I am not ordinarily a celebrant for the state of the economy, but the media have been so over the top in pushing the economic doom story during the Biden presidency, that I feel the need to put some reality into the picture.

One of the central lines among the doomsayers is that we are spending a larger share of income on housing and that for many it has become altogether unaffordable. I will agree that housing is a serious problem. In fact, I recently authored a piece in a new collection on the issue, which I would encourage everyone to read. We need to build more housing and especially more affordable housing.

But acknowledging that housing is a serious problem is not the same as saying it is an unprecedented crisis, and many of the things that have been asserted in the media are simply not true. For example, it is not true that homeownership is no longer part of the American dream for young people. In fact, homeownership rates for young people are above their pre-pandemic level.

It’s true that the run-up in mortgage interest rates since the Fed began hiking in March 2022, coupled with rising house prices, has made the cost of buying a home prohibitive for many new buyers, but few expect rates to stay this high for long.

Mortgage rates are highly cyclical, they go up when the Fed raises rates in an effort to slow the economy. The current rates of near 7.0 percent are high compared to the 3.0 percent rates we saw during the pandemic, but they are not high by historic standards. In 1981, they peaked at over 18.0 percent.

I don’t recall reporters at the time writing pieces as though 18.0 percent mortgage rates would persist for the indefinite future. I am not sure why they feel the need to write that way about the current 7.0 percent rates.

Another aspect of the manufactured housing crisis story is that we are spending higher shares of our income on housing, with a record number of people spending more than one-third of their income on housing. This share has been dubbed as a crisis point by some.

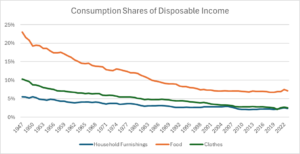

It is certainly true that we are spending a much larger share of our income on housing than in prior decades, but a big part of that story is that we are spending a much smaller share on other things. The graph below shows the share of disposable income going to food, clothes, and household furnishings since the late 1940s.

Source: National Income and Product Accounts, Table 2.3.5 and author’s calculations.

As can be seen, there has been a sharp reduction in the shares of all three. This is especially striking with food. In 1947 we spent 23.0 percent of our income on store-bought food. This had fallen to just 7.1 percent last year. The share of income going to buy clothes fell from 10.3 percent to 2.6 percent. The share for buying household furnishings dropped from 5.5 percent to 2.5 percent.

These declines freed up income to go to other areas, and one area that extra income went to was housing. The houses we live in today are on average much larger than the ones we lived in 75 years ago. They are also far more likely to have air conditioning and relatively clean sources of heat. (Coal furnaces were still common in the late 1940s.) They are much better protected against fires and less likely to have harmful chemicals like asbestos and lead.

As a result of reduced spending in other areas, and the higher quality of the housing we live in today, the share of our income going to housing now exceeds 34.0 percent, on average. (This figure includes “owner equivalent rent,” the money that a homeowner would be paying to rent the home they live in.)

Given the 34.0 percent figure is an average, it is hard to see the one-third level as a crisis. Rather, we probably need to recalculate what share of income going to housing costs presents an unmanageable burden.

None of this should be taken to mean that we don’t have to do things to make housing more affordable. We need to ease up restrictions that block both new construction and the conversion of empty office space to residential. And we should ensure that a substantial share of these new units are affordable.

We can also take short-term steps to improve affordability, like limiting vacation rentals and having moderate rent control. A vacant property tax is also a good way to get more units on the market. It will also be good when Jerome Powell and the Fed get over their inflation fears and start to ease up on interest rates.

We have a serious shortage of housing in the country due to a sharp plunge in construction in the decade following the collapse of the housing bubble. We were gradually getting back to more normal levels of construction when the pandemic broke out. If we can sustain higher levels of construction for several years and convert many of the offices that are currently vacant, due to the explosion in people working from home, we can lower housing costs.

But it is helpful to look at the issue with clear eyes. The biggest reason housing has grown as a share of our income is that we are spending so much less on other necessities. That is a good thing.

I am not ordinarily a celebrant for the state of the economy, but the media have been so over the top in pushing the economic doom story during the Biden presidency, that I feel the need to put some reality into the picture.

