Article

The Absence of Universal Social Protections in the United States Harms Black Men

Article

In a recent post, researchers at the Brookings Institute noted that “[o]n many social and economic measures, Black men fare worse not only than white men, but white and Black women.” They argue that what is needed is “a battery of specifically tailored policy interventions: a New Deal for Black Men, no less,” and explain the “elements of this New Deal will likely consist of intentional policymaking in the fields of education and training, the labor market, family policy (especially for fathers), criminal justice reform, and tackling concentrated poverty.”

“Specifically tailored” policies in these areas are essential, but they are not enough. Black men in the United States are disadvantaged by the piecemeal and fragmented design of the American social state. The absence of universal social protections in the United States is due in part to policymaking based on stereotypical assumptions about Black men and Black women. Without the kind of comprehensive, inclusive social protections that exist in many other wealthy nations, any New Deal for Black Men will be inadequate to meet the challenges Black men face. In this article, we illustrate this with a specific programmatic example showing how the insufficiently universal nature of the US health care system disproportionately excludes non-elderly Black men from coverage, particularly during early adulthood.

The United States spends more per capita on health care than any other country, yet we lack the kind of universal health coverage that is standard in other wealthy nations. Instead, we have a fragmented system that spends about $200 billion a year to publicly subsidize the provision of employer-based coverage in a regressive fashion, while relying on various means-tested individual benefits and subsidies to cover the non-elderly who don’t have employer-based coverage. This fragmented system means that millions of Americans go without any health insurance, have experienced gaps in coverage if they currently have insurance, or have inadequate coverage that leaves them facing high out-of-pocket costs and deductibles.

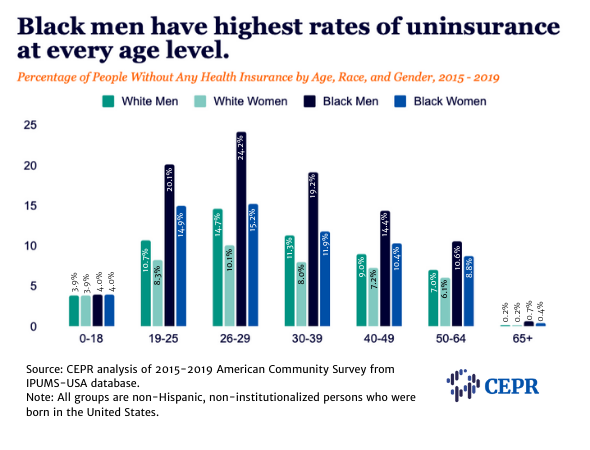

Black working-age men are among those most disadvantaged by our peculiarly inequitable health care system. This is illustrated in the Figure 1 below comparing health insurance coverage by age among the non-elderly in four race-gender groups: Black Men, White Men, Black Women, and White Women.

As children and seniors, all four race-gender groups have similar uninsurance rates (roughly 4 percent for ages 0–18 and under 1 percent for ages 65 and over). In effect, coverage for the elderly is very close to universal in the United States, and coverage for children is near universal as a result of policy decisions. In the case of the elderly, these policies include the creation of Medicaid and Medicare. For children, it includes the establishment of Medicaid as well as successful efforts over the last several decades to expand children’s eligibility for public health coverage. As a consequence, even though employer-based coverage of children has declined substantially over the last several decades, expanded public coverage has not only filled in the gap but increased the share of all children with coverage over time and reduced racial disparities in coverage.

Unfortunately, the same policy decisions have not been made for non-elderly adults, and uninsurance rates jump sharply after age 18, particularly for Black men. In young adulthood (ages 19–25), uninsurance rates more than quadruple when compared to uninsurance rates for ages 0–18. By comparison, uninsurance roughly triples for Black women in this age range and doubles for white men and white women.

Uninsurance continues to increase for most groups in their late twenties (ages 26–29), partly because young adults cannot remain on their parents’ employer-based coverage once they turn 26. But, again, Black men stand out as having a particularly high uninsurance rate, with nearly one-in-four Black men ages 26–29 uninsured. While the rates of uninsurance decrease later in life, Black men remain the most likely to be without health coverage between the ages of 50 to 64.

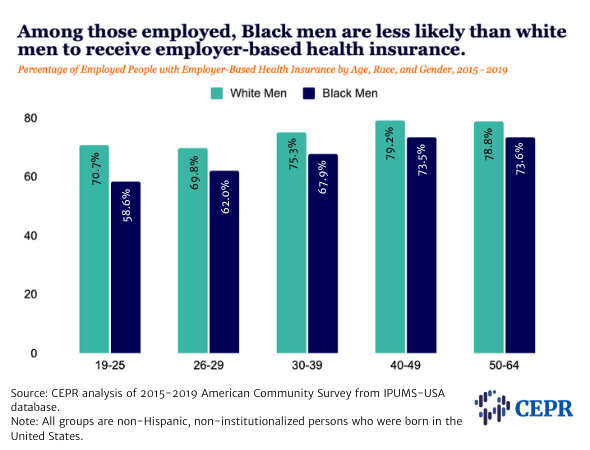

The disparities in coverage for non-elderly adults are partly due to disparities in access to employer-based coverage, which is publicly subsidized through the tax system and remains the most common source of coverage for the non-elderly in the United States. As economist Jason Furman has noted, the tax subsidies for employer-based coverage are “ineffective and regressive, wasting money on those who have health insurance while doing little for those who can barely afford it and nothing at all for those without it.”

