Report

The United States, The IMF, and Special Drawing Rights

Report

In 2021, after pressure from the US Congress and civil society, the US Department of Treasury proposed to the International Monetary Fund (IMF) that the organization issue to its member countries the largest allocation of Special Drawing Rights (SDRs) in its history. The US government holds a formal veto over this decision at the Fund, and can generally, if it chooses, determine whether an allocation will go forward. The US had previously opposed the allocation for more than a year — including in 2020, when the global economy suffered its worst contraction in gross domestic product (GDP) per capita in at least 75 years. Of the 2021 issuance, which was the equivalent of $650 billion, $209 billion went to emerging markets and developing economies (EMDEs), not including China, and provided crucial support when much of the developing world was still recovering from the impacts of the pandemic and facing shortages of vaccines. These SDRs provided balance of payments support, expanded space for countercyclical macroeconomic policy, and supported vital health and social spending — including vaccine purchases — that saved many lives. Using estimates of the relationship between recession and mortality in developing countries, this paper estimates that about 1.94 million people in EMDE countries died as a result of the severe recession in 2020 — not including deaths from the COVID virus. This analysis implies that at least 283,000 lives could have been saved if the SDR allocation had been issued in March 2020, when IMF Managing Director Kristalina Georgieva had called for it. Georgieva had called for a much larger issuance, based on the IMF’s estimate of developing countries’ financing needs at $2.5 trillion, and the US House of Representatives passed legislation that would have required the US to support an allocation worth $2.8 trillion. This could have saved several times more lives than those saved by the smaller issuance. This paper examines some of the benefits from an SDR issuance and also looks at a less-explored positive spillover: the effects that an SDR issuance can have on the US economy. The US exports about $1.1 trillion annually to EMDEs, supporting millions of export-related jobs within the United States. Slower rates of growth in the developing world have been associated with the loss of hundreds of thousands of export-related jobs in the US. The data and analysis indicate that many of these US jobs can be saved when EMDEs are able to avoid balance of payments or other economic crises and stabilize their economies. SDRs can contribute to this stabilization. Given the United States’ control over decision-making at the IMF and the process — including the legal and institutional framework — by which the US government’s and IMF’s approval is determined, the potential impact of SDRs on US employment could be important to the prospects of another issuance.

In August 2021 the International Monetary Fund (IMF) distributed to its member countries the largest allocation of Special Drawing Rights (SDRs) in its history. This issuance, worth $650 billion in USD, of which $209 billion went to emerging market and developing economies (EMDEs) other than China,1 provided crucial support when many countries were still struggling with the COVID pandemic and inadequate access to vaccines.

The EMDEs’ share of this allocation was still less than a tenth of the sum that IMF Managing Director Kristalina Georgieva (and IMF research) had said in March 2020 represented the financing needs of EMDEs. At that time, the IMF had estimated this sum to be at $2.5 trillion. The pandemic recession of 2020 was just beginning, and it was already expected to be severe. As it turned out, it brought a record-breaking decline in global real per capita gross domestic product (GDP); it was the largest such contraction for at least 75 years.2

Nonetheless, the US Department of Treasury shot down the consideration of any SDR allocation within weeks. That was the end of the discussion; the US has a formal veto power over this decision and also has an informal alliance with other high-income countries that allows the US to prevail in almost all votes at the Board of Governors and Executive Board when it chooses to do so.

From the research here, the most profound implication for human survival and well-being is this: if the $650 billion issuance that was distributed in August 2021 had been made in March 2020, when the managing director of the IMF, Kristalina Georgieva, and almost all member governments wanted it to be done, it is likely that hundreds of thousands of lives could have been saved.

This is based on the statistical analysis by the Bank for International Settlements of the relationship between recessions and mortality in developing countries.3 On the basis of their findings, we estimate that mortality among the 3.9 billion people living in EMDE countries that fell into recession in 2020 would have been expected to increase by 1.94 million people as a result of the recession.4 It is likely that at least 283,000 lives, as a lower bound, could have been saved with a $650 billion issuance in 2020.

An allocation of the size that the US House of Representatives would soon approve ($2.8 trillion worth), or that Georgieva and the IMF said was needed, would be expected to save some multiple of these 283,000 lives.

This help from SDRs is even more desperately needed today in EMDE countries than it has been for many years because of unprecedented foreign aid cuts and most importantly because of the billions of dollars cut by the United States this year. This was funding for life-saving medicines and other critical health needs. Recent research in The Lancet estimates that 14 million lives could be lost by 2030 because of this loss of support for health-care programs, especially the ones targeting HIV/AIDS, malaria, and neglected tropical diseases like dengue and chikungunya.5 The need to make up for this loss of billions of dollars for life-saving health care and medicines is one of the most important health crises in the world in terms of the estimated human cost.

After the US Treasury blocked Georgieva’s proposal for a large allocation of SDRs, it came back on the agenda when the US House of Representatives, based on Georgieva’s speeches, passed legislation that required the administration to support an allocation of $2.8 trillion worth of SDRs at the IMF.

The evidence indicates that Congress played a decisive role, not only in reviving the demand for a new allocation of SDRs but also in pressuring the US Treasury to agree to a new allocation of SDRs. In the year that followed Georgieva’s appeal in March 2020, there was continued intensive lobbying of Congress, including of the Senate. A coalition of more than 100 organizations, which included organized labor and major religious institutions representing tens of millions of constituents, was involved.6 In February 2021, the Treasury announced its support for a new allocation of SDRs, thus assuring that it would be approved at the IMF.

The $209 billion from this allocation that went to EMDEs in 2021 was more than twice as much as they received in climate finance that year — $89 billion, most of which, unlike SDRs, was in the form of debt.7 The SDRs, which are reserve assets that can be converted into hard currency, helped stabilize developing countries’ balances of payments and increased their capacity for countercyclical macroeconomic policy.

Because of this, and also because the SDRs could be used to purchase vaccines and other health needs as well as other necessities, the SDR issuance saved many lives.

It is less discussed that the SDR allocation also helps the United States. This fact is important not only for Americans but for the rest of the world because — as explained above — it is the US government that decides whether the IMF will approve a new allocation and how much will be allocated.

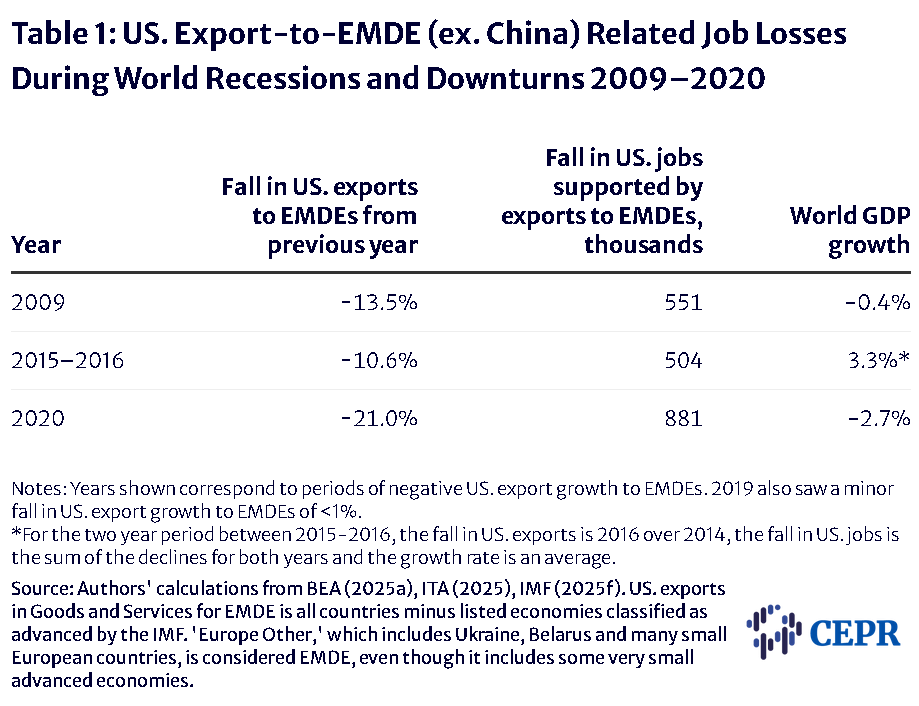

US exports of goods and services to EMDE countries amount to about $1.1 trillion annually.8 These directly support about 4.5 million US jobs.9 In this century in both the Great Recession and the pandemic-related downturn, between 1 and 2 million export-related jobs were lost in the US. A substantial proportion of these job losses were due to a falloff in imports from EMDEs. In the 2020 pandemic recession, for example, about 53 percent of the export-related US jobs lost — 881,000 of 1.7 million — were lost from exports to EMDE countries.

