January 25, 2013

January 23, 2013, Joint Session of the Labor and Education Committees New Mexico State Legislature

January 23, 2013

Testimony by CEPR Co-Director Dean Baker before a joint session of the New Mexico State Legislature labor and education committees on public pension funds

Thank you for inviting me to discuss the return assumptions used by the state pension plans in assessing their funding situation. I recognize that this is an important issue that has important implications for the future of these plans, the plans’ beneficiaries and the state budget. I will make three points on this issue.

1) The assumption of a 7.75 percent annual return on pension fund assets is a modest assumption. This is very much in keeping with historical experience. More importantly it is consistent with the standard projections for economic growth used by government and private sector economists assessing a wide variety of issues.

2) There is very little downside risk to this projection. The stock market is inherently volatile. This means that returns over a one, two, or three year period are unpredictable and can vary sharply from long-term trends. However it is nearly impossible that returns over the full projection period will fall substantially below the 7.75 percent return assumed by the state’s pension funds.

3) There is a real cost to making return assumptions that are markedly lower than the expected return on the fund’s assets. This will require excessive contributions in the near-term future for the benefit levels being provided. In exchange for lower contributions later. That would be the equivalent of raising taxes today to put money in the bank so that future taxpayers will pay lower taxes.

I discuss each of these points briefly below. However before I directly deal with these issues, I want to clarify my views on pension returns and economic growth more generally. I have not historically been a big optimist about either the stock market or the economy. In fact in the 1990s I wrote several papers warning about the stock bubble, which among things raised the point that many pensions were being overly optimistic on their return assumptions.[1] I argued that market was virtually certain to fall sharply from its bubble peaks, and that any funds that were assuming that equities would provide their historic rate of returns, given the price to earnings ratios of the late 1990s, were likely to face serious troubles.

Similarly in the last decade I was warning of the housing bubble and the likelihood that its collapse would lead a recession as early as 2002.[2] I also warned that pension funds were still being overly optimistic in their return assumptions, given that price to earnings ratios in the market continued to be well above their historic average.[3] In short, I have never approached this issue as a blind optimist. I have often been far more pessimistic about the economy than the consensus within my profession. And, I have been quite happy to be critical of pension funds for making dangerously optimistic assumptions on returns. So the argument I am making today is not from a reflexive habit of protecting pension funds but rather based on a consistent analysis that I am applying across different circumstances.

The Basis for a 7.75 Percent Return Assumption

The main issue in any projection of returns on pension assets is the appropriate assumption for returns on equities, which would include both money directly invested in equities and money that is indirectly invested in corporate stock through venture or private equity funds. Typically, these categories together account for roughly 70 percent of a pension fund’s assets.[4]

Historically, the nominal rate of return on equities has averaged over 10 percent (7 percent real). There is considerable short-term fluctuation with the market often producing small or even negative returns for a period of time; however there is considerably less variation over longer periods. Periods of low returns are generally offset by periods of higher than normal returns. The assumption of a 10 percent nominal return is especially safe given that the market has fallen sharply from its extraordinary peaks in 90s bubbles. With price to trend earnings ratios back to their historic averages, it is difficult to envision a scenario in which stocks will produce a return that is much below 10 percent.

Before going through the calculations that provide the basis for this assertion it is worth briefly commenting on the notion of using a risk-adjusted rate of return assumption. The argument for using such an assumption is that the return on stocks is inherently risky; therefore we should reduce the projected return for pension funds in recognition of this risk.

The notion of risk associated with stock returns depends on the relevant time-frame. For individual workers it is entirely appropriate to attach a substantial risk premium to stock returns since it can be a very big deal if the market is down at the moment when it is necessary to cash out their holdings. If a worker retires or dies unexpectedly when the stock market is depressed then the worker or their family will have to get by on a much lower income in future years. By contrast, New Mexico’s pension funds should be able to get through a bear market by relying on short-term assets like money market funds to meet the bulk of their obligations. It should not be necessary to sell off large amounts of equity at a loss. For this reason, the possibility that the market can be depressed for a number of years has little consequence for the pension fund, as long as it has made a correct assumption on long-term averages.

