September 19, 2016

Europe and the United States both shifted their fiscal policies from stimulus to austerity in 2011. Most economists see this as a major factor explaining the weak recovery from the 2008–2009 recession. Incredibly, in his latest Washington Post column assessing the weakness of the economy, Robert Samuelson never mentions the shift to austerity.

Actually, the column is more than a bit confused since it starts by making the case that the Fed actually should be raising interest rates since the economy is now at or near full employment. This is an argument that the economy is now strong and risks inflation due to too much demand.

But most of the piece then turns to the argument that central banks can’t boost the economy the way they had in the past. He tells readers:

“One explanation lies in the high and unsustainable debts that fueled the Great Recession. “Debt recoveries are not the same as ordinary business cycle recoveries,” Harvard economist Carmen Reinhart [yes, that is Reinhart of the famous Reinhart and Rogoff Excel spreadsheet error that helped launch worldwide austerity because they couldn’t be bothered to check their calculations] recently told a conference at the Peterson Institute. Consumers and companies cut debt loads and rebuild savings. Lenders are more restrained in their lending; borrowers are more restrained in their borrowing. All this curbs spending.

“A variant — one often made by this reporter — is that the recession’s severity, almost entirely unanticipated by economists, business leaders and government officials, has made households and enterprises more precautionary and protective. They save more and spend less to shield themselves against future slumps and unpredicted calamities.”

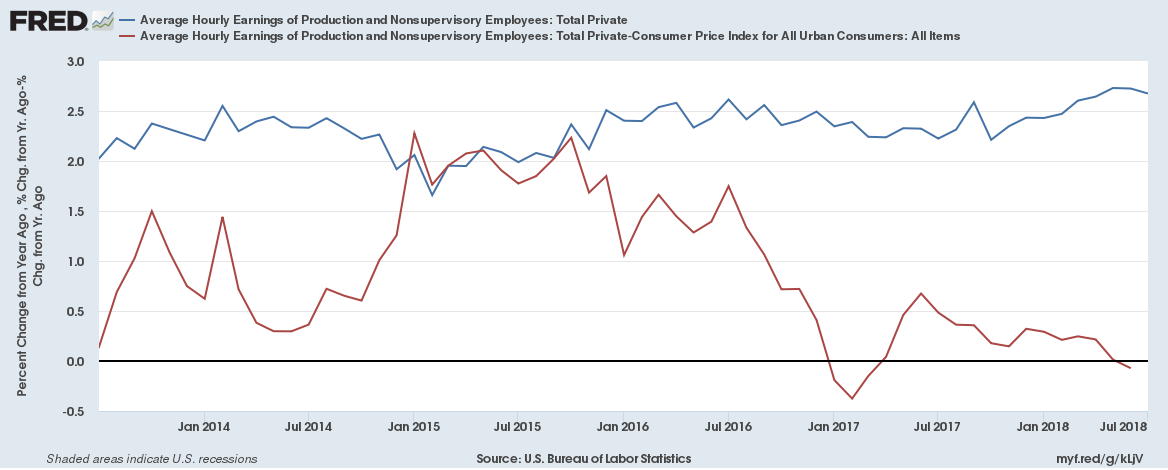

The problem with both variants of the “reluctant to spend” story is that neither households nor businesses were especially reluctant to spend, as those with access to Commerce Department data know. The figure below shows consumption as a share of GDP. As can be seen, it has been near post-war highs in the years since the recession, as the savings rate has been unusually low. The investment share of GDP has also been comparable to the pre-recession level. Housing construction has been depressed — for the mysterious reason that there was severe overbuilding in the bubble years.

In addition to the austerity which sharply reduced demand from the government the other factor depressing demand (which is not allowed to be mentioned in the pages of the Washington Post) is the trade deficit. The U.S. is still running a trade deficit of roughly $500 billion a year (@ 2.8 percent of GDP). This has the same impact on demand in the economy as if government spending were cut by an additional $500 billion. The demand generated by the housing bubble filled this demand gap, but in the absence of the bubble, there is nothing to fill the gap.

All of this is pretty simple and straightforward, but our elite types don’t like us talking about the trade deficit as a problem. So, we end up with folks like Robert Samuelson telling us it is all very mysterious.

Comments