Policies that can help avoid these job losses are therefore important to the US as well as to other countries.

This paper estimates the number of US export-related jobs that could be saved by an allocation of SDRs. A lower bound, conservative estimate from the $209 billion EMDE share of 2021 would be about 41,000 jobs. But this estimate does not capture all the jobs that can be saved even with this allocation, and the jobs that can be saved also increase with the size of the allocation. An allocation of the size that was approved by the US House of Representatives would create about four times that many jobs or more than 160,000 jobs. And there are a range of possible allocations, since this creation of international reserve assets is completely costless to the United States and its budget — and for the rest of the world as well. For the United States, with a divided Congress that has trouble approving budgets, this could be a costless way to increase employment, and the export-related jobs pay more on average than other jobs for blue-collar workers.

Of course there is a pressing need for reform at the IMF — the United States should not have this overwhelming decision-making power at what is supposed to be a multilateral institution.

But SDR allocations can give developing countries more of a stake in trying to reform the organization. This analysis shows that there is a risk-free common interest of all member countries in the expansion of this life-saving policy.

For all of these reasons, and especially because of the lives that can be saved, the issuance of SDRs should become a regular, annual occurrence.10

On March 27, 2020, the managing director of the International Monetary Fund (IMF), Kristalina Georgieva, gave a press briefing following a conference call with the governing body of the IMF. The COVID pandemic was growing at an accelerating rate, with 2.6 billion people globally under some form of lockdown just weeks after the WHO declared that COVID had become a global pandemic.11 “It is now clear that we have entered a recession as bad or worse than in 2009,” Georgieva said.12

Turning to the developing world, Georgieva said: “Our current estimate for the overall financial needs of emerging markets is 2.5 trillion dollars. We believe this is on the lower end. We do know that their own reserves and domestic resources will not be sufficient. And it is in this context that our members are asking us to do more.”13

The $2.5 trillion that Georgieva was referring to was the amount that the IMF estimated was needed for developing countries to avoid balance of payments or fiscal crises.14 And she was right about the world recession of 2020 being much deeper than that of 2009, as measured by the contraction of real gross domestic product (GDP). In fact, it was, in per capita terms, the largest contraction since 1946.15

The day before, Georgieva had asked for help during an extraordinary G20 Leaders’ Summit:

And it is paramount we recognize the importance of supporting emerging market and developing economies to overcome the brunt of the crisis and help restore growth. They find themselves particularly hard hit by a combination of health crisis, sudden stop of the world economy, capital flight to safety, and — for some — sharp drop in commodity prices. These countries are the main focus of our attention.

She recommended a few measures that the IMF could take and asked for support from the G20 countries. One of them was to “boost global liquidity through a sizeable SDR (Special Drawing Right) allocation, as we successfully did during the 2009 global crisis.”17

This was the easiest and quickest practical way to help developing countries. The SDRs, international reserve assets created by the IMF that can be converted into hard currency, can be distributed to member countries within three weeks after they are approved by the IMF Board of Governors.

But there was one problem: according to the IMF charter, this decision requires an 85 percent majority of votes at the IMF Board of Governors, and the US has 16.5 percent of the votes,18 thus giving it unilateral veto power.19 And the US Treasury — which typically decides US policy and voting at the IMF — was not interested in using SDRs to help stabilize the global economy. The US Treasury announced its opposition in a statement to the IMF’s steering committee a few weeks later,20 and that was the end of the discussion.

As we will see, an SDR allocation, when Georgieva proposed it, would likely have saved hundreds of thousands of lives worldwide. But Washington said no.

Normally, it would not have surfaced again, given the US Treasury’s decisive power at the IMF. But this time, members of the US Congress intervened. As noted above, the managing director of the IMF had appealed for a sizable SDR issuance and had stated that developing countries had “financial needs” of at least $2.5 trillion. On that basis, House of Representatives members proposed and passed legislation on July 31, 2020, that required the administration to propose a new issuance by the IMF of SDRs worth $2.8 trillion.21 That put the SDR allocation back on the agenda and led — a year later — to the passage of a much smaller amount, which was still the largest in IMF history.

The 2021 allocation was $650 billion dollars, with $209 billion of this destined for developing countries, which the IMF refers to as emerging market and developing economies (EMDEs).22 According to US law, the Treasury can support, at the IMF, an SDR allocation without a vote of approval by Congress as long as the amount allocated to the US is at most equal to the US quota. At the exchange rate for SDRs to the dollar at the time, this roughly implied a total allocation of about $650 billion in 2021.23 (Note that the IMF Board of Governors has approved a quota increase of 50 percent that, when implemented, would allow the Treasury, without Congress, to support issuances of up to about $975 billion in the future.)24

We will return to SDR decision-making below, when we examine the US stake in SDR issuance and use and what this means for expanding SDRs’ role in stabilizing the world economy and saving lives going forward.

Before 2020, very little information could be found, even on the IMF website, that gave a basic explanation of what these assets are and how they work.25 The SDR is an international reserve asset created by the IMF and distributed to member countries in proportion to their IMF quotas. According to IMF rules, they can be converted into hard currency through voluntary trading arrangements facilitated by the IMF.26

Because high-income countries — or advanced economies, as the IMF calls them — have higher quotas in the aggregate, about 68 percent of a general issuance is allocated to them (and China).27 However, in general, high-income countries cannot use their SDRs.28 No resources are wasted when 68 percent of the allocation goes to high-income countries (and China).

Nonetheless, there is a real need for reform such that all SDRs in an allocation are distributed only to developing countries. This would more than triple the aid for EMDEs that is provided in an allocation of SDRs, such as the $650 billion in 2021.

Although the distribution issue has not been fixed, the support that EMDE countries received in 2021 was quite large. The $209 billion was more than all of the official development aid that these countries received from the 33 country members of the Development Assistance Committee (DAC) in that year,29 and unlike much of international development aid, it came without debt and without conditions attached.

Since the probability of default on SDRs is at least as low, or lower than, almost any other international financial asset, SDRs can play much of the same role as any of the safest international reserve assets that a government can hold. By having more SDRs, countries have a lower risk of balance of payments crises or fiscal crises; they may also have lower borrowing costs.30 In addition, some countries will, after receiving the SDRs, sell off other liquid assets (for example, US Treasury notes or bonds) to get immediate cash.

SDRs can also be used by countries who have IMF programs to pay debt service and principal payments to the IMF, thus freeing up more foreign exchange for other needs, including the urgent needs that they had during the pandemic recession. The IMF recorded that the 2021 issuance helped 55 countries to make repayments totaling $39 billion (27.5 billion SDRs) to the IMF.31

We don’t know exactly how much of these repayments came directly as a result of the SDRs received by developing countries in 2021, but the date of the report (2023) and the size of the 2021 allocation relative to prior SDR holdings indicates that it was probably a large proportion. And $38 billion is a large sum — it amounts to 18 percent of the $209 billion worth of SDRs that EMDEs received in 2021.32 Since the IMF is a “preferred creditor” that must be paid, this is a significant opening of fiscal space to developing countries for countercyclical macroeconomic policy.33

The IMF has often imposed procyclical fiscal and monetary policies.34 SDRs could provide significant benefits by allowing countries to avoid IMF programs and their associated procyclical policies. The case of Argentina is one of the most striking recent examples. The profound failure of procyclical macroeconomic policies attached to the largest IMF loan ever ($57 billion in 2018) continues to reverberate and grow today.35 Argentina already accounts for 44 percent of the $125 billion of IMF loans from the General Resources Account36 and is accumulating tens of billions more of multilateral debt this year to stay afloat.

