where it was a major employer.

In addition, there was the macroeconomic problem created by this trade deficit. The deficit created an enormous gap in demand that could not be easily filled. This is essentially the story of “secular stagnation” which has become popular in mainstream economic circles in the years since the Great Recession.

In the years leading up to the recession, the demand gap was filled by demand created by the housing bubble. When the bubble burst, there was no easy way to fill this gap. We partially filled it with budget deficits. More recently the wealth effect from run-ups in stock and housing prices have spurred consumption almost back to housing bubble peaks. And, the trade deficit, at roughly 3.0 percent of GDP, is down from its pre-recession peak.

It is worth noting that a lower trade deficit will still be a help to the labor market in that it will bring back relatively high-paying jobs in manufacturing. While there is little prospect for bringing back the millions of jobs lost in the Rust Belt in the last decade, a lower trade deficit could mean 1–2 million more manufacturing jobs, which would provide a substantial boost to the labor market.

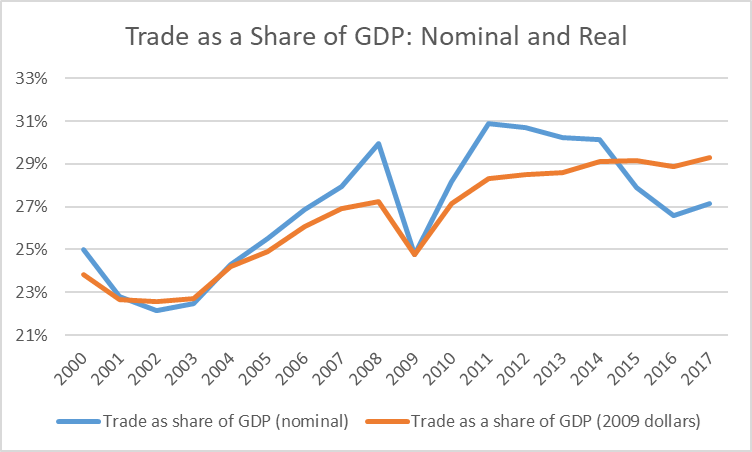

The second point is that Irwin repeats a misleading tale of deglobalization that is getting currency in many circles. The article includes a graph showing trade rising sharply as a share of world GDP until 2007. From that point forward it stagnates and even drops slightly between 2013 and 2015, the last year in the graph.

The reason this is misleading is that much of the run-up to the 2007 peak was driven by higher commodity prices. Commodities like oil and wheat comprise a substantial share of world trade. These prices were soaring just before the recession, with oil peaking at $150 a barrel in 2008. Oil and other commodity prices have since fallen sharply, which substantially reduces the trade share of world GDP.

This story can be seen if we compare the trends in the trade share of US GDP using nominal prices and 2009 dollars. As can be seen, measured in nominal dollars the trade share goes from 25 percent of GDP in 2000 to a peak of 30 percent in 2008. It plummets in the recession, but then rises back to a new peak of 31 percent in 2011, but then falls back to 27 percent in 2017.

Source: Bureau of Economic Analysis.

By contrast, the share using 2009 dollars shows a much more even path of increase. It goes from 24 percent in 2000 to a peak of 27 percent in 2008. After plummeting in the recession, it then resumes its increase, standing at just under 30 percent in the most recent data.

There is no story of deglobalization in these data. It doesn’t make much sense to say the world is less open to trade because commodity prices are falling.

Finally, Irwin correctly notes that the new trade agenda focuses on areas like intellectual property and Internet privacy. However, he doesn’t mention that there are huge within nation conflicts on these issues.

For example, most of us have little reason to want to see Pfizer and Microsoft’s patents and copyrights get longer and stronger either internationally or domestically. Nor do we have a reason to want to see trade deals that make it more difficult for governments to regulate Facebook and Google’s use of its users’ data.

These areas have been a central focus of the Trans-Pacific Partnership and other trade deals, but the negotiation process has been carried on largely outside of the public’s purview. While Pfizer and Facebook have had their seats at the table, the public has been shut out.

It would be great if Trump’s rejection of the Obama administration’s trade agenda led to a more open debate on these topics. That undoubtedly is not Trump’s intention, but it may nonetheless be the outcome of his actions.

Comments