June 13, 2018

Earlier this year we did an analysis of CEO compensation in the health insurance industry to see if it was affected by the cap on deductibility imposed by the Affordable Care Act (ACA). One of the provisions of the ACA limited the amount of CEO pay that health insurers could deduct on their taxes to $500,000, beginning in 2013.

This provision effectively raised the cost of CEO pay to insurers by more than 50 percent. Prior to 2013, the deduction in effect meant that the government was picking up 35 cents of every dollar of CEO pay, while the companies were paying just 65 cents.[1] With the new provision in place, insurers are now paying 100 cents of every dollar of CEO pay in excess of $500,000.

If the pay reflects the value of the CEO to the company, we should expect this change to reduce the pay of CEOs in the insurance industry. For example, if a CEO gets paid $20 million a year, this should mean that she delivers roughly $20 million in additional value to shareholders.

When the CEO’s pay was fully deductible, the $20 million paid to the CEO actually only cost the company $13 million. This would presumably be the number that matters to shareholders since they care about how much money comes out of their pockets, not the number on the CEO’s paycheck.

However, with the change in the tax code, the CEO’s $20 million compensation now costs the shareholders $20 million.[2] We would expect the shareholders to push down CEO pay to the $13 million amount that they previously been paying, net of taxes, or at least to something less than $20 million.

This is what we tested in our earlier analysis. We used a wide variety of statistical specifications, which controlled for factors like revenue growth, profit growth, and share price appreciation. In none of them did we find a statistically significant negative coefficient for the variable for CEO pay in the insurance industry in the years after the cap went into effect. In fact, in most of the specifications, this coefficient was positive, indicating that CEO pay actually rose in the insurance industry, in spite of the cap on the tax deduction.

We saw this result as being consistent with a view that pay does not reflect the CEO’s value to shareholders. In this alternative view, the explosion of CEO pay over the last four decades is primarily attributable to the corruption of the corporate governance process.

CEO pay is most immediately determined by boards of directors. The directors, who are themselves highly paid for very part-time work, largely owe their jobs to CEOs and other top management. Incumbent directors who are re-nominated by the board almost never get removed by shareholders.

In this context, there is little incentive for directors to ever reduce CEO pay. This is about the only way for them to put their job at risk since they could anger both top management and their colleagues on the board. As a result, there is no effective check on CEO pay, which is why it keeps rising higher. In the most recent data, CEO pay averages more than 200 hundred times the pay of ordinary workers, and as recent SEC disclosures show, it can be more than 1000 times the pay of a typical worker.

While our results were very much in keeping with the corrupt corporate governance story, it was pointed out to us by Boston University Law Professor David Walker that we may not have used the best measure of CEO compensation in our analysis.

There are several different commonly used ways to measure CEO pay. In our original analysis, we had applied a measure that used the realized value of stock options at the time they were vested. This can be thought of as a measure of what the CEO got for their work.

By contrast, Professor Walker suggested that we apply a measure of CEO pay that uses the ex ante value of stock options at the time they were issued. This can be thought of as being what the company thinks it is paying the CEO. For the analysis we were doing, Professor Walker is correct; it would be more appropriate to use the ex ante value of the options that the company issued at the time.