Also, as will be examined below, a large part of the last issuance was used for fiscal purposes, which allowed governments to directly engage in countercyclical, expansionary fiscal policy when needed. The strengthening of countries’ external financial positions provided by the addition to central bank reserves also allows for more options with regard to countercyclical monetary policy.

The most important impact that SDRs can have in developing countries is to save lives. This impact can be quite large — even in the hundreds of thousands — during a global recession or downturn.

This was true during the record severity of the 2020 global pandemic recession that had just begun when IMF Managing Director Kristalina Georgieva made her appeal for a large issuance of SDRs. In such a situation, the additional reserves provided by an SDR issuance can have an even greater impact on reducing mortality than they would normally.

Economists at the Bank for International Settlements (BIS) have estimated the impact of recessions on mortality in developing economies.37 They estimated that a typical recession in a developing country would increase mortality by 0.5 deaths per 1,000 people. A large and disproportionate number of these deaths are children less than five years old. This is partly because these recessions often lead to reduced food availability. This causes children to be malnourished; and malnourished children are much more likely to die from childhood diseases, including pneumonia, measles, and diarrhea, which would not otherwise be fatal.38 There are multiple other channels through which lives can be lost during recessions due to loss of income, medicine, and public health needs.

How much would we expect mortality to increase in developing countries during a recession similar to the 2020 global pandemic recession? We can use the BIS estimates to answer this question. For the present study we are focused on mortality that is caused by a recession or economic downturn. Therefore, we are considering a recession in EMDEs as large as the 2020 global recession, but only estimating deaths caused by the recession, not deaths due to a pandemic.

The first step is to calculate the total population of this group of countries but only for the countries that were actually in a recession in 2020. For their statistical estimates, the BIS economists defined recession as having negative real GDP growth for the year. Summing the populations of the EMDE countries that were in recession in 2020 yields a total population of 3.88 billion people.

To estimate the increase in deaths in these countries, we multiply by the expected increase in the mortality rate due to recession, namely 0.5 deaths per 1,000 people. This yields an estimate of 1.94 million deaths in EMDEs if a recession as large as that of 2020 were to happen. Again, these are not deaths due to any pandemic; they are deaths that would result from the impact of recession.

As discussed in this paper, whether SDRs are simply saved as additional reserves or put to fiscal use, there are numerous ways in which they could reduce both the frequency and severity of individual recessions. This includes reducing the risk of balance of payments and fiscal crises, opening more policy space for countercyclical macroeconomic policy, paying off billions of dollars of debt to the IMF, and other channels examined here. SDRs could also reduce mortality from recessions by allowing for more spending on health care, food, and medicine than would otherwise be possible in a downturn.

How many lives would have been saved in a global downturn the size of the one that occurred in 2020, if SDRs had been issued in March of that year? That is when the Managing Director of the IMF, backed by the Fund and almost all of the member countries, called for a very large issuance. First we consider the percentage of their new SDRs that EMDE countries spend on fiscal use, which is estimated at 40 percent.39 We can estimate how much this would be expected to increase GDP. This can be used to calculate a rough estimate of the resulting reduction in mortality. If we assume a linear relationship between the lost GDP in the recession and the resulting increase in mortality, then 283,000 of the estimated 1.94 million deaths attributed to the impact of the 2020 recession would have been saved, had the US Treasury supported a 2020 issuance, as IMF Managing Director Georgieva had called for, and the US House had passed legislation requiring the US Treasury to support at the IMF.40

Note that this is a rough estimate, and the actual number is likely to be substantially higher for several reasons. First, as noted above, the 60 percent of the SDRs that are placed in reserves can in some countries significantly lower the probability of balance of payment crises; the latter can cause or contribute to severe recessions as well as high inflation or hyperinflation; as well as fiscal crises. Avoiding or even reducing the severity of these adverse outcomes would of course reduce mortality, even when the reserves are not converted to cash for spending. Second, the use of a linear extrapolation of the impact of reducing the severity of recession (due to the fiscal use of SDRs) would also produce an underestimate of the lives saved. Normally we would expect that economies in a deeper recession would respond more to a stimulus of the type provided by the SDRs fiscal use.41 So we would expect the positive impact of SDRs to increase at an increasing rate relative to the depth of the recession, rather than a linear relationship.

The global health situation, particularly in Global South or EMDE countries, has become much more acute with the scale of the Trump administration’s foreign aid cuts with almost 50 percent of the USAID budget having been slashed.42 Recent research in The Lancet estimates that 14 million lives could be lost by 2030 because of this cut in support for health-care programs, especially ones targeting HIV/AIDS, malaria, and neglected tropical diseases like dengue and chikungunya.43 The need to make up for this loss of billions of dollars for life-saving health care and medicines is one of the most important health crises in the world in terms of the estimated human cost.

This estimate of 283,000 lives that could have been saved in 2020 with an SDR issuance is very large but does not include all of the channels by which this increase in international reserves would be expected to save lives. And we are considering only the immediate impact of such an addition to reserves in the year that follows. In reality, this measure would have impacts that continue into the next year and beyond. For example, a country would reduce mortality if it is able to improve its access to clean water or improve other health-related infrastructure.

Of course, if the IMF’s managing director and the US House of Representatives had prevailed in getting what they had sought — the legislation passed by the US House of Representatives mandated that the US Treasury support an allocation more than four times as large as what the IMF approved in the following year — some multiple of the 283,000 lives considered here would likely have been saved.

EMDE countries also need the help that SDRs can bring because of the economic risks and perilous debt situation that these countries are currently facing. As of March 2025, 59 out of 68 developing countries for which the IMF publishes debt sustainability analyses were currently either in debt distress or at medium-to-high risk thereof.44 The rise in global interest rates, driven primarily by the US Federal Reserve’s policy rate hikes from 0.25 percent in 2022 to 5.5 percent in 2023, significantly increased the cost of debt for EMDEs. External debt service now represents at least 8.6 percent of public revenues in half of all developing countries, almost double the amount of 2010.45

The rise in the cost of debt has funneled scarce resources away from critical investments in health, infrastructure, education, and climate adaptation, among other public services.46 Because external debt is denominated in foreign currencies, unsustainable payments decrease EMDEs’ ability to afford imports, including basic needs like food and medicine. Insufficient development and climate finance contribute to unsustainable debt burdens. When EMDEs were issued $209 billion from the 2021 SDR allocation, it was more than twice as much as they received in climate finance that year — $89 billion, most of which, unlike SDRs, was in the form of debt.47

As noted above, high-income countries generally do not have any use for SDRs. But it turns out that the positive impact that SDRs have on developing countries that can use them — especially during economic downturns — can be significant, even for an economy as large as the United States. About 10.2 million Americans work jobs directly or indirectly supported by exports, and these are jobs that tend to have higher than average rates of pay for blue-collar workers and those without college degrees, including in manufacturing and services.48

In a global downturn or recession, the United States can lose millions of export-related jobs. In 2009, the global economy contracted by 0.4 percent, and the US Department of Commerce’s International Trade Administration (ITA) estimates that 1.4 million US jobs were lost due to the falloff in US exports. In the 2020 pandemic recession, global GDP fell by 2.7 percent, and 1.7 million export-related jobs were lost.49

The loss of exports to EMDEs has been responsible for a sizable fraction of the fall in US export-supported jobs in these downturns (Table 1).50 In the 2020 pandemic recession about 53 percent of the export-related U.S. jobs lost — 881,000 of 1.7 million — were lost from exports to EMDE countries. This means that a large number of jobs in the US can be saved, or created, by policies that help stabilize EMDE economies so their imports do not shrink as much in the face of a global downturn or other economic shocks. One of the biggest things that the US can do to stabilize EMDE economies, at no cost to the United States or any other government (or economy), is to facilitate a large new issuance of SDRs at the IMF. This is very quick and easy for the US government to do, as it was in 2021 when there was almost no opposition to the US proposal from the other member countries. In terms of need, the situation for approval today is not significantly different.

