October 13, 2022

The author thanks Andrés Arauz, Dan Beeton, Kevin Cashman, Brett Heinz, Jake Johnston, Alex Main, and Mark Weisbrot for helpful comments, suggestions, and editorial work.

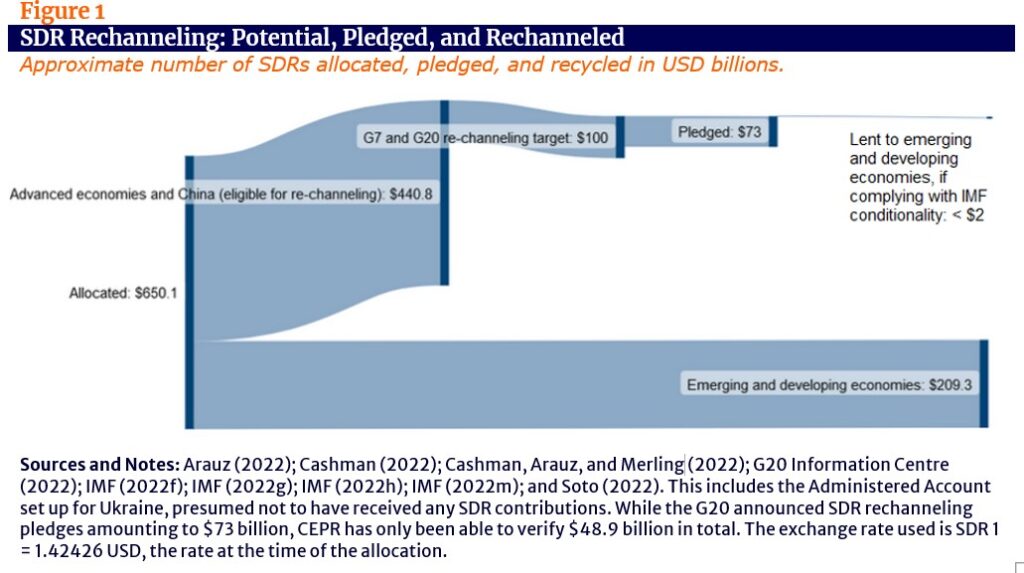

In response to the COVID-19 pandemic, the International Monetary Fund (IMF) issued $650 billion in Special Drawing Rights (SDRs) to its member states in August 2021.1 The IMF issues SDRs at no cost and without conditions attached, and member countries do not have to pay them back; as such, they do not create new debt.2 In previous reports, we analyzed the widespread benefits derived from the allocation in providing much-needed balance of payments and fiscal support. Among other things, countries used SDRs to purchase vaccines and other essential imports, and to boost domestic spending.3

Global economic conditions, however, have continued to deteriorate, contributing to convergent food, energy, and health crises. Many countries are still struggling to recover from the economic fallout of COVID-19 and are now facing additional external shocks. In response to the continued need for additional assistance, the IMF has proposed to “rechannel” SDRs via conditional lending programs for low- and middle-income countries through the Poverty Reduction and Growth Trust (PRGT) and the newly established Resilience and Sustainability Trust (RST). Advanced economies4 and China have pledged approximately $73 billion in SDRs for rechanneling.5 No high-income countries currently plan to donate their SDRs to low- and middle-income countries directly and unconditionally, even though this could serve as a simpler option than rechanneling, and would preserve the special qualities of SDRs.

In this paper, we will demonstrate that by turning a reserve asset that adds nothing to a country’s debt, and that has no conditions attached to it, into a loan with conditions attached, the main proposals for rechanneling SDRs have altered the nature of this unique instrument in fundamental ways with a potential net negative impact on countries that receive this form of assistance. We conclude that a new allocation of SDRs remains the most effective option available to provide critical assistance to all low- and middle-income countries.

Rechanneling through the PRGT and RST, in particular, has several limitations:

A new allocation of $650 billion would provide a much greater amount of funding than rechanneling, and would do so without conditionality or access limits, and without adding any debt to developing countries’ balance sheets, 19 of which are already facing debt stress or crises.8 It would also allow for much faster delivery of assistance. It is worth noting that very little rechanneling has been accomplished, despite a year having passed since the IMF governors approved the allocation; the SDRs, however, were distributed just three weeks after governor approval.9 An analysis of SDR usage following the August 2022 issuance demonstrates that countries could immediately use a new allocation of SDRs for debt relief, to import life-saving necessities, and to support key public services.10 In many cases, SDRs provide important financial support without being converted to hard currency: the additional international reserves that SDRs provide to countries help reduce capital flight11 and potentially devastating balance of payments and fiscal crises. These additional reserves can also lower countries’ borrowing costs.

In response to the COVID-19 pandemic, the International Monetary Fund (IMF) issued $650 billion in Special Drawing Rights (SDRs) to its member states in August 2021.12 SDRs are the IMF’s unit of account and an international reserve asset that can be held, exchanged for hard currency, and used to pay off IMF debt. The value of SDRs is based on a basket of five currencies: the US dollar, the euro, the British pound sterling, the renminbi, and the yen.13 In previous reports, we have analyzed the unique characteristics of SDRs and the widespread benefits derived from last year’s issuance.14 The 2021 SDR allocation provided much-needed balance of payments and fiscal support in the context of the COVID-19 pandemic, with a number of countries using their SDRs to purchase vaccines and other necessary imports, and to boost domestic spending.15 Though this allocation provided much-needed financial relief globally, low- and middle-income countries are in serious need of additional assistance in order to better respond to the world’s current crises.

