August 04, 2021

This post originally appeared on the Duke University School of Law FinReg Blog.

Convenience, speed, and cost are important considerations for electronic payments. Recent events surrounding the COVID-19 pandemic may accelerate these trends as peoples’ willingness to handle cash may be waning. As policy makers try to assess the benefits and risks of Central Bank Digital Currencies (CBDC) researchers at central banks and academic institutions have contributed to the discussion with theoretical works on monetary policy, disintermediation, and financial stability implications.(See Bordo and Levin, 2017; Andolfatto, 2019; Bindseil, 2019; Chiu et al., 2019; Keister and Sanches, 2019; Fernández-Villaverde et al., 2020; Schilling et al., 2020, and Garratt and Zhu, 2021.)

However, when it comes to actual implementation, there is no substitute for experience. In our recent paper, we provide a detailed account of the Ecuadorian experience with Dinero Electrónico (DE). DE was a real-time gross settlement retail mobile payment system developed by the Banco Central del Ecuador (Central Bank of Ecuador; hereafter: BCE) that allowed citizens to transfer money from person to person using the mobile phone operators’ Unstructured Supplementary Service Data (USSD) protocol, the same protocol originally used by Kenya’s M-Pesa. DE was the first CBDC based on a mobile platform.

DE Simplicity of Access

Although the first regulations were issued in 2011, DE operated from 2014 to 2018. Real time information provided by various governmental institutions made registering easy. Citizens of Ecuador could open an account by accessing the gateway, registering their national identity number, and answering security questions. People deposited or withdrew hard currency by going to designated transaction centers. At its peak, DE had 500,000 users.

A great advantage in the design of DE, which was proposed and implemented by the BCE, was its simplicity of access: users did not require Internet access, did not have to pay charges for the use of the cell phone line, and did not need to make an initial deposit or fill out any application. The only requirement was owning a cell phone operating through any one of the nationwide carriers and the person’s identity card. For a developing country, this meant that the design increased financial inclusion.

DE Simple P2P Demo

Origin and Tug-of-war

Ecuador became dollarized in 2000 and DE accounts were denominated in USD. After the 2008 oil shock resulted in a Balance of Payments deficit and a shortage of physical cash, the BCE carried out three initiatives to optimize the use of the dollar.

First, the government issued low denomination electronic securities/T-bills that were intended to be used as currency to make payments. When the Internal Revenue Services started to accept these securities as payment for taxes, their price discount in the secondary market dropped from 20 percent to 2.3 percent.

The second attempt was FactoRepo, a B2B accounts-receivable invoice clearing initiative launched in 2009 that sought to reduce liquidity needs of small producers and entrepreneurs by settling on a net basis. The FactoRepo prototype was evaluated in a simulation using tax data on transactions. It showed a large concentration of liquidity in few firms; supply chains quickly reached importers; and many formal businesses do not pay for their agricultural raw materials with invoices. Thus, the BCE would have required a contingency fund to backstop the system to convert net surpluses into cash. Legal issues regarding the backstop function aborted the project after the prototype phase.

Third, there was a central bank mobile money initiative. Official or de jure dollarization is the adoption of a foreign unit of account as legal tender. The central bank is responsible for the conversion of domestic bank book money (xenodollars) into foreign-issued notes and coins (Fed dollars). The BCE has to acquire USD by selling other assets, a drain on official international reserve holdings. At the time, it was estimated that 82 percent of all retail payments in Ecuador were settled in cash and only 10 percent were bank transfers. BCE ultimately reached the conclusion that the best way to reduce the drain of its reserves was to extend its domestic electronic payment system by improving financial inclusion.

The initial launch of DE was in 2012. However, DE was rolled back because private banks disagreed with a central-bank-centered model. The platform name was changed to Sistema de Pago Móvil, and new regulations only allowed for transfers from deposit accounts in a financial institution. It did not involve the creation of central-bank-issued mobile money.

On February 28, 2014, the original DE legislation was reinstated. These changes turned the DE initiative back into a central-bank-issued mobile money scheme. The new system, with some improvements including payment system integration, operated with partial success and with heavy promotion by the government.