We now look at the estimated impact on US jobs in more detail.

The United States exported $1.1 trillion worth of goods and services to EMDEs in 2024.51 According to the estimates of the ITA of the US Department of Commerce, approximately 4,100 export-related jobs are created in the United States for each billion dollars of additional exports.52 Thus, EMDE exports support about 4.5 million US jobs, and an increase in US exports to EMDEs of 1 percent, or $11 billion dollars, would add 45,100 export-related jobs.

Here we estimate the amount by which these EMDE countries increase their imports from the United States as a result of a new allocation of SDRs. We start with a very low conservative estimate. The roughly $650 billion worth of SDRs that the US Treasury can support at the IMF without a congressional vote would provide about $209 billion worth of SDRs to EMDEs.

On the basis of what happened after the 2021 SDR allocation, the data show that about 60 percent of these new SDRs (worth $125.4 billion) were added to the international reserves of the EMDE governments and not used for fiscal purposes.53 This 60 percent of new reserves remain as they were received: as SDRs, a trusted international reserve asset. But they would lead to an increase in these countries’ imports through a number of channels.

Having sufficient international foreign exchange reserves is important for governments because they must be able to pay for essential imports and debt service in dollars. About 58 percent of central bank international foreign exchange reserves are dollar-denominated reserves.54 Most of the rest are denominated in other hard currencies. About half of trade globally, rising to over 70 percent in all regions of the world except for Europe, is invoiced in dollars.55 When governments run low on these international reserve assets, they can face higher borrowing costs; can have trouble rolling over the principal on their debt; and can even have balance of payments or fiscal crises, even hyperinflation, as capital flees the country.

SDRs are not a currency, but since they can be relatively easily converted to hard currency, including dollars, they are seen as an extremely safe international reserve asset by investors.

These features of SDRs lead to more economic stability and growth than might otherwise occur and therefore lead to additional imports by EMDE countries.56

A central estimate of the elasticity of imports with respect to reserves in the economic literature for developing countries is about 0.2.57

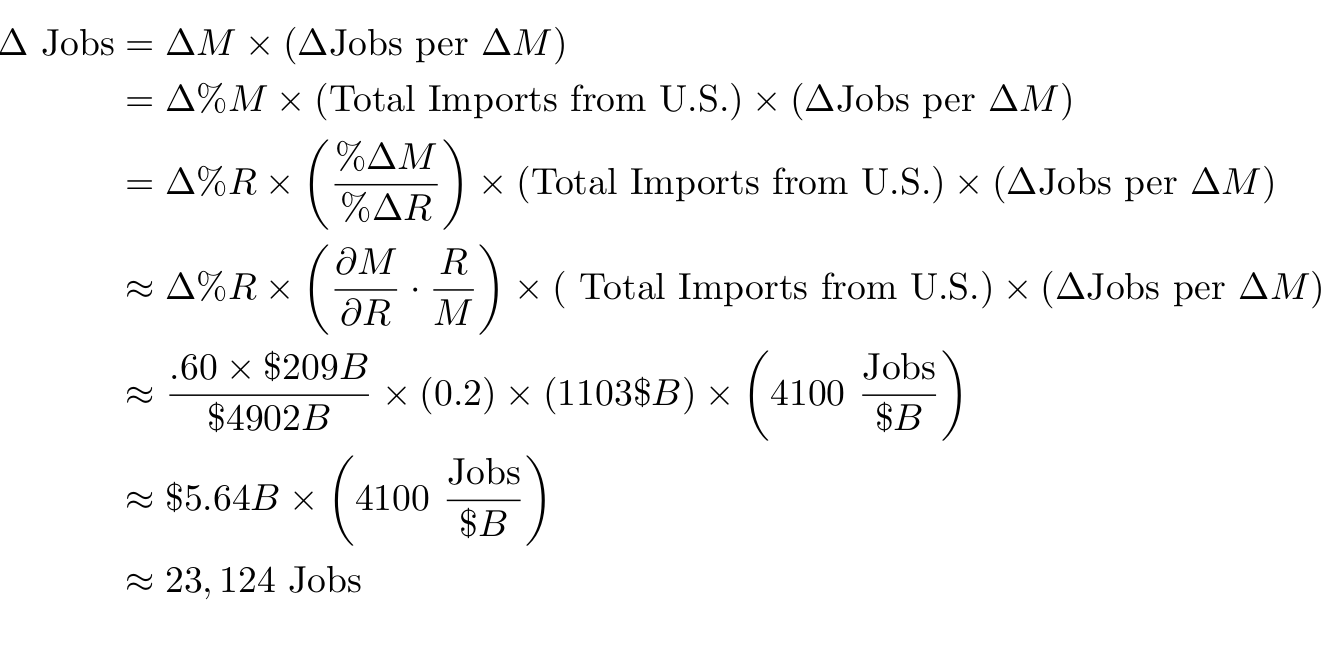

Thus, if EMDEs hold 60 percent of their new SDR allocation as international reserves, this would generate $5.64 billion in new imports from the United States.58 According to ITA estimates, this would create 23,000 additional jobs.

The remaining 40 percent of the new SDRs are used for fiscal purposes. This would include government spending on essential imports, including vaccinations and medicine during the COVID pandemic,59 or a countercyclical economic stimulus in a slowing economy or recession. To calculate the estimated impact of this part of the SDRs on imports, we first note that the multiplier of this spending is estimated at 1.0.60 This means that we would expect the amount of GDP growth from this spending to be equal to the additional spending itself. We therefore need an estimate of the elasticity of EMDE imports with respect to income (i.e., with respect to GDP), alternatively called the income elasticity of imports.

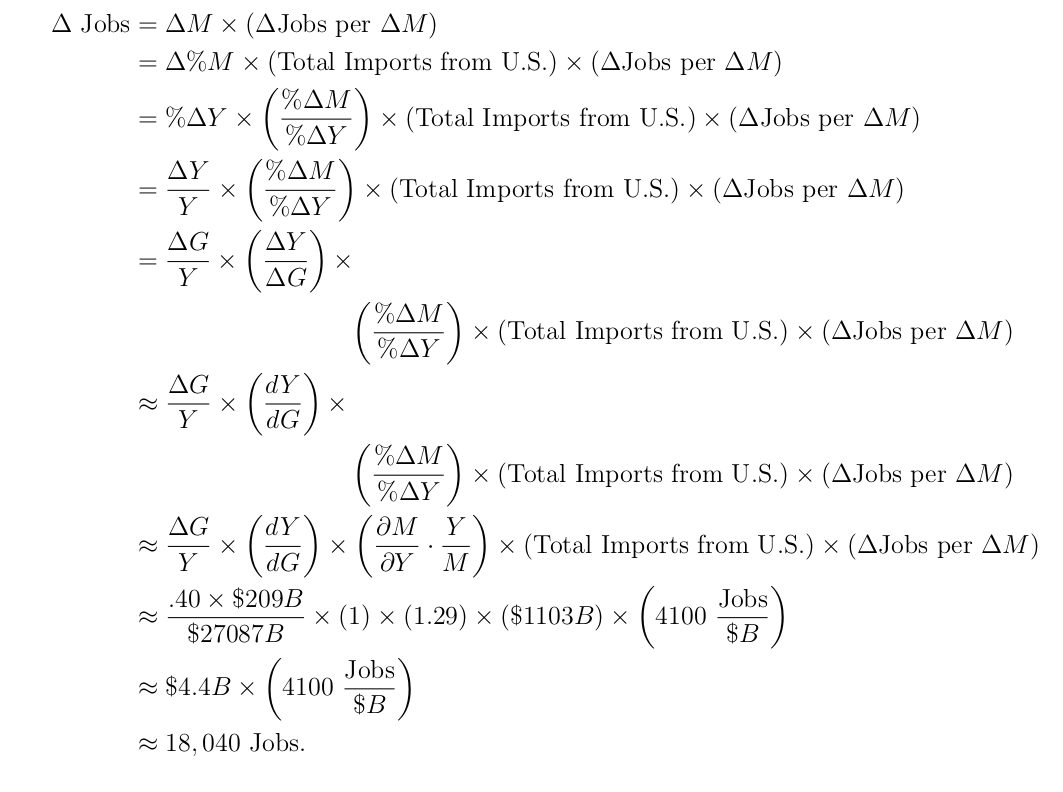

The elasticity of EMDE imports with respect to GDP is estimated at 1.29. (See Appendix II for details.) We calculate the estimated percentage increase in GDP to be 0.31 percent, and we would therefore expect EMDE imports from the United States to increase by 0.40 percent for this 40 percent of the reserves that go to fiscal use.61 This would amount to $4.4 billion of additional imports. At 4,100 jobs per billion dollars of exports, that would be 18,000 export-related jobs in the US.