In the past year, economic conditions have continued to deteriorate around the globe. According to the World Food Programme, 345 million people currently face acute food insecurity — a number that has more than doubled since 2019.16 In its July World Economic Outlook Update, the IMF projected another downgrade to global growth for 2022, in the context of the increased risk of global recession, the war in Ukraine, and concurrent health, food, and energy crises.17 The spillover effects from the war in Ukraine and Western sanctions against Russia, among other factors, include increased energy prices and disruption to markets for food.18

Energy prices, and also food prices, have contributed to an increase in inflation in the United States, to which the US Federal Reserve has responded with increased interest rates.19 Seventy-five central banks throughout the world have followed the Fed’s lead by also raising interest rates, in most cases by multiples of the Fed’s increases.20 These interest rate hikes are making it much more difficult for emerging and developing economies to manage debt. They can result in defaults and currency, fiscal, and balance of payments crises, akin to those that followed the Volcker “shock” caused by an aggressive increase in the Federal Reserve’s interest rates in the early 1980s. That shock ultimately resulted in debt crises and a “lost decade” in Latin America and most of the developing world.21 These rising interest rates have compounded the economic effects of the pandemic and continue to endanger human welfare around the world. Urgent financial assistance, particularly a new allocation of SDRs, is imperative to help ensure an equitable and effective global recovery.

In an attempt to counter the economic effects of the pandemic, subsequent external shocks, and “long-standing structural problems,” the IMF has proposed to “rechannel” SDRs to low- and middle-income countries through two trusts, given that two-thirds of the 2021 SDR allocation went to advanced economies, most of which do not need SDRs, and almost none of which will be able to actively use them.22 In this brief, we will review existing rechanneling proposals and compare their potential impact with that of a fresh issuance of SDRs. We will demonstrate that by turning a reserve asset, which costs governments nothing, into debt with conditions attached, the IMF’s proposals for rechanneling fall drastically short of delivering critical financial support around the globe. In addition, rechanneling faces legal, logistical, and political hurdles that have so far severely prevented its deployment. While rechanneling proposals via multilateral development banks (MDBs) offer better alternatives,23 a new allocation remains by far the most viable and effective option available to assist low- and middle-income countries.

SDRs have a number of unique qualities that make them a very effective policy instrument. This is true in the case of a direct allocation, where there are, most importantly, no significant downside risks. The IMF SDR Department issues SDRs at no cost and without conditions attached, and member countries do not have to pay them back; as such, they do not create new debt.24 An allocation can serve as a relatively quick way to spread liquidity around the globe. As a reserve asset, SDRs play a key role in addressing balance of payments constraints, expanding fiscal space, and heading off current threats and the spread of various additional crises. An increase in a country’s reserves can decrease exchange rate risk, improve borrowing terms, and allow governments to better respond to external shocks like the current convergent food, climate, and health crises. An addition of SDRs to a country’s reserves also allows it to free up foreign currency for spending, instead of having to purchase more.

When the IMF Board of Governors approved an allocation of $650 billion in SDRs in August 2021, countries received the funds within three weeks.25 An analysis of the use of the issuance found that many low- and middle-income countries used SDRs to acquire hard currency and procure vaccines, to support budgets, and to pay off both IMF and non-IMF debt.26 This included significant amounts of IMF debt, ultimately having a vastly greater impact on reducing developing country debt levels than other initiatives, such as the Debt Service Suspension Initiative (DSSI) and the Catastrophe Containment and Relief Trust (CCRT).27 It is worth noting here that SDRs can be used directly to pay off IMF debt, without conversion to hard currency. The DSSI postponed debt payments from 48 of the 73 poorest countries that requested it, but the debt was not canceled,28 while approximately $12.9 billion in debt payments was suspended under the DSSI for 2020–2021.29 The CCRT, which provides grants, issued just under $1 billion in debt relief across 31 countries in 2021.30 In comparison, countries used SDRs from the 2021 allocation to pay off $7.6 billion of IMF debt and potentially avoided incurring $81 billion of new debt thanks to fiscal use of SDRs.31

Approximately two-thirds of an SDR allocation goes to high-income countries and China, as SDRs are distributed according to the IMF’s quota system.32 High-income countries and China have almost never used their SDRs in any proactive way, but rather hold them as reserve assets. This is in accordance with the IMF Articles of Agreement, according to which countries that want to convert their SDRs into one of the IMF’s usable currencies must show need (typically a balance of payments need) in order to do so.33 In response to the ongoing COVID-19 pandemic and the continued global need for balance of payments and fiscal stability, the G7 and the IMF, as well as civil society organizations, proposed that high-income countries reallocate, or “rechannel” some of their new SDRs to low- and middle-income states. Rechanneling can theoretically take a number of forms, including direct bilateral donations, onlending to IMF entities or other prescribed holders (such as regional banks), establishing administered accounts (such as the one created for Ukraine in the wake of the 2022 Russian invasion), or funding new non-IMF mechanisms.34

Since 2021, the IMF has made the case for rechanneling allocated SDRs from wealthy countries by lending through the newly established Resilience and Sustainability Trust (RST), and the previously existent Poverty Reduction and Growth Trust (PRGT). Essentially, these SDRs would be used to fund trusts that issue loans to low- and middle-income countries. By turning a costless reserve asset into conditional debt, however, the IMF’s proposals for rechanneling fail to capitalize on SDRs’ unique qualities, and instead merely use these resources to expand the Fund’s traditional lending mechanisms. The inadequacy of the IMF’s proposal for rechanneling is also clear when compared to the benefits of a new allocation and to other rechanneling proposals. Lending terms for the RST and PRGT, while concessional, are still subject to conditionality — including IMF-backed structural policy reforms — and require an existing Upper Credit Tranche program with the IMF. The RST’s stringent access limits currently exclude approximately 70 percent of emerging and developing economies, including some facing very high climate risks.35