As the Figure 2 below shows, among non-elderly adults, employed Black men are less likely to have employer-based coverage than employed white men. Although not shown in the table, there are almost certainly additional disparities in the quality of employer-based coverage among workers (and their family members) who have it, with poorly compensated employees, who are more likely to be Black than white, getting poorer coverage. Moreover, as other research has documented, “benefit inequality” between employed white men and employed Black men has widened over time.

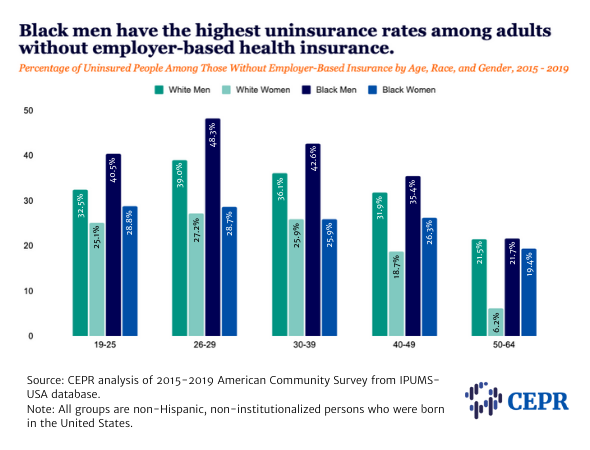

A system that provided universal health coverage would ensure, at the very minimum, that people excluded from employer-based insurance have public or otherwise affordable coverage. This is clearly not the case in the United States, except for children and the elderly. Moreover, as the Figure 3 shows, Black men who don’t have employer-based coverage are much less likely to have coverage from other sources than the other three groups.

The most important means-tested health insurance benefits are Medicaid and the premium tax credit for insurance purchased through the Affordable Care Act (ACA) marketplaces. Under Medicaid, states must provide free coverage to certain “categorically eligible” groups with very low incomes (including children, the elderly, and some people with disabilities). States also have the option to expand Medicaid to cover adults with incomes under 138 percent of the federal poverty line who are not elderly or disabled (under the ACA this coverage was mandatory, but the Supreme Court struck down this requirement, making it optional for states).

As a result of the ACA, the United States has moved further in the direction of universal coverage. Uninsurance rates for adults 19–49 have declined by about one-third since 2008. Racial disparities in coverage have generally narrowed, although not as much as disparities by income. Yet, our health care system remains fragmented and, as already shown in Figure 1, considerable disparities remain. Young adults (19–25) have seen the largest declines in uninsurance since the passage of the ACA, with their likelihood of being uninsured falling by about half since 2008. But young Black men remain nearly twice as likely as young white men in this age range to be uninsured.

There are also considerable disparities in coverage among non-elderly Black men depending on where they live. Currently, 39 states (including the District of Columbia) have adopted the Medicaid expansion, while 12 states, nearly all in the South and Midwest, have not. For Black men ages 19–49, uninsurance rates are nearly twice as high in states that haven’t expanded Medicaid than in states that have. Moreover, as the Kaiser Family Foundation has documented, non-elderly uninsured Black adults are more likely than any other racial or ethnic group to fall into the coverage gap that exists in states without expanded Medicaid, meaning they have low-incomes but do not qualify for Medicaid or premium assistance if they purchase ACA Marketplace coverage.

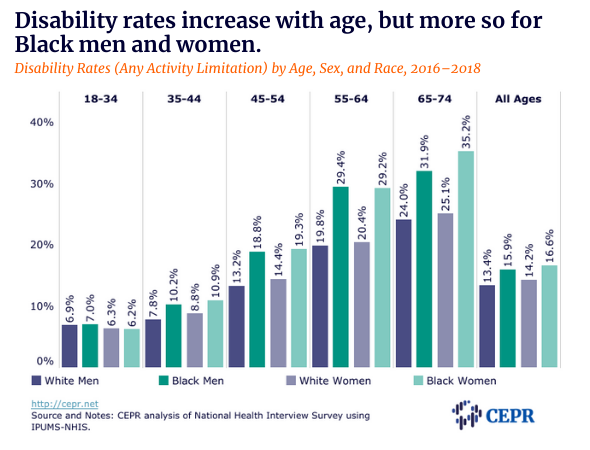

The absence of universal health coverage in the United States and the resulting racial disparities in coverage help explain why Black people are less likely to have access to a regular source of health care than white people. These factors almost certainly contribute to Black men’s lower life expectancy and other disparities highlighted in the Brookings post. They also contribute to the racial disparity in disability, which increases with age. As Figure 4 shows, in their twenties and early thirties, Black men and Black women have roughly the same disability rates as white men and white women, respectively. Disability rates increase with age for all four groups. However, the increases are much larger for Black men and women than for white men and women. Nearly 30 percent of Black people ages 55 to 64 have one or more disabilities compared to about 20 percent of white people in the same age range.