Returning to the basis for projecting future stock returns, the key number is simply the ratio of stock prices to earnings. In principle it is best to take trend earnings, but for simplicity we can just take the ratio of the value of corporate stock at the end of the third quarter to third quarter earnings. This ratio was 13.0, meaning that a dollar in corporate stock produced after-tax earnings of approximately 7.7 cents.[5] Historically more than 60 percent of corporate earnings have been paid out as either dividends or returned to shareholders as share buybacks, which would be expected to raise share prices by reducing the number of shares outstanding. Assuming that 60 percent of corporate profits are paid back to shareholders through one of these channels, the yield would be 4.6 percent annually.[6]

The other component of returns is the rise in the share price. The simplest assumption is that share prices rise in step with corporate profits, which in turn are assumed to rise in step with the rate of growth of the economy. The logic here is that over long periods of time there are not huge changes in the profit share of national income, which means that in general corporate profits will rise in step with income.[7] The CBO and most other analysts project that long-term GDP and income growth will average close to 2.4 percent. If inflation averages 2.5 percent, then this translates into capital gains that will average 4.9 percent annually.

Summing the 4.6 percent dividend yield and the 4.9 percent return gives a 9.5 percent nominal return or 7.0 percent real return. If 70 percent of New Mexico’s pensions are invested in stock directly or indirectly then this implies that this portion of the funds’ assets will provide a return of 6.75 percent on the total value of the fund. If the remaining 30 percent of the funds’ assets have a yield averaging 3.3 percent, then the fund will have the 7.75 percent return assumed in its projections.

Since most of the concern about return projections lies with the stock return assumptions, it is worth showing more carefully the robustness of this assumption. First, in terms of the dividend return, if anything the assumption in this calculation is on the low side. The combination of dividend yields and share buybacks has often exceeded 60 percent, so the assumption of a 60 percent ratio is likely to be lower than is actually the case, especially since growth is projected to be somewhat slower going forward than it has been in the past.

I will consider the appropriateness of the GDP growth projection in the next section, but the assumption that the price to earnings ratio will remain constant over a long period is in fact a conservative one. Of course if the price to earnings ratio were to rise, then the return on money current invested in equities would obviously exceed the 9.5 percent figure calculated above. However, the assumption that the price to earnings ratio can fall enough to produce a substantially lower return can easily be shown to be implausible.

Suppose that the economy grows by 2.4 percent and the inflation rate is 2.5 percent as assumed above. Then assume that the stock prices only grow 3.9 percent a year, rather than the 4.9 percent assumed above. This would lower the return on the money currently held in equities to 8.5 percent from the 9.5 percent calculated above.

However, if our assumptions about GDP and profit growth do not change, then when the price to earnings ratio falls, the dividend yield by definition rises. In the case where the nominal growth rate is 4.9 percent (2.4 percent real and 2.5 percent inflation) and stock prices grow at just a 3.9 percent rate, then the price to earnings ratio will have fallen to just 11.8 to 1 after 10 years. (Stock prices will have risen by 46.6 percent, while earnings will have risen by 61.3 percent.)

With a price to earnings ratio of 11.8 to 1, each dollar invested in stock is getting 8.5 cents in after-tax earnings. If corporations are paying out 60 percent of their earnings in dividends or share buybacks, then this component of the return alone is 5.1 percent annually. Even if stock prices continued to rise at just a 3.9 percent nominal rate the return would still be 9.0 percent annually, just 0.5 percent below the return calculated earlier.

Of course if stock prices continued to grow less rapidly than corporate earnings, then the price to earnings ratio would rise further. If this pattern continued for 20 years, then the price to earnings ratio would have fallen to 10.7 to 1, which would mean that a dollar invested in corporate stock would generate 9.3 cents in after-tax earnings. If 60 percent of this money was paid out in dividends, then the dividend yield would then be 5.6 percent. In this case, even if the stock price just grew at 3.9 percent annually the total yield would be equal to 9.5 percent calculated above. Furthermore, since the stock price would still be growing less rapidly than earnings, the price to earnings ratio would continue to rise. This would mean that the yield would rise above the 9.5 percent assumed in the initial calculation. This means that over a 30-year period, there would be little difference on average between the returns in this scenario and the 9.5 percent return in the initial calculation.

There is no way around this simple logic. If the rate of price growth trailed by earning by 2.0 percentage points, then after a decade the price to earnings ratio would be 10.7, which means that a dollar in stock would generate 9.3 cents in earnings. If 60 percent of these earnings are paid out in dividends then the dividend yield would be 5.6 percent, which would make the total yield 8.5 percent. If the stock price continued to trail earnings growth by 2 percentage points then the price to earnings ratio would be fall to 8.6 after twenty years meaning that each dollar invested in stock was producing 11.3 cents in earnings. If 60 percent of this money was paid out in dividends then the return on dividends would be 6.8 percent of the share price. Adding this to the 2.9 percent capital gains would give a total return of 9.7 percent, slightly higher than the 9.5 percent rate calculated above.