Aside from focusing on the RST and the PRGT, the Fund is also providing technical assistance to MDBs interested in exploring rechanneling options.36 After the 2021 SDR allocation, the G7 and G20 proposed rechanneling $100 billion in SDRs,37 while the IMF called for advanced economies to pledge $45 billion in SDRs for the RST, $16.5 billion for the PRGT in hard currency or SDRs, and $3 billion for subsidy resources.38 In July 2022, the G20 announced that approximately $73 billion in SDRs had been pledged in total, and the IMF Communications Department noted that about $39 billion had been pledged to the RST, specifically.39 CEPR has only been able to verify pledges up to $49.8 billion, however.40 Initially, the United Kingdom, Japan, Korea, Spain, Australia, and the Netherlands pledged to donate a portion of their SDR allocation to the PRGT; China and France each made a general pledge to African countries; and Italy and Canada each made a general pledge to vulnerable and low-income countries.41

In the United States, the largest SDR holder, there was a proposal to contribute $21 billion to the PRGT and RST, but this was not approved by Congress (the legislation mentioned dollar amounts and did not mention the rechanneling of SDRs).42

The PRGT was created to provide concessional financing to low-income countries, and is funded through bilateral loan agreements and an encashment regime with both hard currency and SDRs.43 Bilateral agreements are made between the IMF and lending countries, with lending countries agreeing to transfer SDRs or currency to the trust on demand for onlending to low- and middle-income countries.44 Encashment means that the PRGT holds a portion of SDRs as reserves and uses a portion to issue loans. This is similar to how a typical commercial bank keeps a reserve ratio of deposits that can be withdrawn. In this way, high-income countries can keep these SDR contributions as liquid assets on their balance sheets, with a guarantee that they can retrieve them from the PRGT. The RST is similarly structured.

After a country makes a pledge to rechannel SDRs, it often must approve the transfer through domestic legislative or budgetary procedures, in addition to creating an agreement with the IMF before the SDRs can be transferred.45 As Plant and Sala note, the lack of centrally available information has rendered tracking SDR flows in the context of rechanneling a difficult and opaque process.46 As of July 2022, the only country to have approved a transfer of SDRs to the RST was Spain, in the amount of $1.87 billion.47 And one year after the $650 billion in SDRs allocation was approved, approximately $1.5 billion has been lent from the RST to Barbados, Costa Rica, and Rwanda, with a few other countries, like Bangladesh, showing interest in borrowing.48 Bangladesh has requested $4.5 billion from the IMF generally, including a portion from the RST (the RST’s ceiling for lending per country is 150 percent of quota, or SDR 1 billion, whichever is smaller).49

Borrowing from the RST is conditional, and Costa Rica may be required to implement additional policy reforms on top of its current Upper Credit Tranche (UCT) program under the Extended Fund Facility (EFF).50 Barbados and Rwanda will start new UCT programs, which will enable them to borrow from the RST.51 Bangladesh will have to begin a new UCT program to meet eligibility requirements.

The recently launched RST was created to fill the financing gap for low- and middle-income countries that face climate risks, and to address balance of payments stability.52 Rechanneling SDRs through the RST would mean funding the trust with wealthy countries’ SDRs, which would be used to issue new, conditional loans to low- and middle-income countries. Most low- and middle-income countries, however, do not qualify to borrow from the trust; the RST does not seem to have been designed to fulfill its purported mission to help countries address pandemic and climate risks.

As noted above, one of the most concerning aspects of the RST is its stringent access limit that currently excludes about 70 percent of emerging and developing economies, including many with high poverty rates and climate vulnerability. Eligibility criteria include a current IMF program and an income limit.53 According to a study published by the Task Force on Climate, Development, and the International Monetary Fund, approximately 143 out of 153 emerging and developing economies, as defined by the IMF, will be theoretically eligible according to income requirements.54 But out of those 143, only 38 had an existing financing program with the IMF as of September 2022, and a few countries have nonfinancial IMF programs, such as the Policy Coordination Instrument. This means that approximately 70 percent of low- and middle-income countries, which should qualify under the RST’s income requirement, are in fact excluded.55 Those left out include low-income economies with high poverty rates that are at risk of climate-induced shocks, such as Ghana, Nigeria, Côte d’Ivoire, and Malawi, among others.56 The income-based access limit and higher interest rates could also create a barrier for heavily indebted middle-income countries, which could otherwise use a direct allocation for debt relief.57 It is important to remember that more than 67 percent of the world’s population living in poverty is in middle-income countries.58

The RST’s lending terms specify a 20-year maturity and a 10-and-a-half-year grace period. Interest rates will be applied through a tiered system, at a rate higher than the current SDR rate59 (55-95 basis points above the SDR rate, depending on country classification by income), with higher concessionality for low-income countries.60 Zero percent rates for low-income countries will therefore not be guaranteed through the RST.61

