May 11, 2015

You have to admire Niall Ferguson. There aren’t many people who are willing to write lengthy diatribes on topics on which they seem to know next to nothing, but some would say that is the definition of a Harvard professor.

Anyhow, he apparently believes that the victory of the Conservative Party in the U.K. election last week showed that he was correct to endorse their austerity policy and that Paul Krugman was wrong to criticize it. If he was familiar at all with the literature on the impact of the economy on elections he would know that elections are largely determined by the economy’s performance in the last year before an election, not an administration’s entire term. And, since the conservatives relaxed their austerity in the last two years (as had been widely noted long before the election), the economy was not performing badly in the immediate lead up to the election.

Ferguson’s piece presents a cornucopia of silly mistakes, which I don’t have time to address, but I will give my favorite:

“On more than one occasion during the crisis, Krugman applauded Gordon Brown for injecting capital directly into the British banks rather than relying on purchases of “troubled assets,” the initial thrust of the Troubled Asset Relief Program in the United States. In October 2008, Krugman engaged in the kind of sycophancy that usually indicates a man angling for a knighthood:

‘Has Gordon Brown, the British prime minister, saved the world financial system? … The Brown government has shown itself willing to think clearly about the financial crisis, and act quickly on its conclusions. …. Governments [should] provide financial institutions with more capital in return for a share of ownership … [a] sort of temporary part-nationalization … The British government went straight to the heart of the problem – and moved to address it with stunning speed.’

“TARP has of course proved far more successful than the UK’s nationalization of too-big-to-fail behemoths like RBS.”

The small detail that Ferguson apparently missed is that TARP also went the route of giving the banks capital in exchange for share ownership in the form of the purchase of shares of preferred stock. At the time, Plan A from the Bush administration was to directly purchase the bad assets from the banks (hence the name “Troubled Asset Relief Program”). Krugman and others argued that the better route was to give the banks capital, which is what TARP eventually did, following Gordon Brown’s lead. (I personally favored letting the market work its magic and then pick up the pieces after the Wall Street behemoths were buried in the ground.) In other words, Ferguson is bizarrely holding up TARP as an alternative course to the path set out by Brown, when in fact it followed the path set out by Brown.

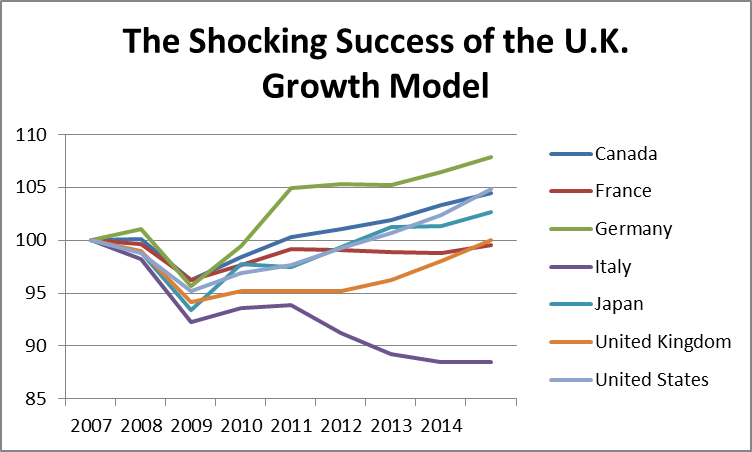

But the real story is the overall performance of the U.K. economy, which Ferguson somehow thinks was extraordinary. The data beg to differ, even if the U.K. has done better in the last couple of years as the government relaxed its austerity. Here is the per capita GDP record of the G-7 economies since the crisis.

Source: International Monetary Fund.

As can be seen, the U.K. ties France for fifth place, only beating out Italy for last place. If we treat 2010 as the start point, it managed to close the gap with France in the next four years (which also was forced to pursue austerity since it was in the euro zone), but fell further behind Germany, Japan, Canada, and the U.S.

In 2014, seven years after the beginning of the crisis, per capita GDP in the U.K. was virtually identical to what it had been in 2007. By comparison, per capita GDP in the U.S. in 1988 was 20.1 percent higher than it had been at start of the 1981 recession. In 1997 it was 12.8 percent larger than it had been at the start of the recession in 1990. It would require some extraordinary affirmative action for conservative politicians to follow Ferguson and declare the Cameron record a success.

Addendum

For folks who thought I was being unfair to use 2010 as a reference point, since Cameron only took office mid-year, you’re right. The OECD has the quarterly data. The UK economy grew at a 2.0 percent annual rate in the first quarter and a 4.0 percent rate in the second quarter when Cameron took office. This slowed to 2.6 percent in the third quarter and 0.1 percent in the fourth quarter. So taking the year as a whole as the start point for Cameron is undoubtedly too generous.

I should also explain that there is a reason for using the pre-recession level of output as a reference point. In the old days (i.e. before the pathetic recovery from this downturn) economists expected economies to bounce back quickly from a recession, making up the ground lost in the recession. This is why we had years of 5-7 percent growth following the steep downturns in 1974-1975 and 1981-1982. This recession has been different in that we have not seen a steep bounce back in any country. I feel it is appropriate to apply normal economic standards to evaluate policy performance instead of using affirmative action for inept policymakers.

Comments