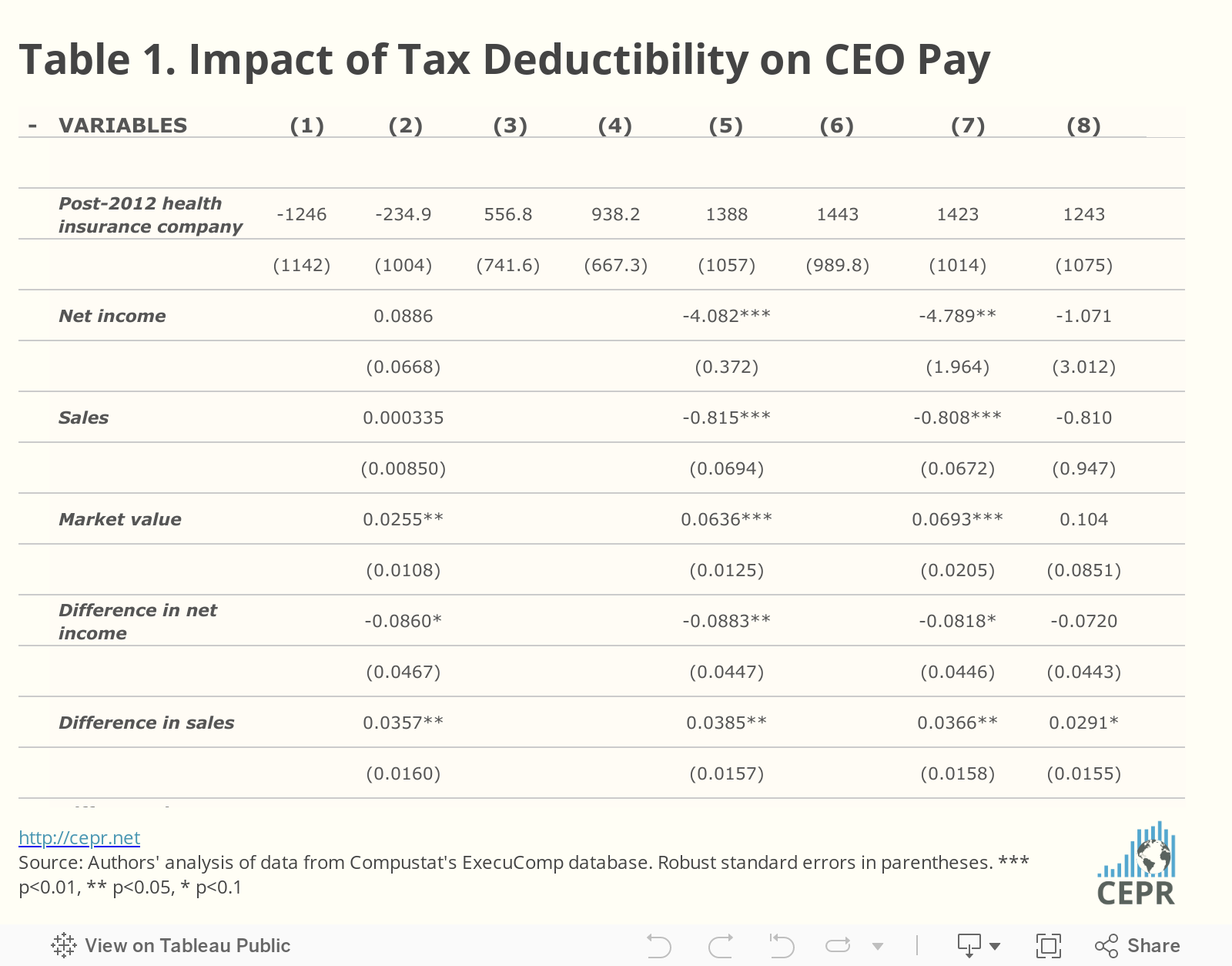

We redid the analysis using the measure of CEO compensation that includes the ex ante value of stock options. Table 1 below reproduces the regressions shown in Table 2 of our paper.

As can be seen, with this specification we again find no evidence that CEO pay fell in response to the cap on deductibility. None of the specifications has a negative coefficient on the variable for insurers in the years when the cap was in effect that is close to being statistically significant. In fact, for most of the specifications, the coefficient is positive. It’s also worth noting that these regressions have a somewhat higher explanatory power than the set in our original analyses, which is consistent with the use of the ex ante value of stock options being a better measure of CEO pay for this analysis.

As we noted in the original paper, our sample is relatively small, and it only includes four years in which the insurance market was undergoing major transformations, so this analysis cannot be seen conclusive. Still, it does provide grounds for questioning whether caps on the deductibility of CEO pay (as was done more generally in the 2017 Tax Cut and Jobs Act) will be an effective way to limit CEO pay. And, it also supports the view that CEO pay is not closely related to returns to shareholders.

Finally, to be clear, we support ending the deductibility of all CEO pay over a threshold of $500,000. Currently, “performance-based” pay is fully deductible, regardless of its amount. Ending the deductibility of “performance-based” pay would raise a modest amount of revenue for the federal government. Further, allowing “performance-based” pay to be deductible could give a signal that policymakers think that these compensation packages are somehow efficiency-enhancing or fair. But, much of the research shows that they are not and “performance-based” measures are often gamed or manipulated so that they serve no efficiency or equity goals at all. Ending the deductibility of all CEO pay over a threshold is a good policy, but it is not likely to be a game-changer by itself in restraining excess managerial pay.

[1] Until 2018 the corporate income tax rate was 35 percent.

[2] This ignores the fact that they can still deduct the first $500,000.