Conditions for borrowers include “(i) a package of high-quality policy measures consistent with the purpose of the Trust; (ii) a concurrent financing or non-financing program with ‘upper credit tranche’ (UCT) quality policies; and (iii) sustainable debt and adequate capacity to repay the Fund.”62 Based on what has frequently been observed regarding the conditions applied to PRGT loans, there is a high probability that countries can expect potentially harmful and/or procyclical fiscal consolidation and monetary policy tightening when borrowing from the RST. Fiscal consolidation and other austerity measures, as prescribed by the IMF, have often been linked to increased poverty and inequality in countries where they have been implemented.63 Ortiz and Cummins’s global study of the “deadly policy” of austerity found that a decade of cuts to, and underfunding of, public health systems increased health inequalities and vulnerability to COVID-19 around the world.64

Organizations including the European Network on Debt and Development (Eurodad) and the Task Force on Climate, Development, and the International Monetary Fund, among others, have criticized the limitations of the RST.65 They have argued that the RST could be improved by embracing broader eligibility criteria to include all climate-vulnerable countries, regardless of income level, and including those without an existing IMF program. Mariotti has warned against harmful conditionality and has called for more concessional financing that would not undermine governments’ debt sustainability, as well as a contingent clause in RST loans to protect recipient countries against external shocks.66 In addition, hundreds of anti-poverty and development-focused organizations signed an open letter warning against exclusionary and conditional rechanneling mechanisms.67 However, at present there are no indications that the IMF — or the most important voice there, the US Treasury Department — is considering the changes advocated by these organizations.

The PRGT is the IMF’s main vehicle for concessional lending to low-income countries.68 It consists of three credit facilities: the Extended Credit Facility (ECF), the Standby Credit Facility (SCF), and the Rapid Credit Facility (RCF). Again, rechanneling through the PRGT would mean funding the trust with wealthy countries’ SDRs, which would be used to issue new, conditional loans to low-income countries.

The three credit facilities issue loans based on short-, medium-, and long-term balance of payments needs. Under the ECF and SCF, borrowing countries agree to implement a set of structural reforms. Borrowing through the facilities is currently interest-free until July 2023, and the PRGT aims to increase subsidy resources to maintain a zero percent interest rate until 2024.69 The interest on PRGT loans, however, is variable; if the interest rate were to increase, it would be applied to all outstanding loans.70 The IMF is currently trying to raise approximately $16.5 billion (SDR 12.6 billion) for the PRGT in hard currency or SDRs, as well as $3 billion for subsidy resources.71

Similar to the RST, one of the main constraints of the PRGT is limited accessibility. Only 69 countries are qualified to borrow from its facilities.72 Eligibility is limited to 145 percent of a country’s IMF quota share per year, and total outstanding concessional credit to 435 percent of quota.

According to a review of IMF lending agreements published by Oxfam International earlier this year, the vast majority of IMF loans to low- and middle-income countries between March 2020 and March 2022, including some issued through the PRGT, require fiscal consolidation or other austerity measures.73 Conditions in recent IMF loans include regressive tax measures, such as the application of Value Added Taxes (VAT) to food staples, and the phasing out of electricity and fuel subsidies, among other measures. Kenya, under the Extended Fund Facility (EFF) and the PRGT’s ECF, was required to increase taxes on food and cooking gas, even though three million Kenyans face acute hunger.74

Capacity poses another potential issue with rechanneling SDRs through the RST or PRGT. Mariotti and Plant noted that the trusts could not absorb the full $100 billion worth of SDRs committed by the G7 and G20, as the RST and PRGT can currently only support $30 and $50 billion, respectively.75 This means that additional rechanneling would have to take other forms in order to utilize the full amount committed.

While the IMF focuses on using SDRs to issue new debt to low- and middle-income countries, several civil society organizations, heads of state, and the African Development Bank (AfDB) have proposed alternate options for rechanneling that avoid harmful conditionalities and access limits. Proposals include rechanneling through MDBs and creating new prescribed holders of SDRs for rechanneling outside of the IMF.

The AfDB has called for $100 billion in SDRs to channel through the African Development Fund (ADF), which provides concessional financing for programs contributing to social and economic development and poverty reduction.76 France, Japan, the UK, Saudi Arabia, and Canada have expressed interest in the proposal.77 There are several benefits to rechanneling through the AfDB or other multilateral development banks, including their existing prescribed holder status and alignment with development and climate goals.78 The AfDB proposes using SDRs for food security, African integration and industrialization, and other important development goals. Crucially, it would not require macroeconomic conditionality as part of its programming.79 However, both Cristine Lagarde, president of the European Central Bank, and Kristalina Georgieva, managing director of the IMF, have argued that European Union countries (27 of the 39 advanced economies) cannot rechannel their SDRs to the AfDB or to other multilateral development banks, even to those — like the AfDB — that are registered holders of SDRs.80

Administered accounts, such as the one launched for Ukraine this year to help meet its balance of payment needs and stabilize its war-ravaged economy, are another rechanneling option. Countries are able to deposit both hard currency and SDRs into the account. While Canada initially pledged CAD $1 billion to the administered account for Ukraine, it is unclear if any contributions have been made in SDRs.81 Plant and Sala noted that SDRs could serve an important purpose in boosting Ukraine’s reserves for balance of payment needs, but that it would not make as much sense for European countries, in particular, to transfer SDRs if Ukraine plans to exchange them for European currencies anyway.82 Additionally, the legislative processes for transferring SDRs could take significant time, and would vary considerably between countries.83 Another proposal by the UN Economic Commission for Africa (UNECA) aims to use SDRs to partially fund a recently launched repurchase market for African debt, the Liquidity and Sustainability Facility (LSF).84 The initiative aims to lower borrowing costs for African governments, and to spur the issuance of “green bonds or sustainability-linked bonds.”85 This is a potentially impactful proposal that could improve debt sustainability.

