November 19, 2020

The author thanks Sarah Rawlins and Karen Conner for helpful comments and work on this report.

The United States is considered a beacon of democracy; democracies, by design, are meant to promote the interests of the majority while protecting the rights of the minority. However, as income inequality has soared, this basic tenet has come into question, as evidenced by Americans’ weariness to tax the ultrawealthy.

In Illinois, a graduated income tax proposal that would raise the taxes of the ultrawealthy, but not on 97 percent of the population failed 55-45 percent.1

At this point, a reasonable person may wonder why this tax referendum is relevant to anyone outside of Illinois. The answer is that while the effect of the amendment is directly consequential to Illinois, the debate around this amendment captures many of the broader trends in the United States.

By looking at what happened in Illinois, we can distill broader political factors that are applicable across the country. These factors have come together in a manner that protects the enormous wealth of a small minority (top 3 percent), at the expense of everyone else. Equally importantly, this ultrawealthy minority tends to be disproportionately white, while the poorest communities who pay the greatest price tend to be disproportionately nonwhite.

In Illinois this year, one of the most anticipated outcomes of the election had nothing to do with any individual candidate. The focus was on a proposed amendment to the state’s constitution that would allow for a graduated income tax.

Currently, Illinois has a flat income tax rate of 4.95 percent, which means that regardless of income level, income is taxed at 4.95 percent by the state.2 The proposed graduated income tax would change this system so that different levels of income are taxed at different rates. The basic principle is that higher earners can afford to pay more in taxes, which are used to fund essential public services such as schools and fire departments. Currently, of the 41 states that tax income, 32 of them (and the District of Columbia) have a graduated income tax.3 Illinois Governor Pritzker pushed in favor of the amendment, citing it as an important source of revenue for the state’s strained budget which COVID-19 has only worsened.

What’s in the proposed amendment? The amendment itself simply removes the current flat tax from the state’s constitution and grants the state the power to tax higher income levels at higher rates.4 The amendment does not change the tax rates; it simply allows future legislation the ability to do so. However, the General Assembly in Illinois has already approved a new tax scheme in the case of a graduated income tax.5 Based on that proposal, the tax rates would be as seen as in Table 1.

Table 1

| Income Level (dollars) | Tax Rate (percent) |

|---|---|

| Less than 10,000 | 4.8 |

| 10,000 – 100,000 | 4.9 |

| 100,000 – 250,000 | 5.0 |

| 250,000 – 350,000 | 7.8 |

| 350,000 – 750,000 | 7.9 |

| Greater than 750,000 | 8.0 |

Source and Notes: OurQuadCities. The current tax rate is 4.95 percent for all.

Since it’s an amendment to the state constitution, its passage requirements are a little different from general ballot initiatives. To pass, either 60 percent of the people voting on the question must vote yes, or a majority from the total number of people voting in the election as a whole.6

Under this new tax system, anyone making under $250,000 (97 percent of the state’s residents)7 would not see their taxes increase. If it wouldn’t cost 97 percent of wage earners anything more and could provide much needed revenue to improve public services, one would assume the measure would pass in a landslide. Of course, if that were the case, there’d be little point in writing this piece.

Despite intuitively only appealing to a small subset of the population, the opposition was able to create a formidable challenge. The opposition largely consisted of a coalition of Illinois’ wealthiest residents and business owners (the graduated income tax would also increase the corporate tax rate from 7 percent to 7.99 percent).8 Through organizations like the ironically named Americans for Tax Reform,9 the opposition has argued that the amendment is a blank check for Springfield and will hurt small business. Of course, just like the majority of individuals, the majority of small businesses, would not actually see their tax rates increase. Kenneth Griffin, Illinois’ wealthiest resident with a net worth of $15 billion,10 has been the most notable member of the opposition. Griffin has donated over $53.75 million to the Coalition to Stop the Proposed Tax Hike Amendment.11 To be fair to the opposition, Illinois does have the worst credit rating of any state, with its rating just barely above junk status,12 which may explain part of the skepticism about giving the government more tax money to spend.