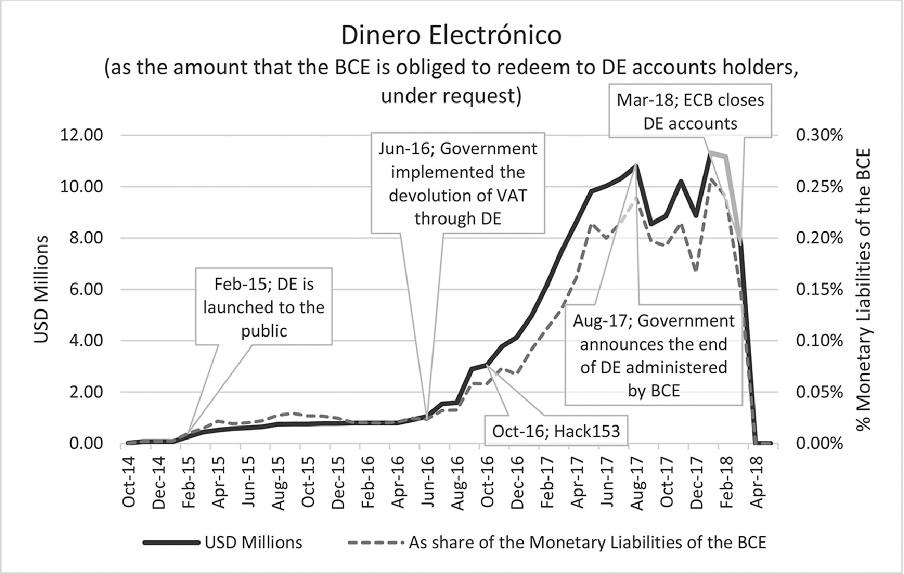

In August 2017, a new government decided that the BCE would no longer administer the system and that private banks would deploy one instead. This was an agreement between Ecuador’s largest banks and the new government. A Presidential veto to an economic law terminated DE. By March 2018, DE was no longer in force.

Deployment

DE was designed to serve multiple practical purposes. For example, there were initiatives to use it for public transportation, online purchases, e-government services, and nano-credits. In 2017, the Ecuadorian government, NGOs and private firms organized the HACK153 Hackathon to develop API-based solutions using DE: 28 innovations resulted from this campaign, including app-based wallets for smartphones.

The Ecuadorian government launched a program whereby DE users received a rebate of 2 percentage points off the Value Added Tax (VAT) paid. An increase in usage followed the devolution of VAT in 2016, but this was mostly due to an increase in transactions by previous users, rather than the addition of new users. Until December 2017, 71 percent of the accounts were not used at all, and only 10 percent were used to make payments for goods and services, including public services. The government announced that public workers could request a portion of their salary to be transferred automatically to DE accounts. However, public institutions never developed a standardized procedure for doing so. In 2017, only 490 government employees (roughly 0.1 percent) received their salary in DE accounts.

Figure 1. Amounts in DE accounts

Transaction fees were competitive and transactions were executed through a real-time gross settlement system.

Transfers of less than 1.00 USD between two individual accounts of the DE system involved a 0.015 USD fee, transfers between 1.00 USD and 11 USD involved a 0.02 USD fee; the most expensive transfers, between 2,001 USD and 9,000 USD, involved a 0.15 USD fee. In contrast, an interbank transfer between two individual bank accounts could cost up to 0.45 USD and involved delayed net settlement (processed within 24 to 48 hours). A transfer from a DE account to a private bank account cost 0.25 USD. The fee for processing payments (not between citizens, but between a citizen and a firm) through DE was 0.02 USD for transactions of less than 10.00 USD, and 0.20 USD for transactions of more than 100.00 USD (up to 9,000.00 USD). In contrast, the commissions for credit cards range from 4.5 to 10 percent of the value of the sale and the payment could be processed with a delay.

The banks’ alternative

After a long gap, Ecuador’s banks finally deployed the inter-bank alternative late in 2019 called billetera móvil (BIMO). It is a mobile wallet developed by Banred, a clearing house owned by a consortium of banks. People without existing bank accounts can theoretically open an account in a few minutes, without submitting any documentation. As of May 2020, 96 percent of BIMO’s 89,000 accounts were associated with previously existing savings and checking accounts, while only 4 percent were new accounts created within BIMO. As of July 2020, BIMO had not reached 50,000 downloads on Google Play.