Government officials and civil society organizations have also proposed using SDRs for long-term climate finance. Barbados’s prime minister, Mia Mottley, called for a $500 billion annual allocation of SDRs to finance climate mitigation policy and a new climate trust that could attract additional investment for sustainability projects.86 Mariotti suggested that the IMF create new prescribed holders, like new and existing climate funds, emphasizing that they should remain unconditional and debt-free.87 The United Nations Conference on Trade and Development (UNCTAD) has also proposed creating “SDR-based global funds for purposes that command a high degree of collective and multilateral support,” specifically, issuing “Special Environmental Drawing Rights,” with which countries would develop plans to meet climate targets with specific budgetary commitments.88

Bilateral donations are another option for transferring SDRs from high- to low- and middle-income countries that could prove more effective than the IMF’s rechanneling proposals, and could allow for maintaining the unique qualities of SDRs. It is unclear why wealthy countries are not pursuing this option, though legislative constraints may pose an obstacle for some to donate SDRs directly.89 Taking countries’ legislative processes into account, another allocation of SDRs proves to be a simpler option.90 Shortly after the last allocation was approved, African leaders called for a new one, citing the continued challenges of the COVID-19 pandemic and the uneven global recovery.91 African governments renewed this appeal in May 2022 following additional shocks linked to the war in Ukraine.92

The consensus among many anti-poverty and development organizations is that a new allocation of SDRs would provide the most rapid and comprehensive relief to low- and middle-income countries facing concurrent global crises, a continuing global economic downturn, and potential national economic crises and sovereign debt defaults.93 Because almost no advanced economies or China have actively used SDRs, the large portion of a new allocation that would go to these countries would not represent any waste or use of resources by them, but would merely be an accounting entry at the IMF. With another $650 billion in SDRs, emerging and developing economies would receive approximately $209 billion, versus whatever portion of the $73 billion pledged for rechanneling via loans from the IMF that might actually materialize. Countries could immediately use a new allocation of SDRs for debt relief, to import necessities, to support key public services, and to increase their reserves. With another allocation, many lives could be saved, likely in the millions.

In comparison with the far-reaching impact of another allocation, little can be expected from the proposals for rechanneling currently under consideration at the IMF and the US Treasury Department. Any positive impact of whatever rechanneling may occur under the existing proposals could easily be negated by the resulting burden of increased debt, as well as by harmful conditions attached to the loans. And for the foreseeable future, it does not look like much rechanneling is going to take place. Indeed, one year since the allocation was approved, only relatively small amounts of SDRs have been rechanneled.

African Development Bank (AfDB). n.d. “About the ADF.” Accessed August 4, 2022. https://www.afdb.org/en/about-us/corporate-information/african-development-fund-adf/about-the-adf

African Development Bank (AfDB). 2022. “Special Drawing Rights and Reallocation for Low Income Countries – The African Development Bank and IMF Special Drawing Rights.” April 15. https://www.afdb.org/en/documents/special-drawing-rights-and-reallocation-low-income-countries-african-development-bank-and-imf-special-drawing-rights

Andrews, David. 2021. “Can Special Drawing Rights Be Recycled to Where They Are Needed at No Budgetary Cost?” Washington, DC: Center for Global Development, April 20. https://www.cgdev.org/publication/can-special-drawing-rights-be-recycled-where-they-are-needed-no-budgetary-cost

Arauz, Andrés. 2022. “New IMF Trust Shows the Path Toward SDR Rechanneling Through Development Banks.” Washington, DC: Center for Economic and Policy Research, April 30. https://cepr.net/new-imf-trust-shows-the-path-toward-sdr-rechanneling-through-development-banks/

Cashman, Kevin. 2022. “List of Commitments from Advanced Economies and China to Rechannel SDRs, By Country.” Datawrapper, August. https://www.datawrapper.de/_/SH6fR/

Cashman, Kevin, Andrés Arauz, and Lara Merling. 2022. “Special Drawing Rights: The Right Tool to Use to Respond to the Pandemic and Other Challenges.” Washington, DC: Center for Economic and Policy Research, April 20. https://cepr.net/report/special-drawing-rights-the-right-tool-to-use/

Do Rosario, Jorgelina and David Lawder. 2022. “Exclusive: IMF Says Bangladesh Seeks Loan under Fund’s Resilience Trust.” Reuters, July 26. https://www.reuters.com/markets/rates-bonds/exclusive-imf-says-bangladesh-seeks-loan-under-funds-resilience-trust-2022-07-26/

Ellsworth, Brian. 2021. “Barbados’ Mottley Says IMF Must Help Finance the Fight Against Climate Change.” Reuters, December 3. https://www.reuters.com/markets/us/barbados-mottley-says-imf-must-help-finance-fight-against-climate-change-2021-12-03/

European Network on Debt and Development (Eurodad). 2022. “Open Letter to G20 Finance Ministers, Central Bank Governors and the IMF: Civil Society Organizations Call for Issuance of More SDRs and Fairer Distribution.” April. https://www.eurodad.org/more_fairer_sdr_distribution

G20 Information Centre. 2022. “G20 Chair’s Summary: Third G20 Finance Ministers and Central Bank Governors Meeting, Bali, 15-16 July 2022.” University of Toronto Library and the G20 Research Group at the University of Toronto, July 16. http://www.g20.utoronto.ca/2022/220716-finance.html

