June 18, 2018

Every year, the Social Security and Medicare trustees’ report, released earlier this month, provokes a range of responses. This year’s report was no exception, even though it was very similar to last year’s report. For Social Security, an essential program that provides retirement and other benefits to millions each year, the report predicted that it would only be able to pay 79 percent of benefits starting in 2034. This is because of a predicted shortfall in funding, which can be explained by a combination of factors, none of which imply the program is poorly run, no longer important, or fundamentally unsustainable.

While some are clear-headed about the issues facing the programs and understand its relative affordability, others provide misleading and often exaggerated narratives that rely on poorly thought-out indicators (for example, changes in worker-to-retiree ratios).

As with last year, buried deep within this year’s 270-page report are the trustees’ own facts about the program’s future. Relying on this data and based on the trustees’ logic, it is clear that Social Security is not in dire straits. Let’s walk through it.

What the Social Security trustees think

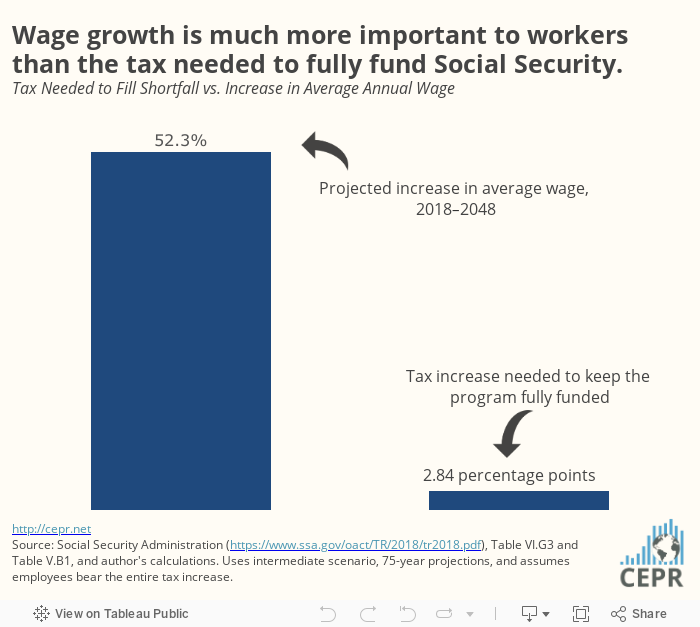

The trustees’ predict that in their intermediate scenario over a 75-year timeframe, Social Security’s trust fund, which collects and disperses money related to the program, will have a shortfall of 2.84 percent of payroll (Table VI.G3). In other words, payroll taxes will need to be increased by 2.84 percentage points overall to eliminate the shortfall entirely.[1] Assuming that this amount falls entirely on employees (rather than shared equally with employers, as is the case now) and that it applies equally across different salaries, workers would see a decrease in their after-tax income. Although this is not an insignificant amount especially for people with lower incomes, it’s not exactly a disaster either.

But the trustees also predict that wages will increase. In their “Principal Economic Assumptions” (Table V.B1), they predict that the average wages will increase by 52.3 percent over the next forty years (in real terms, taking into account inflation).

The figure below compares these two numbers. Wage growth is much more important to workers than the tax needed to fund Social Security over a 75-year horizon.

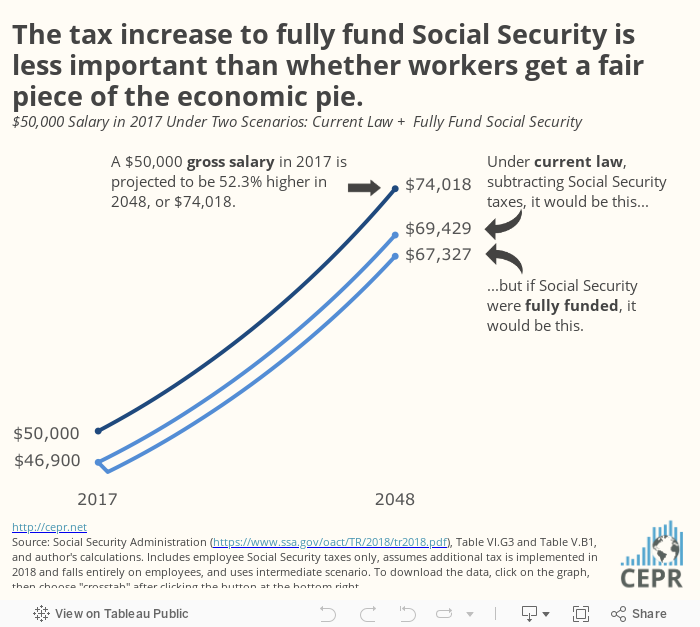

The next figure projects these changes over the next 40 years using a salary of $50,000. A gross salary is projected to grow to $74,018 in this time period. Under current law, it would be $69,429 after Social Security taxes. If Social Security were fully funded, it would be $67,327.