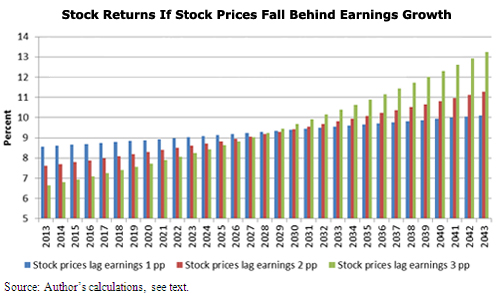

The first two situations are illustrated in Figure 1 below, along with a more extreme scenario in which stock prices trail the growth of the economy by 3 percentage points annually. In all three cases, the implied drop in the price to earnings ratio has the effect of raising the dividend yield. This means that the returns will eventually rise above the 9.5 percent assumed in the original set of calculations.

In short, if the assumptions of earnings growth are close to accurate, then it is virtually impossible to construct a scenario in which returns on stock average substantially less than the 9.5 percent assumed in the initial calculation. If stock prices rise by less than the growth in earnings then it means that the dividend yield in the future will be higher. This puts a floor on how low returns can be on money invested now and implies that money invested in the future will almost certainly get a higher return, if the price to earnings ratio falls as a result of stock prices falling.

Figure 1

The Risk of a Prolonged Slump

The economy has recently seen its worse downturn since the Great Depression and is still far from recovering the lost ground. This has led many people to fear that we could have a slump lasting several decades like Japan, which may lead to substantially lower stock returns than we have seen historically.

While extreme events can never be ruled out, it is important to understand that this sort of prolonged slump be a very extreme event. Not only has the United States never experienced a multi-decade long downturn of this nature, even Japan has not experienced the sort of slump that is often attributed to it.

One of the main factors behind Japan’s slowing growth has been its slowing population and labor force growth. This was the result of demographic factors that preceded the downturn. Japan has long had very slow population growth. While there is an interaction between the economy and population growth (through immigration and birth rates), there is no reason to believe that the United States would see the same sort of falloff in population growth. In fact, U.S. population is still growing at a rate of approximately 0.9 percent annually.

Per capita GDP growth in Japan from 1990 to 2012 averaged 0.8 percent. If we add that to the U.S. population growth of 0.9 percent, this would come to 1.7 percent annual GDP growth in the United States. This means that even if the U.S. plunged into a prolonged Japanese type slump, and we substituted the 1.7 percent growth number for 2.4 percent figure assumed above, then stock returns would only fall by 0.7 percentage points below the levels calculated above.

Furthermore, the calculation of per capita GDP growth in Japan is very sensitive to the year chosen as the start point. Japan’s economy had been booming in the late 1980s, if the year 1988 is chosen as a start point instead of 1990 then per capita growth over the next 24 years would have averaged 1.1 percent. This would translate into 2.0 percent GDP growth given the United States population growth. That would translate into a 9.1 percent annual rate of return, just 0.4 percentage points below the level assumed in the calculations above.

This means that even in the extreme case where the United States enters into a prolonged slump comparable to that Japan has experienced in the last quarter century, a 9.5 percent return assumption for stocks is not likely to be far from the mark. There are of course good reasons for believing the U.S. economy will not experience a comparable slump. Productivity growth has continued to hold up reasonably well in the downturn, with the high tech sector continuing to lead the world in developing innovative products. And of course we have the benefit of learning from the mistakes of Japan and other countries to design better policy.

While it is possible that growth in the long-run will prove to be somewhat slower than the current consensus, it is extremely unlikely to be enough slower so as to make much difference in pension returns over the next three decades. Even if per capita growth in the United States fell to the rates seen in Japan it would not hugely affect the returns on New Mexico’s pensions over this period.

The Cost of Underestimating Returns

Often the discussion of pension accounting is conducted as though it is always desirable to error on the side of overfunding, as though there is no cost to being wrong on the high side. This is not true. In principle we would like to maintain a relatively even flow of funding for pensions, with the payments being roughly in accord with when workers accrue their benefits.

If we adopt an overly conservative funding standard then we will not be maintaining an even stream. For example, if we assume a 5.5 percent rate of return on pension assets and they do in fact provide the 7.75 percent return derived in the discussion above, then the pension would soon become fully funded, at which point it would be possible to sharply reduce contribution levels.[8] This would mean that we would effectively be overfunding the system at present, thereby allowing lower payments in the future.

There is no obvious virtue or sensible principle of public policy that is advanced by going this route. Having an excessive funding level in the present and near future effectively means that we are paying much of our future pension expense in advance of when it is actually being incurred. This would make no more sense than prefunding school systems or fire departments. We could opt to do this sort of prefunding by putting aside money in special accounts for these purposes. This would allow people in 10 or 20 years to tax themselves less to support public services because the money was already available from the prefunding.

