November 04, 2022

The New York Times ran a bizarre piece today telling readers that we face a serious threat of wage price spiral:

“Fresh data out on Friday showed that average hourly earnings climbed 4.7 percent over the past year. That is far faster than the 3 percent pace that prevailed before the pandemic, and is so quick that it could make it difficult for inflation to fully fade. Plus, policymakers remain anxious that today’s pressures could yet turn into a spiral in which wages and prices chase each other higher.”

The data really don’t support this story. First, although the year over year rate of wage growth did slow to 3.0 percent just before the pandemic, it was actually considerably higher for much of 2019. For example, in the year from February 2018 to February 2019 the average hourly wage rose by 3.6 percent (from $26.75 to $27.70).

This matters because we know that inflation remained comfortably below the Fed’s 2.0 percent inflation target in 2019, so it is reasonable to use wage growth in that year as a point of reference. And, the fact is that wage growth averaged roughly 3.4 percent over the course of 2019, not 3.0 percent.

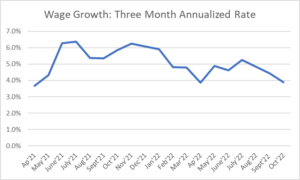

The other part of the story missing in this piece is that wage growth has actually slowed sharply over the course of this year, not accelerated as is implied. This is the picture if we take the annual rate of growth in the average hourly earnings series, over three-month periods, dating back to the spring of 2021. (I prefer to compare three-month averages, using the most recent three months with the prior three months, but it seems no one else does this.)

Source: Bureau of Labor Statistics and author’s calculations.

As can be seen, the rate of wage growth by this measure peaked at 6.4 percent in July of 2021. It fluctuated some over the next several months and was still 6.3 percent in November of 2021. Since then it has slowed sharply. In the most recent three-month period, wages were rising at a 3.9 percent annual rate. This is still higher than the 3.6 peak year over year rate of wage growth in 2019, but not by much. (There were three-month periods where the rate was 4.0 percent in 2019.)

In short, the reality is the opposite of what this piece implies, wage-inflation has not been persistently high, but rather has slowed sharply. Part of the confusion stems from using year over year rates of wage growth rather than focusing on a more recent period. The Fed’s rate hikes, which began in March, could not slow the inflation that occurred last fall and winter, but this is what we are including, if we look at the year over year rate. While short-term data are erratic, and subject to revision, if we want a sense of where inflation will be going forward, we need to focus on recent data, not what happened nine or ten months ago.

There is an issue of the changing composition of the workforce, which does affect the rate of wage growth in this series, but this just makes slowdown from last fall more rapid. The economy was adding close to 600,000 jobs a month last fall. That is more than 1.0 percent of the workforce over a three month period. If these jobs paid 15 percent less than the average job, which is plausible since these were largely low-paid workers in sectors like hotels and restaurants, then the change in composition would reduce the average wage by 0.15 percentage point. Annualizing this rate, the change in composition would slow the rate of wage growth by 0.6 percentage points.

While this calculation is very crude, it shows that the change in composition could have substantially slowed the measured rate of wage growth by this measure last fall. This is no longer the case in recent months, as both the rate of job growth has slowed sharply and there is no longer a major skewing in job gains towards lower paid workers. (We added just 6,000 restaurant workers in October.) This means that wage growth has slowed even more sharply than is indicated by these data.

We can see this pattern of slower wage growth in other series as well, although the picture is less clear. The rate of growth of compensation in the Employment Cost Index (ECI) peaked at a 5.6 percent annual rate in the first quarter of 2022. It was down to 4.8 percent for the third quarter. Inflation in the wage component of the ECI peaked at 5.6 percent in the second quarter, it was down to 5.2 percent last quarter. (Wage growth in the ECI was 3.6 percent in the first and third quarter of 2019.)

The rate of growth of unit labor costs in the productivity data has also slowed sharply. This peaked at 8.2 percent in the fourth quarter of 2021. It was 3.8 percent in the third quarter of this year.

In short, by a variety of measures, wage growth has slowed considerably since the Fed began raising interest rates. And, by the most commonly used measure, it is now only modestly higher than a rate that would be consistent with the Fed’s inflation target.

The Fed’s focus on wage growth is reasonable, since over a long period, we can’t expect to maintain a moderate rate of inflation if wages are growing at the rates we saw last fall. However, given the large shift to profits in the pandemic, it would be reasonable to expect some larger than usual gap between the rate of wage growth and inflation, as the profit share falls back to something closer to the pre-pandemic level.

We also know that import prices, which had been a major factor contributing to inflation last year and earlier this year, are now falling rapidly. The price of non-fuel imports rose 7.2 percent in the year from April of 2021 to April of 2022. Since April, non-fuel import prices have fallen by 2.0 percent, a 4.7 percent annual rate of decline. Add to this a drop in shipping costs (which are not included in import prices) of more than 70 percent from their peak, and we should be seeing a major source disinflationary pressure.

Also, private indexes of marketed rents are now showing declines in many cities. And used car prices have begun to fall rapidly.

In short, the Fed actually has much to show for its efforts to combat inflation thus far. The full impact of its rate hikes will not be felt until late in 2023, but by some measures it has already accomplished most of what it needs to reach its inflation target. Most importantly, there is no evidence to date that inflation expectations have become unhinged and that we risk a wage-price spiral. There seems little danger at the moment if the Fed decides to get more data before any more large rate hikes.

Comments