Article

As the Affordable Care Act Enters Adolescence, US Health Care Still Has Growing to Do

Article

Wednesday, March 23 marks the 12th anniversary of the passage of the Patient Protection and Affordable Care Act (ACA), a landmark piece of legislation that significantly expanded health insurance coverage in the United States. Together with the Health Care and Education Reconciliation Act of 2010, the ACA is widely considered the most consequential US health care reform since the establishment of Medicare and Medicaid.

Bolstered by pandemic relief subsidies, the ACA was instrumental in blunting the impact of the COVID-19 pandemic on Americans’ health insurance coverage. Ultimately, however, the ACA was only a promising first step, and the US health care system remains deeply flawed. Ensuring comprehensive coverage for every American will require more fundamental overhauls.

The ACA made important changes to the way health insurance operates in the US. The law established marketplace exchanges where individuals could purchase qualified health care plans, with subsidized rates available for low-income people. Exchanges could be operated through the federally run HealthCare.gov or independently by states. Insurers were barred from rejecting applicants or charging them extra based on preexisting health conditions or demographic characteristics besides age, and insurance plans were required to meet cost-sharing and coverage standards.

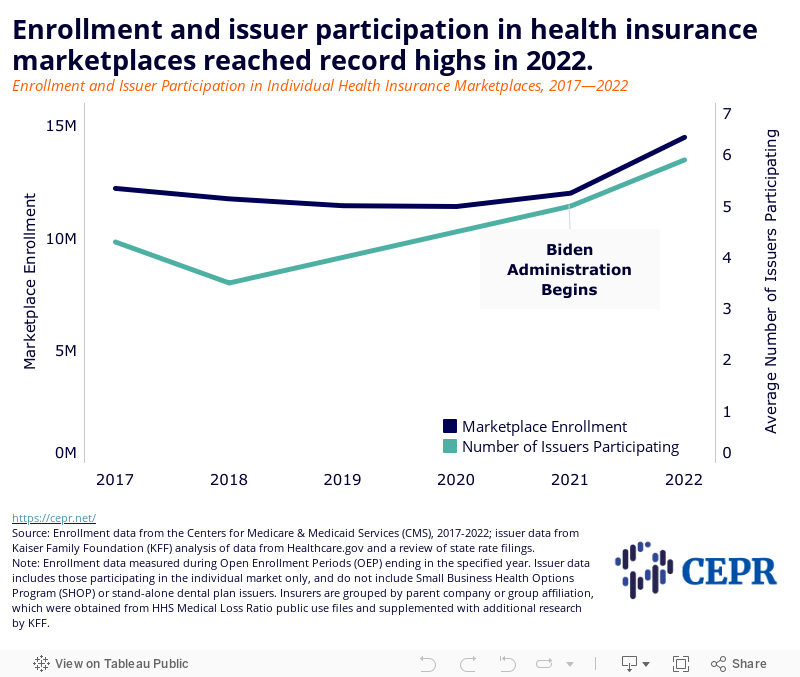

Over the last year, a record number of Americans have obtained health coverage through ACA insurance marketplaces (Figure 1). The 2022 marketplace Open Enrollment Period (OEP) saw the highest number of enrollees since the passage of the ACA, with 14.5 million either starting or continuing marketplace coverage between November 2021 and January 2022. Prior to this, over 2.5 million signed up for new marketplace coverage during the extended Special Enrollment Period (SEP) between February and August 2021. The average number of insurance issuers participating in individual health insurance marketplaces has also ticked up. It is now at the highest number recorded since the ACA exchanges were established.

Figure 1

The ACA also sought to increase coverage by expanding eligibility for Medicaid. States were directed to revise their eligibility criteria to include all adults with incomes at or below 138 percent of the Federal poverty line—$38,295 for a family of four in 2022. Federal funding fully supported newly eligible enrollees through 2016, after which the federal share was gradually reduced until reaching 90 percent for 2020 onward.

Despite a Supreme Court ruling allowing states to opt out, to date 38 states and DC have elected to adopt the ACA’s expanded Medicaid eligibility criteria. Evidence suggests immense benefits to opting in; these include improved health outcomes and reduced mortality, increased financial well-being for lower-income households, narrowed care-related racial and ethnic disparities, employment boosts among working-age adults with disabilities, crime reduction, and net savings at the state level, to name just a few. By contrast, non-expansion states appear to suffer larger gaps in coverage and access to care (especially among young men), poorer health outcomes, higher rates of poverty, and lower crisis resiliency.

