Article

The Federal Reserve Board will submit its semiannual report to the House and Senate next week. The report, and testimony from Chair Janet Yellen, will no doubt discuss whether to raise the federal funds interest rate, the interest rate that banks use when lending to each other. Raising interest rates before the labor market fully recovers from the 2007–2009 recession will slow economic growth, worsen the budget deficit, and weaken the labor market, causing unemployment and a decline in worker bargaining power.

While some measures show that the labor market is far from a complete recovery, the official unemployment rate has made up about 90 percent of its losses since the end of the recession in June 2009. There are good reasons to think that the unemployment rate is overstating the degree to which the economy has recovered, however.

One way to show that overstatement is to look at what is happening to the components that make up the unemployment rate, which is calculated by taking the number of people categorized as “unemployed” divided by those counted in what the Bureau of Labor Statistics calls the “civilian labor force.” It is instructive to look at these components for “prime-age” workers: workers that are ages 25 to 54. These workers are usually old enough to be working and too young to be retired. By looking at measures that track the percentage of prime-age workers over time we can avoid demographic effects that may influence broader measures.

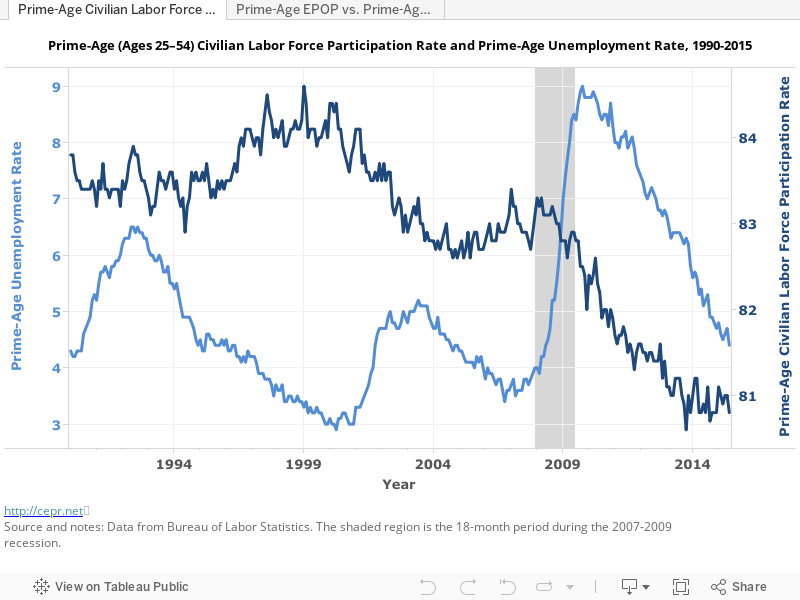

The graph below shows prime-age civilian labor force participation rate on the right axis in dark blue and the prime-age unemployment rate on the left axis in light blue. The civilian labor force participation rate tells us the percentage of workers that are in the labor force, either counted as employed or unemployed.

The results are striking: what we see is that the civilian labor force participation rate began to fall during the 2007–2009 recession (the shaded area) and has continued falling throughout the recovery, losing over two percentage points in total. It stood at 83.1 percent at in December 2007, reached its nadir in October 2013 at 80.6 percent, and as of June 2015, is at 80.8 percent. This suggests that much of the improvement that we have seen in the prime-age unemployment is due to a declining prime-age civilian labor force. When workers are so disheartened with their employment prospects and no longer look for a job, they are no longer counted as unemployed, and thus the civilian labor force participation rate declines, as does the unemployment rate.

This means that among those most likely to be in the labor force, many stopped looking for work and exited the labor force during the recession and the recovery. Another way to conceptualize that is: if the prime-age civilian labor force rate were to recover to its peak just as the recession began (83.3 percent), we would need almost 3.2 million more prime-age workers in the labor force. And if we counted those 3.2 million people as unemployed, the prime-age unemployment rate would be 7.3 percent and would have recovered to pre-recession levels by only 34 percent since its peak in October 2009.

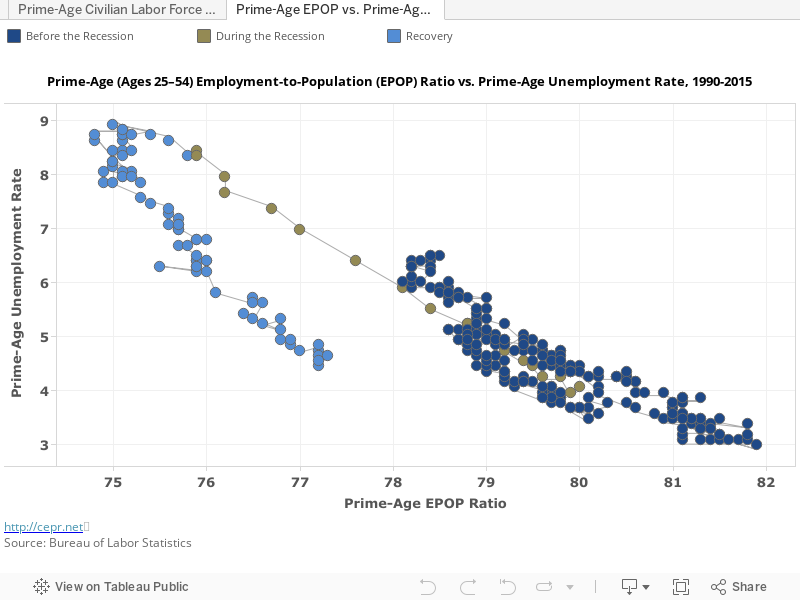

The employment-to-population (EPOP) ratio, or the percentage of the total population that is employed, is another way we can gauge the recovery of prime-age workers. A new issue brief found that the prime-age EPOP was less than halfway recovered, still down 2.5 percentage points from the beginning of the recession in December 2007.

By mapping the prime-age EPOP ratio to the unemployment rate for the same workers, we can see how the current unemployment rate and EPOP ratio, at 4.4 percent and 77.2 percent respectively, compare to the same values before the recession.

We can see that post-recession data (light blue) are associated with a much lower EPOP ratio than a decade ago or more ago (dark blue). Again, the recovery of the prime-age unemployment rate overstates the recovery of prime-age workers overall, as we have seen through the civilian labor force participation rate and now the EPOP ratio. This suggests that there is still a substantial amount of slack in the labor market.

FedWatch is a semi-monthly online publication of the Center for Economic and Policy Research (CEPR) providing analysis by Dean Baker and colleagues of issues related to the pending Federal Reserve decision on interest rates.