Article

Only Radical Changes Will Make Rents Affordable

Article

The affordable rental housing situation in the US has been in crisis from as early as the 1960s, and it has only worsened over time. Without a radically new approach, we can not expect to solve the problem. The US needs to adopt European-style social housing and also make rental assistance an entitlement.

Social housing is not-for-profit affordable housing that includes the working and middle classes. Unlike social housing, public housing in the US shelters impoverished families in government-owned housing often without the funds necessary for maintenance, cleanliness, and safety.

It is important to make rental assistance an entitlement because in the US three quarters of families eligible for rental assistance receive no government help. With these two strategies, the US can provide more affordable, high quality rental housing for all renters.

Last month the Biden administration presented its Housing Supply Action Plan. The plan takes a multipronged approach to address the inadequate supply of affordable housing for renters and owners. If approved by Congress, it would have some positive effects. But the plan is not big enough to address the scale of the problem.

Its centerpiece is a call to Congress to finance “more than 800,000 affordable rental units by expanding and strengthening the Low-Income Housing Tax Credit.” The National Low-Income Housing Coalition estimates that there is a shortage of 7 million rental units for households in poverty. Even if the Biden plan is fully implemented, it is not likely to eliminate the affordable rental housing crisis.

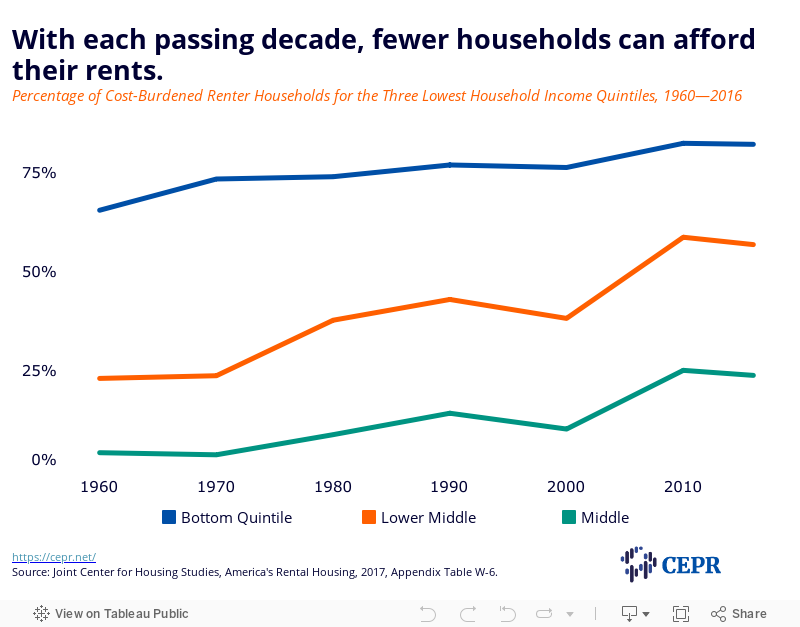

The Biden administration is relying on the current toolkit of federal policies. The problem is that federal affordable rental housing policies favor the needs of the corporate real estate industry and investors over the needs of renters. The figure shows that in 1960, 65.6 percent of renting households in the bottom income quintile were cost-burdened, which means that renters paid more than 30 percent of their income on housing costs — the recommended upper limit. In this discussion, rents that lead to cost burdens are not considered affordable.

By the cost-burdened measure, US rental housing policy failed the bottom income quintile in 1960. The situation has only worsened. In 2016, 82.3 percent of the bottom quintile renters were in cost-burdened homes. The trend has risen over time with only minor fluctuations.

The lack of affordable rental housing is not just a crisis for the poor. The figure also shows the expansion of cost-burdened renters into higher income quintiles. For the lower middle quintile, the rate of cost-burdened renters increased from about a quarter to more than half from 1960 to 2016. Even solidly middle-class households in the middle income quintile increased their rate of living in cost-burdened rental housing from a small 4.3 percent to nearly a quarter by 2016.

This trend of increasing unaffordability has continued. The Joint Center for Housing Studies found that “the number of units affordable to renters with incomes up to $30,000 fell by 1 million from 2018 to 2019.” The US Department of Housing and Urban Development’s category of “worst case housing needs” increased by 50,000 from 2017 to 2019. Households in the category of worst case housing needs “have incomes at or below 50 percent of the area median, do not receive housing assistance, and either pay more than half of their incomes for rent or live in severely inadequate conditions, or both.” In 2019, there were 7.8 million households in these desperate living situations.

