August 02, 2015

Last week the Washington Post again editorialized in favor of reforming the Social Security disability program by either reducing benefits and/or raising disability requirements. The editorial noted the reallocation of funds from the Old Age and Survivors Insurance program to the Disability program twenty years ago and told readers;

“The last tax reallocation, 20 years ago, ‘was intended to create the time and opportunity for such reforms,’ as the Social Security trustees’ report puts it; it would seem that the time, and the opportunity, are finally here.”

In fact, it is not clear that there is any fundamental problem with the disability program that requires reform. If we go back to 2008, before the collapse of the housing bubble brought the economy to its knees, the disability program was in far better shape. It was projected to be able to pay scheduled benefits through the year 2025. Its projected shortfall over the program’s 75-year planning horizon was just 0.24 percent of covered payroll or just over 12 percent of the program’s projected revenue.

But even this projected shortfall was largely due to something that had been unexpected back in 1983 when the Greenspan commission made their recommendations to Congress for reforming Social Security. The commission had expected that 90 percent of wage income would be below the tax cap set at the time and therefore subject to Social Security taxes. This turned out to be mistaken as there was a sharp upward redistribution of wage income in the 1980s which continued into the next two decades. As a result, the program took in considerably less revenue than had been projected.

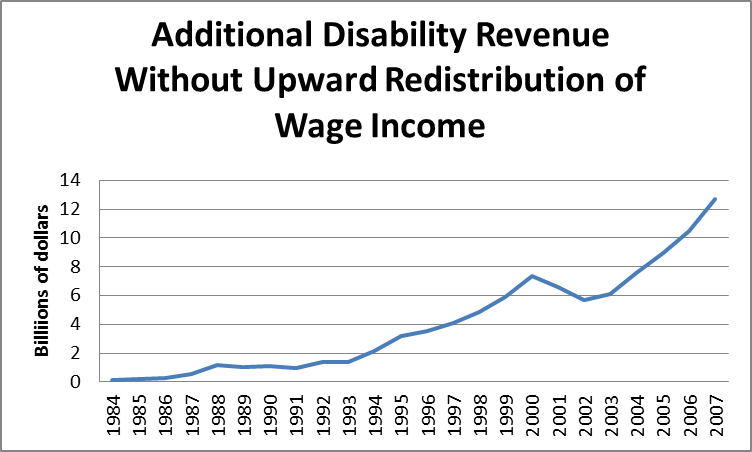

The figure below shows the difference below shows the difference year by year between the revenue the program would have received if 90 percent of wages had been subject to the tax and the revenue actually collected by the Disability Insurance (DI) trust fund. (The calculations also add in 6 percent interest on past revenue, which was roughly the interest rate on government bonds at the time.)

Source: Social Security Administration and author’s calculations.

In total the DI trust fund would have accumulated an additional $97.3 billion by 2007 if we had not seen a sharp upward redistribution of wage income since 1983. Furthermore, if there had not been this upward redistribution of wage income, the DI trust fund would see considerably more tax revenue going forward. The projections at the time assumed that the tax would cover 82.9 percent of wage income going forward, which means that future revenue would be 8.6 percent higher if the tax covered 90 percent of wage income.

Taken together, the higher tax revenue up to 2008 and the higher projected future revenue would add $524 billion to the program’s finances over its 75 year planning period. This would cover more than three quarters of its projected shortfall, leaving a gap of less than 0.06 percent of taxable payroll. That’s not 100 percent in balance, but not the sort of thing that even Washington Post editorial writers could get too worried over.

The implication of this story is that if the economy didn’t crash in 2008 due to the collapse of the housing bubble and we didn’t see a sharp upward redistribution of wage income in the last three decades then the finances of the DI program would look pretty good. In other words, the problem with DI is the economy, not the structure of the program.

If folks want to argue that we can’t count on having competent people to run the economy, then they can rightly complain that DI is not idiot proof. But as a practical matter it is not possible to design a major social insurance program that can remain financially solid in the face of severe economic mismanagement. The main problem with DI is clearly the state of the economy, not the structure of the program.

Note:

I did not count any additional payouts in my calculations. I assume these to be small both to Social Security’s progressive payback structure and also under the assumption that high end earners are less likely than most workers to end up on disability. As a countervailing factor, I did not include any interest on the additional tax collections for years after 2007.

Comments