The proposed amendment failed on November 4th with 98 percent of precincts reporting. In fact, it failed by quite a remarkable margin – 55 percent-45 percent against the amendment,13 since the measure is an amendment to the state constitution requiring 60 percent to pass. Thus, the amendment fell 15 percent short of the minimum threshold needed, despite only raising taxes on the wealthiest 3 percent. Even polling conducted by the opposition did not except such a comfortable margin; preelection polls were between 49-51 percent. The hefty margin has allowed the opposition to conclude a definitive victory, despite the 300,000 – 400,000 ballots that had not been counted.14

Unfortunately, what the opposition fails to understand (or purposely distorts) is that the issue is not really over the role of government; Illinois is facing a dire fiscal situation and needs to increase revenue. With the failure of the amendment, Governor Pritzker has signaled that an across-the-board tax increase will be likely. The issue is not whether taxes will increase, but a question of whose taxes will increase. When you consider the question as a choice between an increase in the flat tax rate or switching to a graduated tax (that would only raise the rate on the wealthiest 3 percent of the population), the answer seems more straightforward.

Pritzker has suggested that if the flat tax were raised, it would be by about 1 percent, bringing the hypothetical new flat tax rate to 5.95 percent. That’s approximately 2 percent less than what the tax rate would be on top earners under the graduated income tax (between 7.75 percent and 7.99 percent). So, to summarize the two possible tax scenarios:

1. Graduated Income Tax

2. Flat Tax Increase (likely measure if the graduated income tax fails)

In nominal terms, the flat tax increase would ask an individual with an annual income of $10,000 to pay an additional $100 in taxes (over the base $495 they already pay). A wealthy Illinoisan, making $750,000 annually, would pay an additional $7,500 (over the base of $37,125). In terms of income after this tax alone,15 the former individual would have $9,405, while the latter would have $705,375. The important piece is to compare this scenario to the graduated income tax. Under a graduated income tax, the individual making $10,000 would see their taxes decrease, and the wealthy Illinoisan would pay an additional $22,800, still leaving them with a staggering $690,075.

At this point, it would be useful to practically consider the tax burden placed on these two individuals in practical terms. If an individual’s annual income is $10,000, it’s reasonable to assume that the entirety of his or her income is going towards basic necessities (food, shelter, etc.). A hundred dollars may seem like a trivial increase, but that’s $100 less in food or rent to an individual on an already tight budget. In contrast, if someone is making $750,000, he or she has plenty of disposable income and their basic necessities are comfortably met. Paying an extra $22,800, while a relatively large nominal amount, won’t cause any significant lifestyle changes. It’s likely money that would have been saved or invested. Of course, this individual isn’t going to be thrilled about paying more in taxes, but it’s just an annoyance; they’re not worried about starving or being evicted as a result. The same cannot be said of the first individual (making $10,000); giving up one additional dollar is not worth the same to both individuals. Economists recognize the increased relative importance of every dollar to the lower wage individual. We cannot simply assume that because the rate is equivalent (5.95 percent), that the sacrifice is the same for all individuals, especially given the fact that the wealthiest earners make at least 75 times more than the lowest earners. The flat tax increase is worse for lower earners and the graduated tax is worse for higher earners; but with incomes of $9,405 and $690,075, life is already drastically harder for the former, whereas as the latter could recoup the difference in income with a good investment year.

If that’s not convincing enough, keep in mind that Illinois’ collective tax system (income, sales, property, etc.) falls most heavily on low-income individuals.16 The state relies on its sales tax for much of its revenue (in Chicago, the rate is 10.25 percent).17 The problem with taxing consumption at a high rate is that it disproportionately affects lower-income people. Why? Low-income people spend most or all of their money on necessities, so all of their income is being taxed by a sales tax. Wealthier people save a significant portion of their income, and that part of their income is free from a sales tax. Considering all of this, a graduated income tax would be a first step in moving the state away from its current regressive tax system.

Plenty of publications have enumerated the pros and cons of a graduated income tax and who the likely winners and losers are. However, little to no attention has been paid to the demographics of said winners and losers. Chicago is Illinois’ largest city and where the majority of the state’s ultrawealthy are concentrated. It’s also an incredibly segregated city. Overall, Chicago is fairly evenly mixed – 33 percent white, 30 percent Black, 29 percent Hispanic, 6 percent Asian, and 2 percent other.18 However, of its 77 community areas, virtually none of them even come close to this type of demographic split. Of the 77 communities, 82 percent have a single race accounting for more than 50 percent of the population. Even more strikingly, 23 percent of the communities have one race accounting for over 90 percent of the population. In other words, almost one-in-four communities in Chicago is almost entirely made up of a single race.