Georgieva, Kristalina. 2022. “Stepping Up With and For Africa”: Remarks by IMF Managing Director Kristalina Georgieva at the EU-AU Summit Roundtable on Financing for Sustainable and Inclusive Growth in Africa. Washington, DC: International Monetary Fund, February 18. https://www.imf.org/en/News/Articles/2022/02/18/sp021822-stepping-up-with-and-for-africa

Georgieva, Kristalina and Ceyla Pazarbasioglu. 2021. “The G20 Common Framework for Debt Treatments Must Be Stepped Up.” IMFBlog, December 2. https://blogs.imf.org/2021/12/02/the-g20-common-framework-for-debt-treatments-must-be-stepped-up/

Group of Seven (G7). 2021. “Our Shared Agenda for Global Action to Build Back Better.” Carbis Bay G7 Summit Communiqué. Council of the EU and the European Council. June 13. https://www.consilium.europa.eu/media/50361/carbis-bay-g7-summit-communique.pdf

International Monetary Fund (IMF). (2010). “Articles of Agreement of the International Monetary Fund.” December 15. https://www.imf.org/external/pubs/ft/aa/index.htm

______. 2018. “IMF Executive Board Approves US$290 million Extended Arrangement Under the Extended Fund Facility for Barbados.” Press Release No 18/370. October 1. https://www.imf.org/en/News/Articles/2018/10/01/pr181370-imf-exec-board-approves-us-290-million-ext-arr-under-ext-fund-facility-barbados

______. 2021a. “2021 General SDR Allocation: Special Drawing Rights.” August 23. https://www.imf.org/en/Topics/special-drawing-right/2021-SDR-Allocation

______. 2021b.”At a Glance: The IMF’s Firepower.” April 29. https://www.imf.org/en/About/infographics/imf-firepower-lending

______. 2021c. “Fund Concessional Financial Support For Low-Income Countries—Responding To The Pandemic.” Policy Paper No. 2021/053. July 22. https://www.imf.org/en/Publications/Policy-Papers/Issues/2021/07/22/Fund-Concessional-Financial-Support-For-Low-Income-Countries-Responding-To-The-Pandemic-462520

______. 2021d. “IMF Executive Board Approves a 36-month US$ 1.778 Billion Extended Arrangement under the Extended Fund Facility for Costa Rica and Concludes 2021 Article IV Consultation.” Press Release No. 21/53. March 1. https://www.imf.org/en/News/Articles/2021/03/01/pr2153-costa-rica-imf-exec-board-approves-36-mo-ext-arr-eff-concludes-2021-art-iv-consultation

______. 2021e. “IMF Executive Board Extends Debt Service Relief for 25 Eligible Low-Income Countries.” Press Release No. 21390. December 20. https://www.imf.org/en/News/Articles/2021/12/20/pr21390-imf-executive-board-extends-debt-service-relief-for-25-eligible-low-income-countries

______. 2021f. “IMF Managing Director Announces the US$650 billion SDR Allocation Comes into Effect.” Press Release No. 21/248. August 23. https://www.imf.org/en/News/Articles/2021/08/23/pr21248-imf-managing-director-announces-the-us-650-billion-sdr-allocation-comes-into-effect

______. 2022a. “2022 Review of Adequacy of Poverty Reduction and Growth Trust Finances.” Policy Paper No. 2022/016. April 21. https://www.imf.org/en/Publications/Policy-Papers/Issues/2022/04/21/2022-Review-of-Adequacy-of-Poverty-Reduction-and-Growth-Trust-Finances-517091

______. 2022b. “Active IMF Lending Commitments as of September 30, 2022.” https://www.imf.org/external/np/fin/tad/extarr11.aspx?memberKey1=ZZZZ&date1key=2025-12-31

______. 2022c. “Bangladesh: Financial Position in the Fund as of September 30, 2022.” https://www.imf.org/external/np/fin/tad/exfin2.aspx?memberKey1=55&date1key=2099-12-31

______.2022d. “World Economic Outlook: Database—WEO Groups and Aggregates Information” April. https://www.imf.org/external/pubs/ft/weo/2022/01/weodata/groups.htm

______. 2022e. “IMF Executive Board Approves the Establishment of a Multi-Donor Administered Account for Ukraine.” Press Release No. 22/111. April 8. https://www.imf.org/en/News/Articles/2022/04/08/pr22111-imf-executive-board-approves-establishment-of-a-multi-donor-administered-account-for-ukraine

______. 2022f. “IMF Reaches Staff-Level Agreement with Barbados for a Resilience and Sustainability Trust (RST) program, with an accompanying Extended Fund Facility (EFF)”. Press Release No. 22/325. September 28. https://www.imf.org/en/News/Articles/2022/09/28/pr22325-imf-reaches-staff-level-agreement-with-barbados-rst-program-with-accompanying-eff

______. 2022g. “IMF Reaches Staff-Level Agreement with Costa Rica on a Resilience and Sustainability Facility (RSF) and the Third Review under the Extended Fund Facility (EFF)”. Press Release No. 22/330. October 4. https://www.imf.org/en/News/Articles/2022/10/03/pr22330-imf-reaches-staff-level-agreement-with-costa-rica-on-rsf-and-the-third-review-under-the-eff