Thus the total for this calculation would be about 41,000 export-related jobs in the US. When the quota increase, which as noted above was approved in 2023, is implemented, this would rise to about 62,000 additional export-related jobs.

The estimate here is based on very conservative assumptions; the main purpose is to illustrate the mechanics of what could happen with an SDR issuance of $650 billion, the maximum that is allowed by US law without a vote of Congress. But the US House of Representatives approved more than four times that much, and it was just a couple of votes away from passing the Senate. So it is a real possibility that it could be passed in the near future, especially if the executive branch were to endorse it. There is no telling when that might happen; the current administration has not said no to a new issuance.

In any case, a larger issuance could easily push the number of jobs created in the United States well into the hundreds of thousands, and as noted above, these are jobs with a higher proportion of better-paying blue-collar jobs. This would provide a significant additional incentive for the US government to support such an issuance.

With a divided Congress that has difficulties agreeing on budget issues, an administration that wants to create jobs may find this to be one of the easiest paths to that goal, since it has zero cost to the budget. And as noted above, it can be done very quickly.

This overwhelming weight of the US decision-making and political process is clearly not the way a multilateral institution is supposed to work. It is a legacy of 80 years ago, like the gentlemen’s agreement (not included in any written rule or bylaw) that the IMF managing director is always a European and the World Bank president, an American. The rules and customs were formulated when the United States was the overwhelmingly preeminent industrial power and much of the world did not consist of independent countries.

But the experience of recent years has shown that the US’s decision-making on this issue can be influenced by the US Congress, an important part of which is willing to listen to the arguments of civil society at home and also to the rest of the world.

The role of the US Congress appeared to be decisive in winning this record-size issuance of SDRs. As noted above, the SDR issuance proposed by the IMF managing director in March 2020 was first blocked by the US Treasury, but the approval of a $2.8 trillion-worth issuance by the US House of Representatives put it back on the agenda. In the year that followed, there was continued intensive lobbying of Congress, including the Senate. A coalition of more than 100 organizations, which included organized labor and major religious institutions representing tens of millions of constituents, was involved.62 After Joe Biden was elected president in November 2020, these organizations, along with members of Congress, continued to push the incoming administration. But in public statements, the administration of the new president-elect — unlike their party in Congress — would not endorse a new issuance of SDRs for three months, until February 25.63 All of this indicates that the US Congress made the difference.64

This of course will never be a substitute for an actual multilateral institution. But the unprecedented experience of 2020–2021 shows that life-saving harm reduction is possible even before the IMF is reformed.

The data and analysis here show how important SDRs can be to developing countries, especially in a time of world recession or downturn. The most consequential implication here is that if the $650 billion issuance that was distributed in August 2021 had been made in March 2020, when the IMF managing director, Kristalina Georgieva, and almost all member governments wanted it to be done, it is likely that hundreds of thousands of lives could have been saved.

Georgieva was seeking something more than four times larger, based on IMF research. This could have saved even more lives, a multiple of the 283,000 lives that a $650 billion-worth issuance could likely have saved in 2020.

The finding here that an SDR issuance can create jobs in the US, proportionately to the size of the issuance, could increase the likelihood of another issuance in the near future.

Nonetheless, this latest issuance is the largest ever and is potentially of historic importance going forward. The 2021 issuance had important positive impacts, including the saving of many lives, and no significant downside risks.

SDRs can begin to narrow the huge gap in policy space between high-income countries and EMDEs to allow them to recover in the face of global downturns and negative economic shocks. When the Great Recession hit the United States at the end of 2007, the US was able to cut interest rates to near zero for about seven years and deploy trillions of dollars of quantitative easing. The response to the 2020 pandemic recession was much stronger, with budget deficits of 15 percent of GDP in 2020 and 12.4 percent of GDP in 2021, zero interest rates, and $13 trillion in quantitative easing for the two years. Needless to say, developing countries don’t have the same options.

Of course there is a pressing need for reform at the IMF. The United States should not have either the absolute veto power that it has over this and other important decisions. Nor should it have the near-absolute power, allied with other high-income countries, over almost all decisions.

But SDR issuances can give developing countries more of a stake in trying to reform the IMF so that more countries can have a voice. Since SDR issuance helps stabilize the world economy and increases EMDE imports from both high-income countries and other EMDEs, all member countries share a common interest in expanding this life-saving policy. This is especially true since there is no cost to the governments of the high-income countries.

For all of these reasons, and especially because of the lives that can be saved, the issuance of SDRs should become a regular, annual occurrence.65

The total allocation is assumed to be $650 billion US worth of SDRs. Of this, $209 billion worth of SDRs would be allocated to EMDEs other than China, as occurred for the 2021 allocation.

As noted, we can expect that 60 percent of the reserves allocated to EMDEs other than China would be added to the international reserves of the EMDE governments and would remain as reserves. The other 40 percent of the new SDRs are assumed to be used for fiscal purposes.

In the next two sections, we will estimate the additional number of US jobs created due to these two categories of changes and then finally add the results from each section to get a total estimated number of US jobs created.

In this section, we estimate the number of additional export-related jobs resulting from the 60 percent of the SDR allocation expected to remain as reserves; note that this excludes the effect from the SDRs assumed to go to fiscal use. We first estimate the percentage change in total reserves due only to this 60 percent of the allocation for EMDEs excluding China.

To do so, we first calculate the total foreign reserves for EMDEs excluding China. The quantity of foreign reserves for all EMDEs (including China) is 6.412 trillion SDRs.66 We use the exchange rate of SDRs to US dollars to convert to dollars; namely, 1.30413 dollars per SDR.67 The total foreign reserves for China is $3.46 trillion.68 Thus we obtain an estimate of 6,412B * 1.30413 − 3,460B = 4,902 billion dollars of total foreign reserves for the EMDEs excluding China.

The added SDRs that we estimate to remain as reserves, that is, that will not be used for fiscal expenditures, are 0.60 * $209B = $125.4B. Thus the percentage change in total foreign reserves for the EMDEs excluding China is 125.4/4902 = 2.56 percent.

We multiply by the estimated elasticity 0.2 from the literature69 to obtain the estimate that the percentage change in imports is 0.2 * (2.56 percent) = 0.511 percent.

Now we need to compute the implied absolute change in imports. Total imports in 2024 from the US to EMDEs other than China was $1.103 trillion.70 Thus the estimated absolute change in imports is 0.511 percent * $1.103 trillion = $5.64 billion.

According to estimates of the ITA of the US Department of Commerce, approximately 4,100 export-related jobs are created in the United States for each billion dollars of additional exports.71 So, for example, an increase in US exports of 1 percent, or $11 billion, would add 45,100 export-related jobs.

Therefore, the estimated change of imports of $5.64 billion translates into an estimated (5.64 * 4,100) = 23,124 jobs.