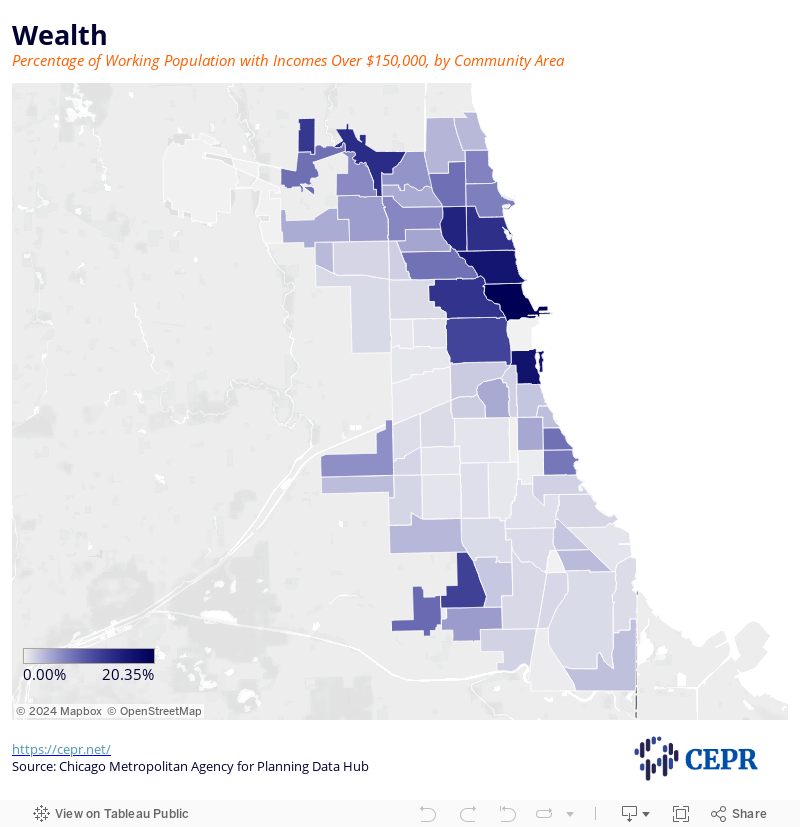

Figure 1

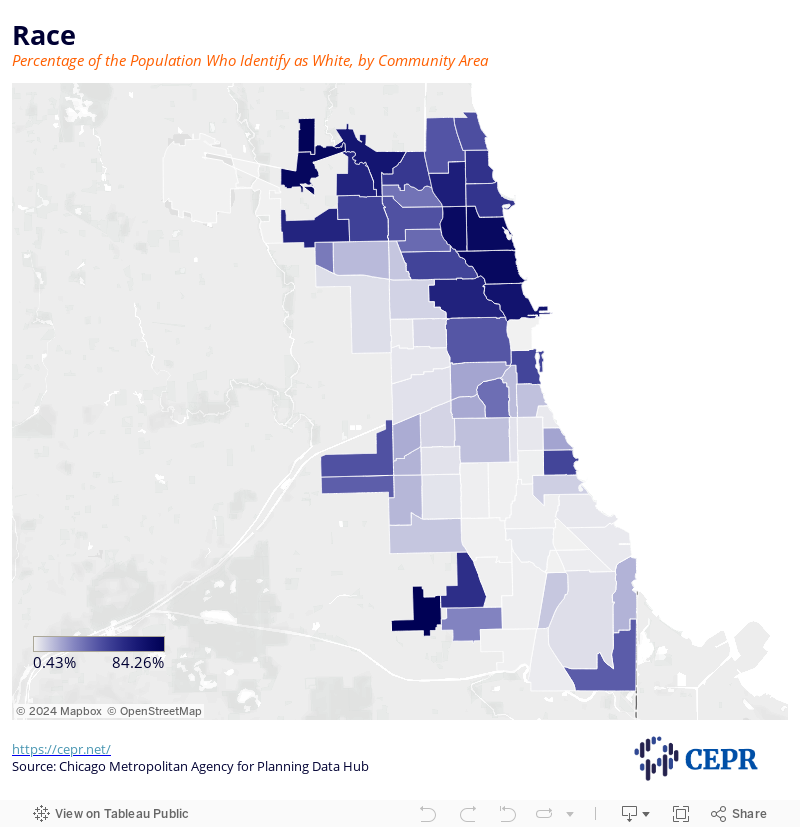

Figure 2

Figure 1 is a gradient map depicting the number of individuals with incomes over $150,000. These are the neighborhoods that are most likely to be negatively affected by a graduated income tax. Figure 2 is a gradient map that shows the percentage of a community area that is white. Remarkably, the two figures are almost identical. The neighborhoods that have the highest numbers of wealthy individuals are neighborhoods that are disproportionately white. The obvious flip side is that the poorest neighborhoods are comprised of non-whites. To further illustrate the point, consider Table 2 which provides the specifics of the six communities at either extreme.