______. 2022h. “IMF Reaches Staff-Level Agreement with Rwanda for a Resilience and Sustainability (RST) Program, with an Accompanying Policy Coordination Instrument (PCI)”. Press Release No. 22/340. October 6. https://www.imf.org/en/News/Articles/2022/10/06/pr22340-rwanda-imf-staff-reaches-staff-level-agreement-rst-program-accompanying-pci

______. 2022i. “IMF Support for Low-Income Countries.” January 5. https://www.imf.org/en/About/Factsheets/IMF-Support-for-Low-Income-Countries

______. 2022j. “Proposal to Establish a Resilience and Sustainability Trust.” April. https://www.imf.org/-/media/Files/Publications/PP/2022/English/PPEA2022013.ashx

______. 2022k. “Resilience and Sustainability Facility (RSF).” October 12. https://www.imf.org/en/About/Factsheets/Sheets/2022/resilience-and-sustainability-facility-rsf

______. 2022l. “SDR Interest Rate Calculation.” Accessed October 12, 2022.

https://www.imf.org/external/np/fin/data/sdr_ir.aspx

______. 2022m. “SDR Valuation.” Accessed October 12, 2022.

https://www.imf.org/external/np/fin/data/rms_sdrv.aspx

______. 2022n. “Special Drawing Rights.” July 29. https://www.imf.org/en/About/Factsheets/Sheets/2016/08/01/14/51/Special-Drawing-Right-SDR

______. 2022o. “World Economic Outlook Update July 2022: Gloomy and More Uncertain.” July. https://www.imf.org/en/Publications/WEO/Issues/2022/07/26/world-economic-outlook-update-july-2022

IMF Communications Department. 2022a. Email message to author, July 29.

______. 2022b. Email message to author, August 5.

Kedem, Shoshana. 2021. “#UNGA: African Leaders Call for Additional IMF SDRs for Pandemic Recovery.” African Business, September 23. https://african.business/2021/09/economy/unga-african-leaders-call-for-additional-imf-sdrs-for-pandemic-recovery/

Lagarde, Christine. 2021. “Statement by Christine Lagarde, President of the ECB, at the Forty-Fourth Meeting of the International Monetary and Financial Committee.” Washington, DC: International Monetary and Financial Committee of the International Monetary Fund, October 14. https://www.imfconnect.org/content/dam/imf/Spring-Annual%20Meetings/AM21/IMFCStatePub/IMFC-S-44-21-28%20Statement%20by%20Ms.%20Lagarde%20-%20European%20Central%20Bank.pdf

Lustgarten, Abrahm. 2022. “The Barbados Rebellion.” The New York Times Magazine, July 27. https://www.nytimes.com/interactive/2022/07/27/magazine/barbados-climate-debt-mia-mottley.html

Maki, Sydney. 2022. “Historic Cascade of Defaults Is Coming for Emerging Markets.” Bloomberg, July 7. https://www.bloomberg.com/news/articles/2022-07-07/why-developing-countries-are-facing-a-debt-default-crisis#xj4y7vzkg

Mariotti, Chiara. 2022. “Special Drawing Rights: Can the IMF’s Reserve Currency Become a Transformative Financial Resource?” Brussels, Belgium: European Network on Debt and Development (Eurodad), April. https://assets.nationbuilder.com/eurodad/pages/2897/attachments/original/1649658655/sdr-briefing-apr10-final.pdf?1649658655

Martin, Eric. 2022. “Japan, UK Keen to Channel IMF Support Through Top African Lender.” Bloomberg. September 22. https://www.bloomberg.com/news/articles/2022-09-22/japan-uk-keen-to-channel-imf-support-through-top-african-lender

Martin, Jaime. 2022. “The U.S. Wants to Tackle Inflation. Here’s Why That Should Worry the Rest of the World.” The New York Times, April 28. https://www.nytimes.com/2022/04/28/opinion/fed-inflation-interest-rates-third-world-debt.html

Munevar, Daniel. 2021. “Liquid Illusions: Who Really Benefits from the Liquidity and Sustainability Facility?” Brussels, Belgium: European Network on Debt and Development (Eurodad), June 24. https://www.eurodad.org/liquid_illusions_who_really_benefits

Murillo, Alvaro. 2022. “Costa Rica Asks IMF for $700 Million from New Sustainability Trust.” Reuters, June 25. https://www.reuters.com/world/americas/costa-rica-asks-imf-700-million-new-sustainability-trust-2022-06-25/

One Campaign. 2021. “From Allocation to Action on SDRs.” October. https://cdn.one.org/international/media/international/2021/10/05114447/FROM-ALLOCATION-TO-ACTION-ON-SDRs-ONE-Campaign.pdf

Ortiz, Isabel and Matthew Cummins. 2021. “Global Austerity Alert: Looming Budget Cuts in 2021-25 and Alternative Pathways.” New York: Institute for Policy Dialogue, April. https://policydialogue.org/files/publications/papers/Global-Austerity-Alert-Ortiz-Cummins-2021-final.pdf

Oxfam International. 2022. “IMF Must Abandon Demands for Austerity as Cost-of-Living Crisis Drives up Hunger and Poverty Worldwide.” April 19. https://www.oxfam.org/en/press-releases/imf-must-abandon-demands-austerity-cost-living-crisis-drives-hunger-and-poverty

Oxfam International Washington Office. 2022. “How the IMF is Pushing an Austerity-Based Recovery.” Medium, April 18. https://medium.com/@OxfamIFIs/how-the-imf-is-pushing-an-austerity-based-recovery-f19c6040e918

Plant, Mark. 2022a. “A Setback to SDR Recycling?” Washington, DC: Center for Global Development, March 31. https://www.cgdev.org/blog/setback-sdr-recycling