The difference between the salaries due to the additional Social Security tax is again, not insignificant. But by the trustees’ own numbers and logic, assuring that workers, especially at the middle and bottom of the wage ladder, see their wages grow is enormously more important than a 2.84 percentage point tax. This tax seems like a small price to pay for a secure retirement.

It’s unlikely that trustees’ projections will hold over such a long time frame, yet politicians should take note: focusing on growing the wages of workers should be a top priority, not cutting Social Security benefits.

There are even more reasons why “fixing” the program is easy

Running through the trustees’ logic on Social Security’s financial status makes a pretty convincing case that it is not imminently in need of cuts or “reforms” that could jeopardize the well-being of seniors and others who rely on the program. (Social Security keeps tens of millions out of poverty.)

It’s important to note that this analysis assumed that the entire additional 2.84 percentage point Social Security tax would be borne by workers. In reality, the tax that funds Social Security is equally split between workers and employers. A common economic assumption is that increases to employer payroll taxes come out of the pay from workers, so “splitting” the tax could be effectively the same as if workers paid the entire tax. That’s not to say that there couldn’t be other kinds of taxes that fund the program, only that those taxes wouldn’t be in line with how the current system is set up.

Another qualification to add is that the trustees use a 75-year horizon to evaluate the program’s finances. There is nothing natural about this time frame — a lot could change in 75 years! The program should be flexible enough to make changes to keep benefits at current levels or even raise them. (There is little evidence retirees rely less on Social Security than in the past, so it’s a bit perplexing that some think that routine changes to the program should result in cuts.)

Indeed, a lot has changed over the last 75 years. One example relates to Social Security’s payroll tax cap, which rises with inflation. The cap means that only the first $128,400 of wages are subject to the tax in 2018. But due to rising inequality, more and more wages are above the cap, meaning Social Security has less of a base to draw on. 10 percent of wages were above the cap in 1983. In 2016, over 17 percent of wages were above the cap. It makes sense that the tax cap should be eliminated or at least re-worked to capture some of these wages. Doing so would result in the elimination of a significant portion of the shortfall.

Post-deficit politics

There’s also a question of whether the government needs to increase taxes now to pay for Social Security at all. Social Security’s trust fund has an inherent logic behind it: people pay into the program during their working life, and it distributes money to people when they qualify (usually at retirement). Yet, while the trust fund has insulated the program from political attacks to cut benefits, the logic behind it has also prevented politicians from tweaking its financing to cope with, for example, the increasing amount of wages above the payroll tax cap.

Simply put, if politicians want to increase or maintain Social Security benefits, they can simply put money into the trust fund, similar to how they could give everyone a pony. To give everyone a pony, the government would need to breed enough ponies; to put money into Social Security, the government would need prioritize a growing economy that produces enough output for that money to maintain its value. While this decision to directly fund the trust fund would have to be balanced with the risks of opening up the program to attacks, there are clearly enough resources in the United States to fully fund Social Security and even expand the program without directly raising taxes to cover the cost. This is not to say that taxes in general will never need to be changed in the future, only that debt itself and specifically, the fact that Social Security will have a shortfall, are the wrong indicators to use to determine if Social Security is affordable or not.

It has been encouraging that over the last few years there has been a transformational shift within the Democratic Party regarding Social Security. While many Democrats once supported cuts to the program, there is now a consensus to expand the program. This is because expanding the program is increasingly more important as it becomes a larger share of retirees’ incomes, in part due to the decline of pensions.

It’s also because, whether or not politicians or policymakers subscribe to all the ideas outlined here or not, there are clear and relatively easy pathways forward to fully fund and expand the program. The difficulty of actually solving these problems is more about politics, and less about specific numbers or reports.

[1] This amount also would leave the trust fund with a reserve equal to one year’s cost, as opposed to the “necessary tax rate” of 2.78 percent, which would leave the trust fund empty at the end of the period (but which also assumes some shift of wages to evade the tax).