We can write this down all in one set of equations by writing the following: M denotes

imports to EMDEs (other than China) from the US, and (∂M/∂R)(R/M) denotes the elasticity of imports with respect to reserves, which is well-known to approximate the ratio of the percentage change of imports to the percentage change of reserves (for small changes). Note also that we make the simplifying assumption that the quantity of imports from the US to each country increases by the same percentage as the overall level of imports to each country.

In this section, we estimate the number of additional export-related jobs resulting from the 40 percent of the SDR allocation expected to go to fiscal use.

We start with the estimate that the total fiscal spending of EMDEs excluding China will increase by the quantity 0.4* ($209B) = $83.6 billion.

We assume a fiscal multiplier of 1.72 Therefore, we estimate the total GDP of EMDEs excluding China to increase by the same amount as the fiscal spending; namely, $83.6 billion.

We estimate GDP for all EMDEs excluding China at $27.087 trillion.73 Thus the estimate of the percentage change in increased GDP from the reserves that went to fiscal use is 0.31 percent (= 83.6/27,087) of the total GDP of all EMDEs excluding China.

We use the elasticity of imports with respect to income (i.e., GDP) from the literature of 1.2974 and therefore estimate an increase in the percentage of imports of (1.29 * 0.31 percent) = 0.40 percent.

So in turn we estimate that the quantity of imports from the US to all EMDEs excluding China would increase by (0.40 percent) * $1.103 trillion = $4.4 billion.

Multiplying by the estimate of 4,100 jobs per billion dollars, we estimate that the increase from fiscal use would be 4.4 * 4,100 = 18,040 jobs.

We can write this down all in one set of equations by writing the following: here M denotes

imports to EMDEs (other than China) from the US, Y denotes GDP (i.e., income), G denotes fiscal spending — that is, government spending — and (∂M/∂Y)(Y/M) denotes the elasticity of imports with respect to GDP/income, which is well-known to approximate the ratio of the percentage change of imports to the percentage change of GDP/income (for small changes). And finally, (dY)(dG) denotes the fiscal multiplier, which approximates the ratio of the change of GDP to the change of government expenditures (for small changes). Note also that, as we did above, we make the simplifying assumption that the quantity of imports from the US to each country increases by the same percentage as the overall level of imports to each country.

We now sum the two estimates to get our total estimate of increased US jobs due to an SDR allocation. We thus get the final estimate:

23,124 + 18,040 = 41,164 new jobs.

We arrive at our estimate for the elasticity of imports with respect to income (i.e., with respect to GDP) from a recently published article by El-Shagi, Sawyer, and Tochkov in the Pacific Economic Review (2022).75 The study presents a meta-analysis of over 600 income elasticity of import demand estimates drawn from 152 papers covering 105 countries between 1975 and 2014.

The authors employ quantile regressions to estimate the distribution of income elasticities across different country groupings and focus specifically on differences by income level. Their methodology controls for variation in model specification and estimation technique, allowing for a consistent comparison across studies. In particular, they estimate how income elasticity varies across World Bank income classifications — low-income (LI), lower-middle-income (LMI), upper-middle-income (UMI), and high-income (HI) — with high-income countries serving as the reference group.

Based on their results (specifically, the median quantile regression estimates controlling for model structure), the most reasonable income elasticity values to adopt for modeling purposes by income level are as follows.

| Income Level | Median Income Elasticity |

| Low income (LI) | 1.16 |

| Lower-middle income (LMI) | 1.29 |

| Upper-middle income (UMI) | 1.35 |

Given that “developing countries” as commonly defined by the IMF and World Bank include low-, lower-middle-, and upper-middle-income economies, it is also reasonable to compute a weighted average elasticity to represent the group as a whole. Using our own estimates of the distribution of developing countries by income level — 19.4 percent low-income, 39.5 percent lower-middle-income, and 41.1 percent upper-middle-income — the implied aggregate income elasticity of import demand for developing countries is approximately

0.194 * 1.16 + .395 * 1.29 + .411 * 1.35 = 1.29.

A key caveat is that the authors do not provide a full list of the countries included in their meta-sample. As a result, the income-group weights used here may not precisely match the composition of their study sample. However, they represent a reasonable approximation for the purpose of deriving an aggregate elasticity estimate for developing countries.

Action Corps et al. 2020. “Support for the Robust International Response to Pandemic Act (H.R.6581).” https://docs.google.com/document/d/1R2umgTDYtM6h7OqkTmIx8i9BXmlr39rekvRj6X2i7Gs/edit?usp=sharing.

Arize, Augustine C., and John Malindretos. 2012. “Foreign exchange reserves in Asia and its impact on import demand.” International Journal of Economics and Finance 4, no. 3 (2012): 21–32.

Arize, Augustine C., and Srinivas Nippani. 2010. “Import demand behavior in Africa: Some new evidence.” The Quarterly Review of Economics and Finance 50, no. 3 (2010): 254–263.

Arize, Augustine C., and Thomas Osang. 2007. “Foreign exchange reserves and import demand: Evidence from Latin America.” World Economy 30, no. 9 (2007): 1477–1489.

Auerbach, Alan J., and Yuriy Gorodnichenko. 2012. “Measuring the output responses to fiscal policy.” American Economic Journal: Economic Policy 4.2 (2012): 1-27.

Baird, Sarah, Jed Friedman, and Norbert Schady. 2011. “Aggregate income shocks and infant mortality in the developing world.” Review of Economics and Statistics 93, no. 3 (2011): 847–856. https://www.researchgate.net/profile/Jed-Friedman-2/publication/227629244_Aggregate_Income_Shocks_and_Infant_Mortality_in_the_Developing_World/links/59078ce0a6fdccd580dcb6e8/Aggregate-Income-Shocks-and-Infant-Mortality-in-the-Developing-World.pdf.

Bertaut, Carol, Bastian von Beschwitz, and Stephanie Curcuru. 2023. “The International Role of the U.S. Dollar: Post‑COVID Edition.” FEDS Notes. Board of Governors of the Federal Reserve System. https://doi.org/10.17016/2380-7172.3334.

Black, Robert E., Lindsay H. Allen, Zulfiqar A. Bhutta, Laura E. Caulfield, Mercedes De Onis, Majid Ezzati, Colin Mathers, and Juan Rivera. 2008. “Maternal and child undernutrition: Global and regional exposures and health consequences. The Lancet 371, no. 9608 (2008): 243–260.

Black, Robert E. et al. 2013. “Maternal and child undernutrition and overweight in low-income and middle-income countries.” The Lancet 382, no. 9890, 427–451. https://www.thelancet.com/journals/lancet/article/PIIS0140-6736(13)60937-X/abstract.

Board of Governors of the Federal Reserve System. 2025. “Summary of Economic Projections.” June 18. https://www.federalreserve.gov/monetarypolicy/files/fomcprojtabl20250618.pdf.

Cashman, Kevin, Andrés Arauz, and Lara Merling. 2022. “Special Drawing Rights: The Right Tool to Use to Respond to the Pandemic and Other Challenges.” Challenge 65, nos. 5–6: 176–198. https://doi.org/10.1080/05775132.2022.2134638.

Cavalcanti, Daniella Medeiros, Lucas de Oliveira Ferreira de Sales, Andrea Ferreira da Silva, Elisa Landin Basterra, Daiana Pena, Caterina Monti, Gonzalo Barreix et al. 2025. “Evaluating the impact of two decades of USAID interventions and projecting the effects of defunding on mortality up to 2030: A retrospective impact evaluation and forecasting analysis.” The Lancet 406, no. 10500: 283–294. https://www.thelancet.com/journals/lancet/article/PIIS0140-6736(25)01186-9/fulltext.

Central Bank of the People’s Republic of China. 2025. “Official Reserve Assets.” http://www.pbc.gov.cn/eportal/fileDir/diaochatongjisi/resource/cms/2025/01/2025010716000971240.htm.

Chauhan, Shaylika. 2020. “Comprehensive review of coronavirus disease 2019 (COVID-19).” Biomedical Journal 43, no. 4: 334–340.