Table 1. Comparison between BIMO (as proposed in 2019) and DE (as of its end in 2017)

| BIMO | DE | |||

|---|---|---|---|---|

| Features | ||||

| Technology requirements | Internet | Yes | No | |

| Smartphone | Yes | No | ||

| Other requirements | Bank account | Yes (basic accounts can be opened without documentation). | No | |

| Transaction Limits | USD50 per transaction, USD100 per day, USD300 per month. | No | ||

| Backing | Backed by | Private Banks deposit accounts | BCE liquid assets | |

| Redeemed by | Private Banks | BCE | ||

| Provider | BANRED | BCE | ||

| Settlement | Real time gross | Real time gross | ||

| Fees (USD) | Transaction between participants (individuals, not firms) | USD 0.01 – 5.00 | 0.09 | Free |

| USD 5.01 – 10.00 | 0.09 | 0.02 | ||

| USD 10.01 – 50.00 | 0.09 | 0.10 | ||

| USD 50.01 – 100.00 | not available | 0.10 | ||

| USD 100.01 – 9000.01 | not available | 0.20 | ||

| Redeeming in ATM | 0.45 | 0.35 |

Criticisms: Surveillance and Dedollarization

Alejandro Salas, then the regional director for the Americas of Transparency International, when interviewed by The Guardian, stated: “This can become a huge invasion of privacy because with electronic banking you can follow, even detect where the person is, and how much the person is spending. It has the potential to be a surveillance program.”

DE was designed to be traceable due to regulatory requirements. All transfers automatically record the identities of the sender and receiver, so it would be easy to criminally investigate the origin and recipient of any transfer. Although all DE information was stored, it was handled automatically by the platform, requiring minimal human intervention. Thus, one can argue that there was no inherent surveillance problem associated with DE.

The same concerns regarding data exploitation apply to information used for Internet transfers, debit cards, credit cards, credit history, and so on. This is evident from recent discussions surrounding Facebook’s Libra/Diem and other local issues. Christine Lagarde, former IMF managing director, has made the case that the central bank is a better steward of payments data than a private corporation would be.

Some Ecuadorian analysts stated that DE was designed to be a parallel or sovereign currency that was intended to cover the fiscal shortfall and thus put dollarization at risk. Critics such as the local association of private banks challenged whether DE was backed 100 percent by cash, arguing that if it was not, then DE was a new form of sovereign currency.

DE Was Backed by Cash

Although DE was not legally fully backed by USD bills, it was fully backed by USD-denominated assets. According to article 101 of the Código Orgánico Monetario y Financiero (2014) — the monetary law — DE was fully backed by liquid assets of the Banco Central. This policy was reaffirmed in an official ruling: Resolución Nro. 274-2016 of the Junta de Política y Regulación Monetaria y Financiera (art. 5). Moreover, DE was readily convertible to USD bills on demand. The holder of DE had a direct claim on USD banknotes, which made DE distinct from a typical “sovereign” currency. Some critical analysts argued that because DE was a claim on the BCE’s holdings of US dollars, and not a digital representation of a domestic fiat currency, that DE was not devoid of credit risk, and this may have induced some consumers to perceive it as more risky than other means of payment. This perceived risk could have been a factor that led some consumers not to adopt DE.

At all moments in its lifespan, the BCE held actual USD banknotes that were more than sufficient to meet expected DE cash conversions.

Main Conclusions: Ecosystem and Banks’ Acquiescence

The initial deployment competed directly with banks’ incumbent businesses. BCE should not have deployed a one-to-one commercial transaction center designation strategy. It should have developed an API platform-based open innovation and business model. The number of cash-in/loading transaction centers was limited, and some of them required the user to wait in line. In contrast, there are thousands of points to top-up (i.e., buy) airtime for mobile phones nationwide, including small convenience stores, drug stores, and even individual sellers waiting at traffic lights and using their own cell phones to sell mobile airtime. A small number of companies control the system for mobile phone top-up. DE could have used the same scheme, as was originally designed for the 2011 version, through an agreement with wholesale top-up resellers. BCE, together with the government, should have first promoted DE adoption in younger demographics and the rural areas.

Additionally, given that there was no fee for small transactions, every DE user had the potential to be a DE top-up charge agent and arbitrageur: they could receive an amount in cash and transfer it by DE. This mechanism was not announced explicitly by the Banco Central, and many users did not realize it was feasible and convenient.

Ultimately, the banking sector’s opposition contributed significantly to DE’s demise, as admitted by the new government’s BCE general manager. The Ecuadorian experience suggests that the support or acquiescence of the private banking sector is crucial to the success of any CBDC initiative. Indeed, most advocates of CBDC do not seek to undermine their two-tier banking systems. Rather, they see CBDC as a potentially necessary evolution of their strategy to meet their existing mandate to provide payment services. Many countries are simultaneously working with their commercial banks to modernize their retail-payment systems, and at the same time they are contemplating CBDCs. As DE demonstrates, this could create a tension that will be difficult to manage if not properly addressed.