June 22, 2011

In discussing the Fed’s QE2 program, the NYT tells us that things are much different today than they were a year ago.

“Last year prices were falling; this year, prices are increasing.”

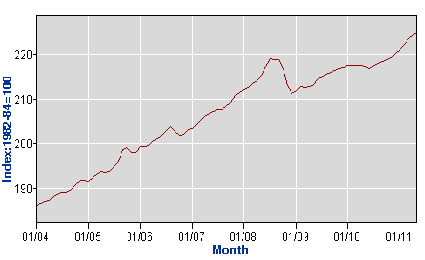

Well, sort of. Here’s the overall CPI where there is in fact a small drop between April and June, although it is completely reversed by the July increase.

Source: Bureau of Labor Statistics.

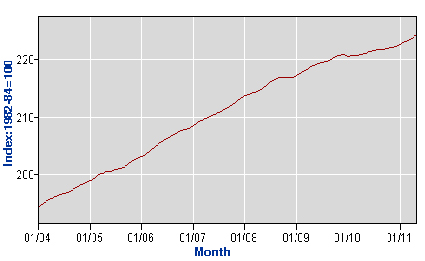

Of course, if we look at the core CPI which the Fed targets, there is no decline in prices at all in the summer of 2010. In fact, inflation looks pretty much exactly the same in the summer of 2011 as it did in the summer of 2010.

Source: Bureau of Labor Statistics.

In other words, what explains the difference in the Fed’s behavior is not any obvious difference in inflation or even the growth outlook. (Growth projections were if anything stronger in the summer of 2010 than at present.)

Rather, the most obvious explanation is a difference in politics. There is a growing push against any effort to stimulate the economy, which is noted in the article. It is this change in politics that seems to explain the end of quantitative easing, not any change in the economy.

This article includes a peculiar statement by Mark Zandi, of Moody’s Analytics, which attributes the economy’s weakness to a loss of confidence. It would have been useful to ask how he thought low confidence was hurting the economy. Consumer spending continues to be very high relative to income and investment in equipment and software is quite strong given the low capacity utilization rates, so it is not obvious what sector of the economy is being constrained by a lack of confidence.

Comments