Chletsos, Michael, and Andreas Sintos. 2023. “The effects of IMF conditional programs on the unemployment rate.” European Journal of Political Economy 76: 102272.

de Onis, Mercedes, and Francesco Branca. 2016. “Childhood stunting: A global perspective.” Maternal & Child Nutrition 12, no. S1. https://onlinelibrary.wiley.com/doi/full/10.1111/mcn.12231.

Doerr, Sebastian, and Boris Hofmann. 2020. Recessions and mortality: A global perspective. BIS Working Papers No. 910, Bank for International Settlements, December.

El-Shagi, Makram, William C. Sawyer, and Kiril Tochkov. 2022. “The income elasticity of import demand: A meta-survey.” Pacific Economic Review 2022, no. 27: 18–41. https://doi.org/10.1111/1468-0106.12357.

Food Security Information Network (FSIN) and Global Network Against Food Crises (GNAFC). 2025. Global Report on Food Crises 2025. Rome. https://doi.org/10.71958/wfp130664.

Galant, Michael. 2022. “Righting the Record: Claims that SDRs ‘Help US Enemies’ Are Baseless.” Washington, DC: Center for Economic and Policy Research, April 14. https://cepr.net/publications/righting-the-record-claims-that-sdrs-help-us-enemies-are-baseless/.

Geli, José Federico, and Afonso S. Moura. 2023. Getting into the Nitty-Gritty of Fiscal Multipliers: Small Details, Big Impacts. International Monetary Fund.

H.R. 7617, 116th Cong. 2020. Defense, Commerce, Justice, Science, Energy and Water Development, Financial Services and General Government, Labor, Health and Human Services, Education, Transportation, Housing, and Urban Development Appropriations Act, 2021. https://www.congress.gov/bill/116th-congress/house-bill/7617/text.

H.R. 8406, 116th Cong. 2020. Making emergency supplemental appropriations for the fiscal year ending September 30, 2021, and for other purposes. https://www.congress.gov/bill/116th-congress/house-bill/8406/text.

H.R. Rept. No. 117–110. 2021. Providing for Consideration of the Bill (H.R. 4346) Making Appropriations for Legislative Branch for the Fiscal Year Ending September 30, 2022, and for Other Purposes; Providing for Consideration of the Bill (H.R. 4373) Making appropriations for the Department of State, Foreign Operations, and Related Programs for the Fiscal Year Ending 30, 2022, and for Other Purposes; and Providing for Consideration of the Bill (H.R. 4505) Making Appropriations for the Departments of Commerce and Justice, Science, and Related Agencies for the Fiscal Year Ending September 30, 2022, and for Other Purposes. https://www.congress.gov/committee-report/117th-congress/house-report/110.

High-Level Advisory Board on Effective Multilateralism (HLAB). 2023. “A Breakthrough for People and Planet: Effective and Inclusive Global Governance for Today and the Future.” New York: United Nations University. https://unu.edu/sites/default/files/2025-02/highleveladvisoryboard_breakthrough_fullreport.pdf.

Initiative for Policy Dialogue (IPD) and the Pontifical Academy of Social Sciences ( PASS). 2025. “Launch of Jubilee Report – Afternoon Session.” Initiative for Policy Dialogue, YouTube, June 23. Video, 3 hr., 47 min., 45 sec. https://www.youtube.com/watch?v=F28tZwMuy1Y.

International Monetary Fund (IMF). 2008. “IMF Survey: IMF Outlines Three Lines of Defense for Global Economy.” April 9. https://www.imf.org/en/News/Articles/2015/09/28/04/53/sopol040908a.

———.2019. “2018 Review of Program Design and Conditionality.” Policy Papers, May. https://www.imf.org/en/Publications/Policy-Papers/Issues/2019/05/20/2018-Review-of-Program-Design-and-Conditionality-46910.

———.2020a. “Articles of Agreement.” Article XIX, §3. https://www.imf.org/external/pubs/ft/aa/index.htm.

———.2020b. “Enhancing the Emergency Financing Toolkit—Responding To The COVID-19 Pandemic.” Policy Papers, April. https://www.imf.org/en/Publications/Policy-Papers/Issues/2020/04/09/Enhancing-the-Emergency-Financing-Toolkit-Responding-To-The-COVID-19-Pandemic-49320.

———.2020c. “Remarks by IMF Managing Director Kristalina Georgieva During an Extraordinary G20 Leaders’ Summit.” Press Release No. 20/108, March 26 https://www.imf.org/en/News/Articles/2020/03/26/pr20108-remarks-by-imf-managing-director-during-an-extraordinary-g20-leaders-summit.

———.2020d. “Transcript of Press Briefing by Kristalina Georgieva following a Conference Call of the International Monetary and Financial Committee.” March 27. https://www.imf.org/en/News/Articles/2020/03/27/tr032720-transcript-press-briefing-kristalina-georgieva-following-imfc-conference-call.

———.2021a. “2021 General SDR Allocation.” August 23. https://www.imf.org/en/Topics/special-drawing-right/2021-SDR-Allocation.

———.2021b. “IMF Executive Directors Discuss a New SDR Allocation of $650 billion to Boost Reserves, Help Global Recovery from COVID-19.” March 23. https://www.imf.org/en/News/Articles/2021/03/23/pr2177-imf-execdir-discuss-new-sdr-allocation-us-650b-boost-reserves-help-global-recovery-covid19.

———.2021c. “IMF Governors Approve a Historic $650 Billion SDR Allocation of Special Drawing Rights.” August 2. https://www.imf.org/en/News/Articles/2021/07/30/pr21235-imf-governors-approve-a-historic-us-650-billion-sdr-allocation-of-special-drawing-rights.

———.2021d. “Questions and Answers on Special Drawing Rights.” August 23. https://www.imf.org/en/About/FAQ/special-drawing-right.

———.2021e. “Special Drawing Rights.” August 23. https://www.imf.org/en/Topics/special-drawing-right.

———.2023a. “2021 Special Drawing Rights Allocation—Ex-Post Assessment Report.” Policy Papers, August. https://www.imf.org/en/Publications/Policy-Papers/Issues/2023/08/28/2021-Special-Drawing-Rights-Allocation-Ex-Post-Assessment-Report-538583.

———.2023b. “IMF Board of Governors Approves Quota Increase Under 16th General Review Quotas.” December 18. https://www.imf.org/en/News/Articles/2023/12/18/pr23459-imf-board-governors-approves-quota-increase-under-16th-general-review-quotas.

———.2023c. “Tracker on the Use of Allocated SDRs.” April 21. https://www.imf.org/en/Topics/special-drawing-right/SDR-Tracker.

———.2023d. “World Economic Outlook Database: Groups and Aggregates Information.” April. https://www.imf.org/en/Publications/WEO/weo-database/2023/April/groups-and-aggregates.

———.2024. “IMF Annual Report 2024.” Appendix I. August. https://cdn.sanity.io/files/yg4ck731/production/e2b836d46e7640286f7551ed344a28ecebbae717.pdf/Appendices.pdf.

———.2025a. “Argentina: Ex-post Evaluation of Exceptional Access under the 2022 Extended Fund Facility Arrangement-Press Release; Staff Report; and Statement by the Executive Director for Argentina.” Country Reports, January. https://www.imf.org/en/Publications/CR/Issues/2025/01/11/Argentina-Ex-post-Evaluation-of-Exceptional-Access-under-the-2022-Extended-Fund-Facility-560748.

———.2025b. “Currency units per SDR for December 2024.” https://www.imf.org/external/np/fin/data/rms_mth.aspx?SelectDate=2024-12-31&reportType=CVSDR.

———.2025c. “IMF Members’ Quotas and Voting Power, and IMF Board of Governors.” https://www.imf.org/en/About/executive-board/members-quotas.

———.2025d. “Special Drawing Rights (SDRs) Allocations and Holdings

for all members as of August 31, 2025.” https://www.imf.org/external/np/fin/tad/extsdr1.aspx.