The absence of universal health coverage also contributes to other structural inequalities in the US health care system. One recent example is the distribution of CARES Act Provider Relief funds to hospitals and other health care providers using a formula that is largely driven by “total net patient revenue from all sources.” This favors hospitals with higher shares of insured patients, especially ones with private insurance. Researchers have found that the formula results in “allocations largely unrelated to health or financial needs” and means “disproportionately Black communities received the same level of relief funding as counties with less health and financial need.”

Beyond the absence of universal health coverage, the inadequate and fragmentary nature of various other forms of social insurance and social assistance in the United States further contributes to these disparities. The United States has a relatively stingy unemployment insurance system, is the only wealthy nation without paid sick leave, and sharply rations rental housing assistance. Means-tested money assistance is largely limited to the elderly (Supplemental Security Income, referred to as SSI), people with severe work-related disabilities (SSI), people caring for minor children (Temporary Assistance for Needy Families, or TANF), and employed people (the Earned Income Tax Credit, called EITC). The Supplemental Nutrition Assistance Program (SNAP), sometimes called food stamps, provides an in-kind income floor, but has very stringent work tests for non-elderly, non-disabled people not caring for minor children. The EITC is much more generous for workers with dependents than for workers without them.

The heavy reliance on means-testing, categorical limits on eligibility, punitive work tests, waitlisting, and other “ordeal mechanisms” block many of those who would benefit most from social protections, but give up on obtaining them. As Victor Ray, Pamela Herd and Don Moynihan discuss in a new working paper, these kinds of “burdens have historically been used to normalize and facilitate racially disparate outcomes from public organizations that promise fair and equal treatment.” Table 1 below, is adopted from their paper and provides examples.

|

Tenets of Racialized Organizations Theory |

Examples of Administrative Burdens as Racialized Weapons |

|---|---|

|

Tenet 1: Burdens diminish agency of racially marginalized groups. |

Example: Means-tested programs consume more time and effort to establish eligibility and maintain benefits, which disproportionately impact Black people. |

|

Tenet 2: Burdens legitimate unequal distribution of resources. |

Example: “Deservingness” and fraud tropes legitimate making it more difficult for marginalized racial groups to access social benefits. |

|

Tenet 3: Whiteness is a credential that eases burdens. |

Example: Whiteness secures access to less burdensome benefits, even without work credentials, e.g., white women with Social Security survivors benefit. Whiteness also confers social resources that advantages white people within bureaucracies. |

|

Tenet 4: Decoupling of formal rules from organizational practice in ways that racialize burdens. |

Example: Bureaucratic discretion employed in ways that systematically advantage white beneficiaries and disadvantage Black beneficiaries in terms of access to social welfare benefits. |

Source: Adopted from Table 4 in Ray, Herd, and Moynihan, Racialized Burderns: Applying Racialized Organization Theory to the Administrative State, December 8, 2008.

Many of these kinds of burdens are present in Medicaid, including means tests and other eligibility requirements that, as Ray, Herd, and Moynihan note, “disproportionately shift administrative burdens towards beneficiaries and away from organizations.” Some 19 states have even sought approval from the Trump administration to impose punitive work-hours tests on working-age beneficiaries. Such tests would harm both the unemployed and poorly compensated workers in occupations with volatile hours. Many employed Medicaid beneficiaries subject to the test would lose eligibility for paperwork and reporting reasons, not because they actually failed the test.

Most Americans would benefit from a more comprehensive and universal system of social protection than currently exists in the United States. But Black men would be among the most well served by the same kind of comprehensive, inclusive social protections that exist in most other wealthy nations.

Methodology

Health insurance coverage rates were calculated using 2015–2019 American Community Survey (ACS) data from the IPUMS-USA database. For the age groups, 18-year-olds are included in the same group as those between the ages of 0–17 because Medicaid and State Children’s Health Insurance (SCHIP) for children generally extends through age 18. To focus on Black-white racial disparities, the sample was restricted to US-born citizens who did not report an Hispanic origin. In addition, people living in institutional group quarters (including correctional facilities) were not included. Correctional facilities have a legal duty to provide adequate coverage to prisoners, and prisoners generally cannot use Medicaid or the ACA Marketplace coverage to pay for health care while incarcerated. Including non-elderly men (19–64) living in institutional group quarters in the sample would increase the Black-white disparity in health insurance by about 2.6 percentage points; among non-elderly men ages 19–49, the disparity would increase by 2.9 percentage points.