______. 2022b. “How We Can Put SDRs to Work in the Fight Against Climate Change—The Multilateral Development Bank Option.” Washington, DC: Center for Global Development, April 25. https://www.cgdev.org/blog/how-we-can-put-sdrs-work-fight-against-climate-change-multilateral-development-bank-option

______. 2022c. “The Best Options for Recycling SDRs.” Washington, DC: Center for Global Development, May 25. https://www.cgdev.org/blog/best-options-recycling-sdrs

Plant, Mark, John Hicklin, and David Andrews. 2021. “Reallocating SDRs into an IMF Global Resilience Trust.” Washington, DC: Center for Global Development, September 23. https://cgdev.org/publication/reallocating-sdrs-imf-global-resilience-trust

Plant, Mark and Lucas Sala. 2022. “Does European Tithing of SDRs for Ukraine Make Any Sense?” Washington, DC: Center for Global Development, May 30. https://www.cgdev.org/blog/does-european-tithing-sdrs-ukraine-make-any-sense

______. 2022b. “Tracking Recycled SDRs: More on the Hunt for Bigfoot” Washington, DC: Center for Global Development, August 31. https://www.cgdev.org/publication/tracking-recycled-sdrs-more-hunt-bigfoot

Red Latinoamericana por Justicia Económica y Social (Latindadd). 2021. “CSO Launches Call for the Fair Channeling of Special Drawing Rights / OSC lanza llamado para la canalización justa de los Derechos Especiales de Giro.” September 29. https://www.latindadd.org/2021/09/29/osc-launches-call-for-the-fair-channeling-of-special-drawing-rights-osc-lanza-llamado-para-la-canalizacion-justa-de-los-derechos-especiales-de-giro/

Richard, Adriel. 2022. “Barbados Seeking U.S. $340 Million from the IMF.” NationNews, September 9. https://www.nationnews.com/2022/09/09/barbados-seeking-u-s-340-million-imf/

Sammut, Joe. 2022. “Will US Rate Hikes Hurt Developing Countries?” Washington, DC: Center for Economic and Policy Research, May 27. https://cepr.net/will-us-rate-hikes-harm-developing-countries/

Smialek, Jeanna and Eshe Nelson. 2022. “Global Central Banks Ramp Up Inflation Flight.” The New York Times, July 17. https://www.nytimes.com/2022/07/17/business/economy/global-central-banks-inflation.html

Soto, Alonso. 2022. “Spain Offers $1.9 Billion to New IMF Trust for Fragile Nations.” Bloomberg, July 11. https://www.bloomberg.com/news/articles/2022-07-11/spain-offers-1-9-billion-to-new-imf-trust-for-fragile-nations

Stubbington, Tommy. 2021. “UN Launches African Repo Market in Bid to Lower Borrowing Costs.” Financial Times, November 3. https://www.ft.com/content/0c5c2e7f-32e9-4e91-9fca-fab9d5ff59b7

Stubbs, Thomas, Alexander Kentikelenis, Rebecca Ray, and Kevin P. Gallagher. 2021. “Poverty, Inequality, and the International Monetary Fund: How Austerity Hurts the Poor and Widens Inequality.” GEGI Working Paper 046. Boston, MA: Global Development Policy Center. Boston University. April. https://www.bu.edu/gdp/2021/04/02/poverty-inequality-and-the-imf-how-austerity-hurts-the-poor-and-widens-inequality/

Task Force on Climate, Development and the International Monetary Fund. 2022. “Designing a Resilience and Sustainability Trust: A Development-Centered Approach.” February. https://www.bu.edu/gdp/files/2022/02/TF-PB-002-FIN.pdf

United Nations Conference on Trade and Development (UNCTAD). 2021. “Trade and Development Report 2021.” https://unctad.org/system/files/official-document/tdr2021_en.pdf

United Nations Development Programme (UNDP). 2021. “2021 Global Multidimensional Poverty Index (MPI): Unmasking Disparities by Ethnicity, Caste and Gender.” October 7. https://hdr.undp.org/content/2021-global-multidimensional-poverty-index-mpi#/indicies/MPI

United Nations Economic Commission for Africa (UNECA). 2022. “The Dice is Loaded Against Africa: Ministers Call for Reform.” May 17. https://www.uneca.org/stories/the-dice-is-loaded-against-africa-ministers-call-for-reform

Weisbrot, Mark. 2022. “It Will Be the Fed’s Fault If the Economy Crashes into Recession.” New York: MarketWatch, July 28. https://www.marketwatch.com/story/it-will-be-the-feds-fault-if-the-economy-crashes-into-recession-11659020032

Wheatley, Jonathan. 2022. “Emerging Markets Hit By Record Streak of Withdrawals By Foreign Investors.” Financial Times, July 31. https://www.ft.com/content/35969b19-86db-4197-a419-b4a761094e9a

White House. 2022. “Letter to the Speaker of the House of Representatives on Fiscal Year 2022 Emergency Supplemental Funding.” April 28. https://www.whitehouse.gov/wp-content/uploads/2022/04/FY_2022_Emergency_Supplemental_Assistance-to-Ukraine_4.28.2022.pdf

World Bank. 2022. “Debt Service Suspension Initiative.” March 10. https://www.worldbank.org/en/topic/debt/brief/covid-19-debt-service-suspension-initiative

World Food Programme (WFP). 2022. “A Global Food Crisis.” https://www.wfp.org/global-hunger-crisis