July 06, 2014

Floyd Norris had an interesting piece on the impact of investor purchased homes on prices at the lower end of the housing market. His takeaway is that investor purchased homes have made housing less affordable for many low and moderate income households.

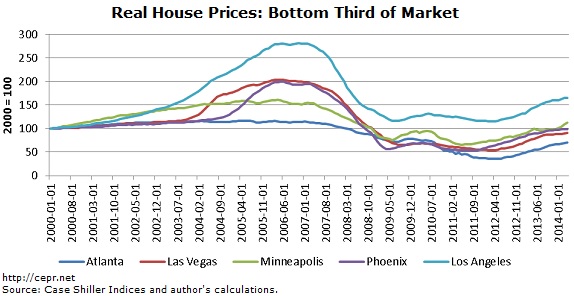

While this is partly true, by focusing only on the last couple of years the piece misses much of the picture. While investor purchases have pushed prices to unusual levels in many markets, in some cases they essentially put a floor on the market, helping to stabilize prices at levels that are consistent with longer term trends. The chart below shows house prices in the Case-Shiller indices for the bottom third of the market for five cities. (This is the same series used for the charts in the article.)

There are several features of this chart worth noting. First, it is possible to see a rise in house prices (most pronounced in Minneapolis) in the middle of 2009. This was the result of the first-time homebuyers tax credit. This policy currently ranks #1 as most boneheaded policy of the century. It encouraged millions of people to buy into a market that was still inflated by the housing bubble.

As soon as the credit ended, prices began to plummet again, surprise, surprise. Many of these first-time homebuyers suddenly found themselves underwater. Of course the flip side is that many homeowners were able to dump their homes before they went underwater. And, many holders of mortgages were able to get them paid off either through a sale or refinancing. The new mortgages almost always sat with the government, either at Fannie Mae or Freddie Mac or were guaranteed by the Federal Housing Authority. In fairness, prices have mostly recovered, but those who were forced to sell in 2011 or 2012 would have taken large losses.

The other noteworthy point not fully picked up in Norris’ discussion is that the house price rise had moderated in most markets. This is an unheralded result of Bernanke’s famous “taper talk” in June of 2013. This press conference, at which Bernanke first suggested that the Fed would soon start cutting back its quantitative easing program, sent interest rates soaring. As a huge and possibly unintended plus, it took the air out of the bubble in many of these markets.

In many cities, house prices in the bottom tier had been rising at extraordinary rates. For example, in Phoenix house prices in the bottom tier had risen 44.6 percent between May of 2012 and October of 2013, a 29.8 percent annual rate. (October is used because there is a lag between when the market weakens and its appearance in the index.) The rise in prices over the same period for the bottom tier of the market in Las Vegas and Atlanta was 57.9 percent and 80.3 percent, respectively. In the six months since October for which we have data the annual rate of price increase for the bottom tier in Phoenix has been 4.5 percent, in Las Vegas it was 7.6 percent, and in Atlanta it was 17.7 percent.

In these markets prices had been badly beaten up, so a bounce back was good news. However, when prices are rising at a 50 percent annual rate, as was the case in the bottom tier in Atlanta, they will soon be in bubble territory regardless of how low they started. Bernanke’s taper talk broke this bubble momentum. That may not have been his intention, but he deserves some serious credit on this one.

This brings us to the final point, we may indeed have some new bubbles to worry about. Inflation-adjusted house prices for homes in the bottom tier in Los Angeles are 64.7 percent above their level at the turn of the century. The price increase for the bottom tier in San Francisco would be even larger. While these are clearly desirable cities in which to live, there has been no comparable increase in rents. In the case of Los Angeles, the rental index has risen by just 13.8 percent in real terms over the same period.

This discrepancy should give homebuyers in Los Angeles and other cities with sharply rising house prices something to worry about. While rents and house prices may not rise at exactly the same rate, this is an extraordinary discrepancy. The past history indicates that it is more likely that house prices will adjust to bring the two into balance. A plunge in house prices in Los Angeles, San Francisco and other cities with inflated house prices will not crash the economy, as did the bursting of a nationwide housing bubble, but it will not be pretty for those directly affected.

Comments