| Median Income | White | Hispanic | Black | Asian | Other | |

| (dollars) | (percent) | |||||

| Poorest Neighborhoods | ||||||

| Riverdale | 13,518 | 1.8 | 2.6 | 95.3 | 0.3 | 0.0 |

| Englewood | 21,275 | 0.7 | 4.3 | 94.1 | 0.3 | 0.5 |

| East Garfield Park | 22,818 | 6.0 | 3.6 | 87.7 | 0.6 | 2.2 |

| Fuller Park | 22,920 | 3.5 | 6.6 | 89.1 | 0.5 | 0.2 |

| West Garfield Park | 24,591 | 2.1 | 2.6 | 93.7 | 0.3 | 1.2 |

| Burnside | 25,461 | 0.4 | 1.6 | 97.0 | 0.0 | 1.0 |

| Wealthiest Neighborhoods | ||||||

| North Center | 115,756 | 77.5 | 11.4 | 1.7 | 5.0 | 4.4 |

| Forest Glen | 111,771 | 69.5 | 15.0 | 1.1 | 12.2 | 2.1 |

| Lincoln Park | 108,875 | 79.1 | 5.9 | 4.6 | 7.4 | 3.0 |

| The Loop | 107,246 | 62.3 | 8.3 | 8.9 | 17.4 | 3.1 |

| Edison Park | 101,213 | 83.1 | 10.0 | 1.9 | 2.5 | 2.5 |

| Near South Side | 100,720 | 47.5 | 4.1 | 24.6 | 20.6 | 3.3 |

| Chicago Average | 53,335 | 32.8 | 29.0 | 29.7 | 6.4 | 2.1 |

Source and Notes: Chicago Metropolitan Agency for Planning Data Hub

Income is on average four times greater in the wealthier areas, with even greater inequality at the extremes. Equally strikingly is the difference in demographics between the two tables; an unfortunate but poignant reminder of Chicago’s segregated dynamics.

Table 2 shows that the graduated income tax would benefit Black households and, of the small number of households that would see their taxes increase, most of them would be white. The tax itself is not a racial issue, but its consequences most certainly are.

In a democracy, we naively believe that the laws are passed to benefit the interests of the majority of people. The reality is far more complicated, as evidenced by the fact that a graduated income tax which would benefit 97 percent of people in Illinois failed by a large margin. Here are three important themes, highlighted by the Illinois tax referendum, that are broadly applicable across the US.

While nothing covered in this piece so far required especially investigative journalism, it’s likely that a large portion of the people who voted in the election weren’t entirely sure what a graduated income tax would entail. Many middle-class families ($75,000–$150,000) may have been worried that their income was high enough to qualify them for a tax increase; the reality is that it was not.

Why was the opposition’s framing successful? In part, because the opposition did a fantastic job of framing the amendment as the “tax hike” amendment. Technically, it was a tax hike, but it was a tax hike for the wealthiest 3 percent of the population, a fact they cleverly omitted. Part of the issue is there aren’t very many trusted, impartial sources of information. As political polarization continues, people seek out news from places that confirm their political intuitions, which often omits part of the story. A small-government advocate may have been against increasing taxes on principle but didn’t realize the question was effectively between an across-the-board tax increase or a graduated income tax. Distorted information is part of the reason that an increasing portion of the electorate seem to be voting against their best interest. When it’s not clear what is at stake, you might not realize what you’re really voting for.

The notion of one person, one vote is central to democracies. The US was founded on the idea of promoting the interests of the majority, while protecting the rights of the minority. Unfortunately, in practice, some voices/interests are louder than others. The push for the amendment was led by Governor Pritzker, an heir to the Hyatt fortune, who spent $56.5 million19 of his personal wealth to push for the amendment. The opposition was led by Kenneth Griffin, the founder of Citadel Securities, who spent $53.75 million to campaign against the amendment. Regardless of whose side you fall on, there is no doubt than both Pritzker and Griffin had the resources to sway many individuals, magnifying the force of their own beliefs well beyond the one person, one vote baseline.

Lobbying of course, isn’t a uniquely Illinoisan innovation. In 2018, $3.4 billion dollars was spent on lobbying in the US.20 The issue is so prevalent that in 1995, the Lobbying Disclosure Act was passed, which requires public disclosure for legislative and executive lobbying at the federal level.21 Notably, the act does not apply to state or local lobbying. I assume that in part, the idea was that if all lobbying had to be reported, there would be less of it happening, because people would be ashamed. Maybe $3.4 billion is less than what lobbying would be without the law, but it didn’t exactly eliminate the issue entirely. And if lobbying was not deeply entrenched enough into the system, look at the electoral college.