———.2025e. “Quarterly Report on IMF Finances: For the Quarter Ended July 31, 2025.” https://www.imf.org/-/media/Files/Data/IMF-Finance/Quarterly-Financial-Statements/2025/q1-fy2026-quarterly-report-for-posting-revised.ashx/.

———.2025f. “World Economic Outlook Database.” April. https://www.imf.org/en/Publications/WEO/weo-database/2025/april.

———.2025g. “World Economic Outlook Update.” July. https://www.imf.org/en/Publications/WEO/Issues/2025/07/29/world-economic-outlook-update-july-2025.

———. 2025h. “List of LIC DSAs for PRGT-Eligible Countries.” March. https://www.imf.org/external/Pubs/ft/dsa/DSAlist.pdf.

International Trade Administration (ITA). 2025. “Jobs Supported by US Exports.” https://www.trade.gov/data-visualization/jobs-supported-us-exports.

Kose, M. Ayhan, and Naotaka Sugawara. 2020. “Understanding the depth of the 2020 global recession in 5 charts.” World Bank Blogs, June 15. https://blogs.worldbank.org/en/opendata/understanding-depth-2020-global-recession-5-charts.

Maronoti, Bafundi. 2022. “Revisiting the International Role of the US Dollar.” BIS Quarterly Review, December 5. https://www.bis.org/publ/qtrpdf/r_qt2212x.htm.

Merling, Lara, Ivana Vasić-Lalović, and Lorena Valle Cuéllar. 2024. “The Rising Cost of Debt: An Obstacle to Achieving Climate and Development Goals.” Washington, DC: Center for Economic and Policy Research, April. https://cepr.net/publications/the-rising-cost-of-debt-an-obstacle-to-achieving-climate-and-development-goals/.

Mnuchin, Steven T. 2020. “U.S. Treasury Secretary Steven T. Mnuchin’s Joint IMFC and Development Committee Statement.” US Department of the Treasury, press release, April 16. https://home.treasury.gov/news/press-releases/sm982.

Mottley, Mia. 2021. “WLS – Opening Ceremony, Remarks by Mia Amor Mottley, Prime Minister of Barbados.” United Nations Framework Convention on Climate Change. November 1. https://unfccc.int/sites/default/files/resource/BARBADOS_cop26cmp16cma3_HLS_EN.pdf..

Organisation for Economic Co-operation and Development (OECD). 2024. “Climate Finance Provided and Mobilised by Developed Countries in 2013–2022.” May. https://www.oecd.org/content/dam/oecd/en/publications/reports/2024/05/climate-finance-provided-and-mobilised-by-developed-countries-in-2013-2022_8031029a/19150727-en.pdf.

———. 2025a. “OECD Data Explorer.” https://data-explorer.oecd.org/vis?lc=en&df[ds]=DisseminateFinalDMZ&df[id]=DSD_DAC1%40DF_DAC1&df[ag]=OECD.DCD.FSD&df[vs]=1.0&av=true&pd=%2C&dq=DAC…1140%2B1160..Q.&ly[rw]=MEASURE&ly[cl]=TIME_PERIOD&to[TIME_PERIOD]=false&vw=tb.

———. 2025b. “Cuts in Official Development Assistance: OECD Projections for 2025 and the Near Term.” OECD Policy Brief, June 26. https://www.oecd.org/en/publications/cuts-in-official-development-assistance_8c530629-en/full-report.html.

Ortiz, Isabel, and Matthew Cummins. 2022. “End Austerity: A Global Report on Budget Cuts and Harmful Social Reforms in 2022–25.” Initiative for Policy Dialogue, Global Social Justice, International Confederation of Trade Unions, Public Services International, ActionAid International, Arab Watch Coalition, Bretton Woods Project, Eurodad, Financial Transparency Coalition, Latindadd, Third World Network, and Wemos, September. https://www.eurodad.org/end_austerity_a_global_report.

Riker, David. 2015. “Export-Intensive Industries Pay More on Average: An Update.” Office of Economics Research Note, no. 2015-04A, US International Trade Commission, April. https://www.usitc.gov/publications/332/ec201504a.pdf.

Schoenfeld Walker, Amy, Malika Khurana, and Christine Zhang. 2025. “What remains of U.S.A.I.D.?” The New York Times, June 22. https://www.nytimes.com/interactive/2025/06/22/us/politics/usaid-foreign-aid-trump.html.

Sheremirov, Viacheslav, and Sandra Spirovska. 2022. “Fiscal multipliers in advanced and developing countries: Evidence from military spending.” Journal of Public Economics 208, no. 2022: 104631.

Special Drawing Rights Act, Pub. L. No. 90–349, 82 Stat. 189. 1968. https://www.govinfo.gov/content/pkg/COMPS-1359/pdf/COMPS-1359.pdf.

Sultan, Zafar Ahmad. 2011. “Foreign exchange reserves and India’s import demand: A cointegration and vector error correction analysis.” International Journal of Business and Management 6, no. 7: 69.

United Nations Conference on Trade and Development (UNCTAD). 2025. “A World of Debt 2025: It Is Time for Reform.” June. https://unctad.org/publication/world-of-debt.

United Nations Department of Economic and Social Affairs (UN DESA). 2012. “Global Liquidity for Global Development.” Policy Brief no. 39, October. https://policy.desa.un.org/sites/default/files/inline-images/eapd2023/policybrief39.pdf.

US Bureau of Economic Analysis (BEA). 2025a. “International Trade in Goods and Services.” https://www.bea.gov/data/intl-trade-investment/international-trade-goods-and-services

———. 2025b. “International Transactions, Services, and Investment Position (IIP) Tables.” https://www.bea.gov/itable/international-transactions-services-and-investment-position

Weisbrot, Mark. 2015. Failed: What the “Experts” Got Wrong about the Global Economy. New York: Oxford University Press.

———. 2016. “The IMF’s Lost Influence in the 21st Century and Its Implications.” Washington, DC: Center for Economic and Policy Research, September 15. https://cepr.net/publications/the-imfs-lost-influence-in-the-21st-century-and-its-implications/.

———. 2020. “If you could save a million lives, would you do it?” The Hill, October 1. https://thehill.com/blogs/congress-blog/politics/519243-if-you-could-save-a-million-lives-would-you-do-it/.

Weisbrot, Mark, Rebecca Ray, Jake Johnston, Jose Antonio Cordero, and Juan Antonio Montecino. 2009. “IMF‐Supported Macroeconomic Policies and the World Recession: A Look at Forty‐One Borrowing Countries.” Washington, DC: Center for Economic and Policy Research, October. https://cepr.net/documents/publications/imf-2009-10.pdf.

Weisbrot, Mark, and Lara Merling. 2018. “Argentina’s Deal with the IMF: Will ‘Expansionary Austerity’ Work?” Washington, DC: Center for Economic and Policy Research. December. https://cepr.net/images/stories/reports/argentina-imf-2018-12.pdf.

World Bank. 2025a. “Total reserves (includes gold, current $) – China.” https://data.worldbank.org/indicator/FI.RES.TOTL.CD?locations=CN.

———. 2025b. “World Development Indicators.” https://databank.worldbank.org/source/world-development-indicators/Series/NY.GDP.PCAP.PP.KD.

World Health Organization (WHO). 2020. “Coronavirus Disease 2019 (COVID-19) Situation Report – 67.” https://www.who.int/docs/default-source/coronaviruse/situation-reports/20200327-sitrep-67-covid-19.pdf?sfvrsn=b65f68eb_4.

———. 2024. “Joint child malnutrition estimates.” https://www.who.int/data/gho/data/themes/topics/joint-child-malnutrition-estimates-unicef-who-wb.

———. 2025. “Coronavirus disease (COVID-19) pandemic.” https://www.who.int/europe/emergencies/situations/covid-19.

Yellen, Janet L. 2021. “Letter from Treasury Secretary Janet L. Yellen to G20 Colleagues.” US Department of the Treasury, press release, February 25. https://home.treasury.gov/news/press-releases/jy0034.

Report

Article

Report