Article

The IMF’s Effective Lending Rate for Large Borrowers Is Now at Over 8 Percent

Article

The International Monetary Fund (IMF) is considered a “super-senior” creditor for developing countries, but it is now charging over 8 percent for disbursements to its most indebted borrowers. Super-senior credits are loans that have priority payback, above all other loans.

Domestic pundits in developing countries usually claim that governments should prefer borrowing from multilateral lenders like the IMF because it’s cheaper than taking on debt elsewhere. While they usually ignore the social and economic costs of conditionality, they are also ignoring the true financial costs of IMF lending.

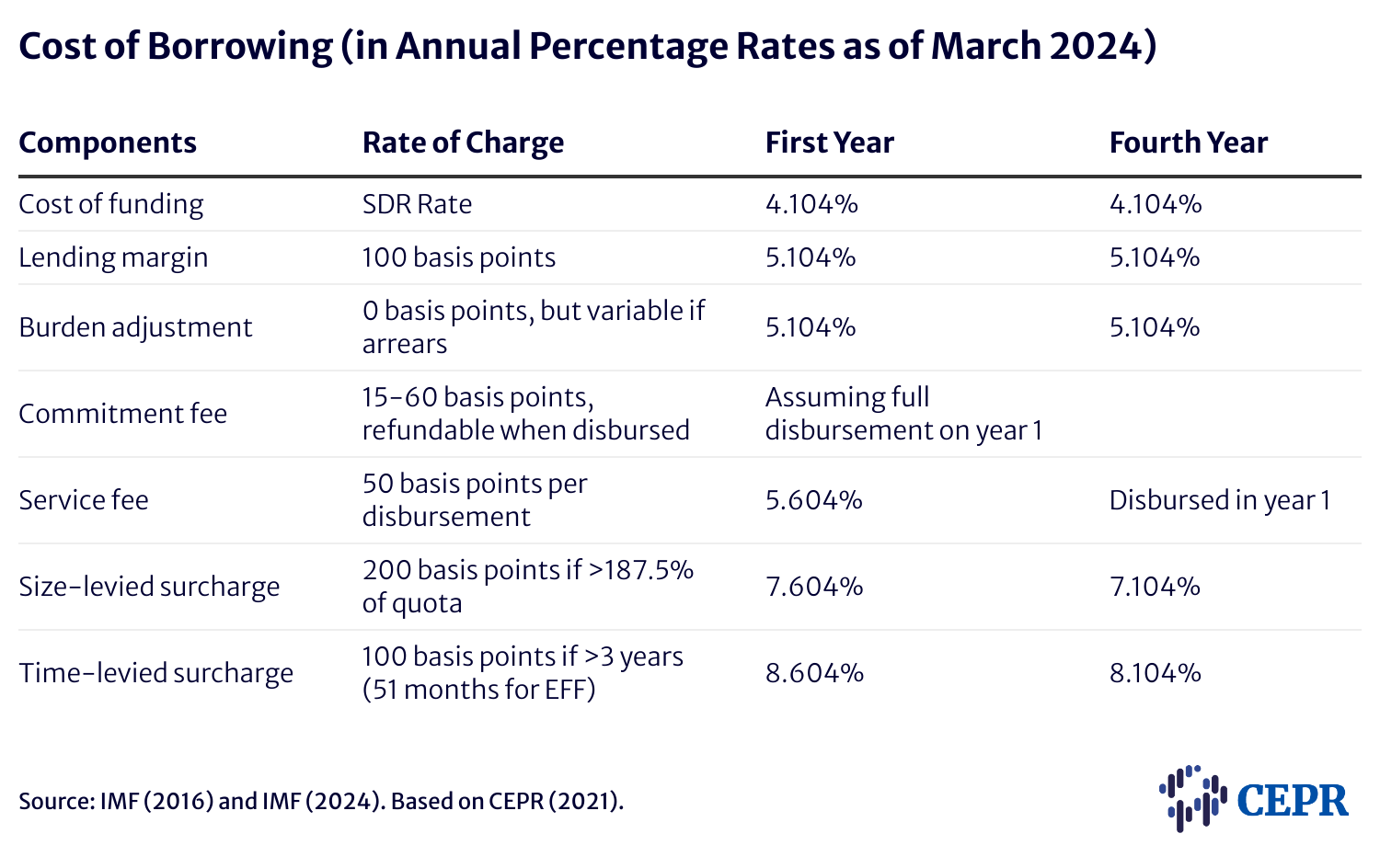

IMF surcharges are not, relatively, well-known, and they add on to IMF lending rates. The official lending rate is the base rate (a weighted average of the money market rates of five currencies) plus 100 basis points (lending margin). But there are other fees and (until recently, completely opaque) surcharges that are not published in staff reports’ “Indicators of Fund Credit” — a table included in reports that projects countries’ cost of borrowing from the IMF.

CEPR has published several articles and reports on IMF surcharges and their economic consequences. US legislators who are discussing ways of curtailing junk fees paid by consumers in the United States have also advanced legislation to get the US Treasury to lead efforts to suspend surcharges at the IMF.

The IMF charges an extra 200 basis points if a country’s debt to the IMF is above a certain threshold, and an extra 100 basis points if the debt was taken at least four years ago and has not been paid back early (even if the country sticks to the original amortization table, which usually lasts 10 years).

In our 2021 report on surcharges, we included Table 2 that shows what the true cost of borrowing is for developing countries. An updated version of this table is presented below:

Now, with rising interest rates, the base rate has gone up from 0.05 percent to 4.104 percent today. This means that the effective cost of new borrowing for these already indebted countries is now above 8 percent, which is very high for many developing countries compared to when they sought IMF financing only a few years ago.

The IMF managing director has said that rising interest rates should be taken into account when discussing surcharges. The World Bank has also raised alarms regarding the problem of variable interest rates.

Some might argue that the IMF cannot forego these additional charges because it must also remunerate higher rates on its liabilities. This is true, but the IMF has an investment portfolio of liquid assets that has generated gross investment income that has vastly exceeded these remuneration expenditures. It appears to be perfectly safe for the IMF to forego surcharges in this high interest rate environment.

It has been claimed that scrapping surcharges would negatively affect the IMF’s balance sheet. However, the IMF’s target for its precautionary balances has already been met.

In order to mitigate the likelihood of recurring indebtedness due to the added budgetary and balance of payments pressure of surcharges, the Executive Board of the IMF should suspend surcharges immediately.

Article

Article

Report

Report