The electoral college ultimately hands more political power (a larger voice) to lower populated, rural states than urban cities.22 Coincidently, these rural states tend to be majority white, which means that white voters have more of a say in our policies than other groups overall. This helps explain why democrats have repeatedly won the popular vote but lost the presidency. Of the last nine elections, democrats won the popular vote seven times, but will only hold the presidency five times.

While distorted information helps people unknowingly vote against their best interest, it’s not always unknowingly. Although seemingly odd, it’s a well-documented phenomenon. Look at the estate tax, which is a tax on the transfer of property for a deceased person.23 The federal estate tax is on individuals with assets of greater than $5.3 million or couples with assets greater than $10.6 million.24 Ninety-nine percent of Americans do not qualify for an estate tax. In fact, in 2019, of the 2.7 million people that died, only .07 percent paid an estate tax.25 You’d imagine that approximately 99 percent would be in favor of such a tax. Even economists, a notoriously divided discipline, agree that there is a strong case for estate taxes, and they can be helpful in reducing inequality.26 But estate taxes are largely hated; in some cases, even more so by the poor than the rich. A 2017 Quinnipiac survey found that 48 percent of respondents favored repealing the estate tax, while only 43 percent opposed the idea (i.e., keeping the current estate tax).27 This is often because people tend to believe and or hope that they will become wealthy in the future. Therefore, people oppose estate taxes, in part, because they hope to become wealthy enough to qualify for the estate tax in the future. Of course, most people will never qualify for such a tax, but in the process, they prevent the presently ultrawealthy from being taxed, which allows generational wealth to be passed down. This is in some ways the trickiest obstacle to overcome, but presumably re-emphasizing the statistical nature of the situation would help increase its appeal.

The main issue is how these three factors have come together to create a perfect storm, echoed across the country, that helps enact and keep in place policies that benefit a disproportionately white, wealthy elite, at the expense of everyone else. While some may take comfort voting in favor of a small-government, conservative ideals in principle, the reality is that we’ve protected the ultrawealthy at the majority’s expense. It’s time for some pragmatism.

Systematic inequality refers to biases that are inherent under the model we operate in. True change requires us to re-evaluate the systems that we have in place and consider, on a fundamental level, whether or not they perpetuate inequality. The graduated tax amendment is an example of doing just this – re-evaluating our current tax system and deciding whether or not it’s fair. The existence of such a referendum is a positive step, but for the most vulnerable and marginalized in our communities, it’s not enough on its own.

We have to actively create the change, i.e., vote in favor of such reforms. Economists will genuinely debate the pros and cons of a flat tax versus a graduated one, but I’m confident in assuming that the vast majority of people in Illinois are not economists. When a measure was proposed that would not harm 97 percent of the population, one really has to wonder why it’s so hard to pass. How representative can our democracy be if such an amendment fails. People don’t generally vote with advanced knowledge of abstract economic principles; they vote based on what they think will benefit them and their surrounding communities. And if it wasn’t inherently obvious to most Illinoisans that this would be to their benefit, then that’s a huge red flag for how we disperse and educate our populous on political matters.

Of course, many will argue that fixing such matters (distortion of information, lobbying, etc.) will take time. But I think that we can and should expect more for two reasons. First, such matters are pinnacle to our fundamental notion of democracy and who we are as a nation, so what could possibly be more important to fix. And second, we cannot forget the people who have and will continue to pay the highest price – low-income people, who are disproportionately of color. The social unrest in the US didn’t happen overnight; it has been brewing for decades as communities of colors have noticed that, for a variety of reasons, they always seem to get the short end of the stick. Perhaps, we should stop exclusively looking at policy proposals in terms of end-state outcomes and start considering historical inequities. Chicago, a microcosm of the United States, was and continues to be segregated; the maps in Figures 2 and 3 have looked like that for quite some time. So maybe when we consider who should pay more in taxes, we should consider who has historically paid more than they should.

As a final point, we should keep in mind the magnitude of inequality. Economic models tell us about the general trade-offs between taxing everyone and taxing the wealthy. But in the modern-day US, the wealthy have magnitudes of order more wealth than everyone else (think Jeff Bezos who is worth $180 billion). And in cases where the inequality is so great, we have to wonder how those trade-offs are affected and if the ultrawealthy can and should bear a greater responsibility. When the income of households in the highest tax bracket is 75 times greater than the lowest, we really have to question the fairness of everyone paying the same rate.