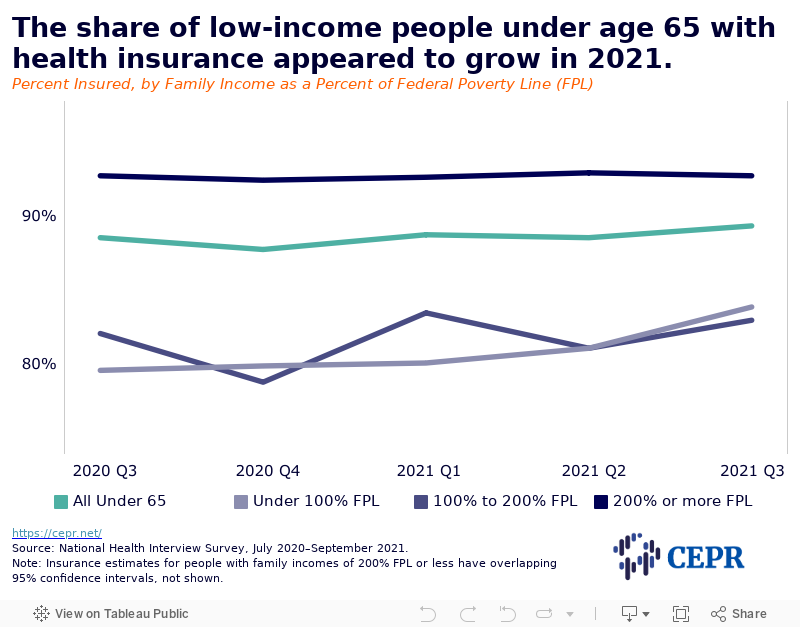

During the COVID-19 pandemic, increases in public coverage, particularly Medicaid coverage, have been instrumental in offsetting declines in private coverage. The percentage of non-elderly adults with health insurance was roughly the same in March 2021 as in March 2019. Coverage data through the end of 2021 is not available yet, but point estimates of insurance among non-elderly people trended upward through the third quarter of 2021, with the most notable increases occurring among low-income people (Figure 2).

Figure 2

Small sample sizes for these preliminary estimates mean they have wide and overlapping confidence intervals. When considered alongside administrative data showing a sharp increase in the number of Americans obtaining coverage through ACA marketplace exchanges and boosted Medicaid enrollment, however, there is good reason to believe that the share of Americans with health insurance may now exceed pre-pandemic levels.

Recent increases in insurance coverage are largely due to the American Rescue Plan Act (ARPA), which expanded eligibility for marketplace insurance subsidies and increased financial assistance for people who were already eligible for subsidies. The legislation also provided additional fiscal incentives to encourage hold-out states to adopt the expanded ACA Medicaid criteria, and ensured that Americans who were receiving unemployment benefits had access to zero-cost plans. Out-of-pocket costs have also come down; both average monthly benchmark premiums and median individual deductibles have decreased substantially. However, it remains to be seen whether these gains will be short-lived. Key provisions in the ARPA that enabled coverage expansion and increased affordability are set to expire in 2022.

Health insurance coverage and care access have both improved substantially since the passage of the ACA, and the ARPA has further shored up the system amid the COVID-19 public health crisis. The administration has fulfilled many of President Biden’s ACA-related campaign promises, though it has yet to make good on his pledge to establish a public health insurance option. Doing so would restore a key provision that corporate interests succeeded in eliminating from the ACA prior to its signing.

All of these proposals keep in place the country’s current system of largely for-profit health insurance, one where most of the working age population receives coverage through their employers. There are many problems with this structure. First, it continues to leave millions uninsured or otherwise hesitant to access care due to cost concerns. Requiring employers to act as health insurance intermediaries is burdensome for both employers and workers, promoting job lock and stifling entrepreneurship. This dynamic is especially fraught during a public health crisis, where people find their access to health care curtailed as a result of losing their jobs. The for-profit system is also expensive and administratively complicated, and the needs of patients are often secondary to the financial prerogatives of insurers and providers.

Many of these problems are solvable, policy-wise. The most straightforward way to ensure universal coverage would be to establish a single-payer system, such as that proposed in the Medicare for All Act of 2021 (2021 MFAA). In addition to making all Americans eligible for Medicare, the 2021 MFAA would modernize the program so that it offered benefits comparable to those currently available only through private Medicare Advantage plans. The 2021 MFAA would also eliminate cost-sharing in the form of deductibles, co-pays, and other charges. Finally, the 2021 MFAA would authorize the government to negotiate drug prices and, if negotiations broke down, allow adjustments to the terms of patents and other government-granted licenses for market exclusivity. These measures would help control prescription drug costs, which are more than 2.5 times higher in the US than in other countries.

Such legislation would reorient incentives to prioritize patient and public health rather than corporate profits. It could also have positive spillover effects, including new business and job creation and increases in wages and job quality. Single-payer systems have been thoroughly vetted abroad, and nations with universal coverage enjoy lower costs, more equitable access, and better overall health outcomes than the US.

Finally, it is worth noting that, despite our use of the word “Americans” throughout this piece, the ACA significantly neglected those who reside in US island territories. Residents of these territories are not eligible for the subsidies meant to make health insurance affordable. And unlike in the 50 states and DC, the federal government’s Medicaid contribution in the island territories is capped according to a set allotment each year. This disparate treatment jeopardizes coverage for the most vulnerable and ultimately costs the federal and state governments billions more than equitable treatment would. A truly universal system of coverage cannot neglect those who live in the parts of the US that don’t appear on the logo map, so it is important that the 2021 MFAA explicitly takes a more inclusive approach.

The passage of the ACA was an extraordinary achievement, one that significantly improved health care access in the United States. It deserves credit for the monumental progress it enabled and the numerous lives it has saved and improved. Similarly, the Biden administration deserves to be commended for the improvements it made and the catastrophes it averted by shoring up the ACA during the pandemic. Yet there is still much more work to be done. To meet the moment and the needs of the American people, the Biden administration must champion more ambitious policies that would truly reform health care in this country.

Portions of this piece are adapted from content that previously appeared in another CEPR publication.