The Low-Income Housing Tax Credit is Not a Solution

The US relies most heavily on an affordable housing mechanism that is not very good at making housing affordable to low-income renters. Currently, the primary mechanism for providing affordable rental housing is the Low-Income Housing Tax Credit (LIHTC), which goes to investors when they invest in affordable housing.

The tax credit is affected by the overall investment landscape. If investors use less of the credit, less affordable rental housing is created even when there is no reduction in the need for affordable rental housing. For example, in the wake of the Great Recession there was a decline in the amount of the credit used. LIHTC responds to the needs of investors, not the need for affordable housing.

The demand for affordable housing is permanent, but LIHTC affordable housing is temporary. The housing created with the LIHTC generally shifts to market rate housing after 30 years, and in some cases, this shift can occur in as few as 15 years. The country is at risk of losing nearly half a million housing units over the next few years because of the 30-year expiration date. About 10,000 housing units are lost annually after only 15 years because of a technical issue in the credit. Again, this design is great for investors, but it is terrible for the renters facing large rent increases as the affordability requirements expire.

LIHTC affordable housing is not very affordable. The Joint Center for Housing Studies reports that, “lower-income renters living in LIHTC units often require additional subsidies to make this housing affordable.”

Low-Income Renters Want a Public Option

In 2013, the waiting list for 8,000 public housing units in Washington DC was closed after 70,000 people added their names. When the Chicago public housing authority opened its waiting list in 2014, 280,000 families entered their names, a number equal to a quarter of the city’s population. Many cities have closed their waiting lists for public housing because they are so long. In large cities, households can be on public housing waiting lists for decades.

There is a strong demand for public housing. Households in public housing are less likely to be cost-burdened than households in LIHTC housing. Public housing is one of the most affordable rental policies in our toolkit, and low-income renters seem to know this. Instead of responding to this high demand for public housing by increasing the supply and quality of public housing, policy makers passed the Faircloth Amendment which has helped to end the construction of new public housing.

Public housing was originally quite desirable housing created primarily for white working- and middle-class households during a period of a severe housing shortage. But, as the author Richard Rothstein notes, “From the beginning, the real estate industry bitterly fought public housing of any kind.” And, he adds, “once the housing shortage eased, the real estate lobby was successful in restricting public housing to subsidized projects for the poorest families.” This was a key part in undermining the quality of public housing. Rothstein concludes:

The federal government had required public housing to be made available only to families who needed substantial subsidies, while the same government declined to provide sufficient subsidies to make public housing a decent place to live. The loss of middle-class tenants also removed a constituency that had possessed the political strength to insist on adequate funds for their projects’ upkeep and amenities. As a result, the condition and then the reputation of public housing collapsed.

But in spite of multiple policies aimed at destroying public housing, there is still a strong demand for it.

The Social Housing Model

The US needs to repeal the Faircloth Amendment, end the LIHTC, and dramatically increase the amount of public housing. The new model for public housing should be a social housing model where public and nonprofit-owned housing is not restricted to the poorest households. Some portion of this new public housing should be reserved for the poorest households, but a portion should also be market rate housing, and a portion with rates lower than market rate, but not subsidized as heavily as that for the poorest households. (See the “Self-Financing Rental Models” in the appendix to Social Housing in the United States and Public Housing for All for financing models.)

Policy makers should learn from social housing examples in Europe, Asia, and the US. Much of the early history of US public housing was similar to social housing. Social housing in the US has not completely ended. As the economist Paul Williams reports:

California’s university system, a public entity, develops, builds, owns and operates housing for students on its campuses. The Alaska Permanent Fund Corporation purchases, develops, builds and collects rents from its own housing. The Housing Opportunities Commission in Maryland’s Montgomery County recently funded a program that will result in thousands of county-owned mixed-income apartments over the next decade, using a creative financing scheme of their own.

Additionally, there is a bill in the California State Assembly to create social housing in the state. The US will need to expand the scale of these types of activities.

Finally, housing assistance, whether social housing or housing vouchers, should be expanded to meet the need. Everyone who is eligible and applies receives federal homeownership tax benefits. But most renters in need of housing assistance do not receive any government support. In many European countries, there is no limit on the number of households that can receive rental assistance. If the US adopts these policies, it will finally create enough affordable rental housing to reduce housing cost burdens for low-income renters.