No state or municipal government has gone this route of prefunding public services and for good reason. While it might be nice to pay lower taxes in the future, it comes at the cost of higher taxes in the present and/or reduced public services. There is no obvious reason that we would want to go this route. While taxes are necessary, they do impose distortions on the economy reducing output. And those distortions rise more than proportionately to the increase in the tax rate. In other words, a tax rate of 10 percent will lead to considerably more than twice the economic losses of a tax rate of 5 percent. If we overfund our pensions by having tax rates than would otherwise be necessary in the present, then we will be causing unnecessary losses of economic output.

Alternatively, if we cut back public services to cover the cost of overfunding we are either ignoring current needs, for example providing health care services for the poor and elderly, or neglecting investment in the future, for example in infrastructure and education. In the former case, if there are real needs that we would otherwise meet, it seems a poor excuse to neglect these needs in order to overfund public pensions. In the case of public investment, we will be making our children and grandchildren worse off if we defer necessary expenditures in order to overfund the pension. Overfunded public pensions will provide little consolation to a generation of children that does not receive an adequate education in school or lives in a state with an antiquated infrastructure.

In short, there is a good reason to ensure that pensions are properly funded. This means not allowing large shortfalls to develop. However there is also good reason not to deliberately overfund pensions. The cost in terms of higher than necessary levels of taxation or inadequate levels of public service and investment is likely to far exceed any future benefit in the form of lower tax rates. In effect the decision to deliberately overfund pensions amounts to imposing the costs on society today that we are worried we could have to impose on society in the future, if events turn out badly. That is not good policy.

Conclusion

New Mexico’s pension systems are being completely responsible in assuming a 7.75 percent rate of return on their assets. This is consistent with past performance and also consistent with current ratios of stock prices to corporate earnings and projections of economic growth. This assumed return will not be hugely affected by even sharp and sustained departures of stock prices from their historic trend or by an economy that is substantially weaker than consensus projections. While it is always necessary to use caution in any set of projections, the harm from being overly pessimistic is real and substantial. Given the relative risks, New Mexico’s pension funds are using good judgment in their assumptions on the returns of the assets in their funds.

[1] See Baker, Dean 2000. “The Implications of the Over-Valuation of the Stock Market and the Dollar,” Center for Economic and Policy Research, Washington, DC: Center for Economic and Policy Research, available at https://www.cepr.net/index.php/publications/reports/double-bubble-the-implications-of-the-over-valuation-of-the-stock-market-and-the-dollar/; Baker, Dean 1999. “Bull Market Keynesianism,” The American Prospect, January, 1999, available at http://prospect.org/article/bull-market-keynesianism.

[2] Baker, Dean, 2002. “The Run-up in House Prices: Is It Real or Is It Another Bubble?” Center for Economic and Policy Research, Washington, DC: Center for Economic and Policy Research, available at https://www.cepr.net/index.php?option=com_content&view=article&id=405.

[3] Weller, Christian and Dean Baker, 2005. “Smoothing the Wave of Pension Funding: Could Changes in Funding Rules Help Avoid Cyclical Underfunding,” Journal of Policy Reform, V8 #2: 131-151.

[4] New Mexico’s main public employee pension fund is invested heavily in international equities and venture capital. It would require a careful examination of the specific investments to judge whether these investments are likely to offer better returns than U.S. equities. However if the fund’s managers have used good judgment in opting for these investments rather than domestic equities, it is reasonable to assume that their expected return will be at least as high as the return on the U.S. stock market.

[5] The market value of domestic corporations at the end of the third quarter was $19,698.1 billion (Federal Reserve Board, Flow of Funds, 2012:Q3, Table 213, Line 23). After-tax corporate profits were $1515.2 billion (U.S. Department of Commerce, National Income and Product Accounts, Table 1.12, Line 15).

[6] In a period of slow growth the percentage of profits paid out to shareholders would be expected to rise, since there are few good investment opportunities.

[7] It is likely that the profit share of GDP is near a cyclical high, which means that it is likely to decline in the decade ahead. However, the GDP growth assumption used in this calculation is somewhat lower than most forecasters would use since the economy is still well below its potential GDP, which means that it will have a substantial period in which its growth rate is likely to exceed its long-term average.

[8] Rosnick David, and Dean Baker, 2012. “Pension Liabilities: Fear Tactics and Serious Policy,” Center for Economic and Policy Research, Washington, DC: Center for Economic and Policy Research, available at https://www.cepr.net/index.php?option=com_content&id=6667&view=article.