One of the central lines among the doomsayers is that we are spending a larger share of income on housing and that for many it has become altogether unaffordable. I will agree that housing is a serious problem. In fact, I recently authored a piece in a new collection on the issue, which I would encourage everyone to read. We need to build more housing and especially more affordable housing.

But acknowledging that housing is a serious problem is not the same as saying it is an unprecedented crisis, and many of the things that have been asserted in the media are simply not true. For example, it is not true that homeownership is no longer part of the American dream for young people. In fact, homeownership rates for young people are above their pre-pandemic level.

It’s true that the run-up in mortgage interest rates since the Fed began hiking in March 2022, coupled with rising house prices, has made the cost of buying a home prohibitive for many new buyers, but few expect rates to stay this high for long.

Mortgage rates are highly cyclical, they go up when the Fed raises rates in an effort to slow the economy. The current rates of near 7.0 percent are high compared to the 3.0 percent rates we saw during the pandemic, but they are not high by historic standards. In 1981, they peaked at over 18.0 percent.

I don’t recall reporters at the time writing pieces as though 18.0 percent mortgage rates would persist for the indefinite future. I am not sure why they feel the need to write that way about the current 7.0 percent rates.

Another aspect of the manufactured housing crisis story is that we are spending higher shares of our income on housing, with a record number of people spending more than one-third of their income on housing. This share has been dubbed as a crisis point by some.

It is certainly true that we are spending a much larger share of our income on housing than in prior decades, but a big part of that story is that we are spending a much smaller share on other things. The graph below shows the share of disposable income going to food, clothes, and household furnishings since the late 1940s.

Source: National Income and Product Accounts, Table 2.3.5 and author’s calculations.

As can be seen, there has been a sharp reduction in the shares of all three. This is especially striking with food. In 1947 we spent 23.0 percent of our income on store-bought food. This had fallen to just 7.1 percent last year. The share of income going to buy clothes fell from 10.3 percent to 2.6 percent. The share for buying household furnishings dropped from 5.5 percent to 2.5 percent.

These declines freed up income to go to other areas, and one area that extra income went to was housing. The houses we live in today are on average much larger than the ones we lived in 75 years ago. They are also far more likely to have air conditioning and relatively clean sources of heat. (Coal furnaces were still common in the late 1940s.) They are much better protected against fires and less likely to have harmful chemicals like asbestos and lead.

As a result of reduced spending in other areas, and the higher quality of the housing we live in today, the share of our income going to housing now exceeds 34.0 percent, on average. (This figure includes “owner equivalent rent,” the money that a homeowner would be paying to rent the home they live in.)

Given the 34.0 percent figure is an average, it is hard to see the one-third level as a crisis. Rather, we probably need to recalculate what share of income going to housing costs presents an unmanageable burden.

None of this should be taken to mean that we don’t have to do things to make housing more affordable. We need to ease up restrictions that block both new construction and the conversion of empty office space to residential. And we should ensure that a substantial share of these new units are affordable.

We can also take short-term steps to improve affordability, like limiting vacation rentals and having moderate rent control. A vacant property tax is also a good way to get more units on the market. It will also be good when Jerome Powell and the Fed get over their inflation fears and start to ease up on interest rates.

We have a serious shortage of housing in the country due to a sharp plunge in construction in the decade following the collapse of the housing bubble. We were gradually getting back to more normal levels of construction when the pandemic broke out. If we can sustain higher levels of construction for several years and convert many of the offices that are currently vacant, due to the explosion in people working from home, we can lower housing costs.

But it is helpful to look at the issue with clear eyes. The biggest reason housing has grown as a share of our income is that we are spending so much less on other necessities. That is a good thing.

Read More Leer más Join the discussion Participa en la discusión

I was a bit surprised to see a piece on Marketplace radio telling listeners:

“In 1947, U.S. workers got about two-thirds of the income from their labors. ‘Now, they’re getting something that is just a little bit over half. And so they’re getting less of the pie,’ said Erica Groshen, who used to head the Bureau of Labor Statistics and is now at Cornell.”

I was surprised because it’s not true. There have been ups and downs in the labor share of income over this period, but there is no downward trend. In 1947, it was 67.7 percent of net value-added in the corporate sector. In 2023, it was 67.8 percent of net value in the corporate sector. Here’s the picture.

Source: NIPA Table 1.14 and author’s calculation.

As can be seen, there is some rise in the labor share in the sixties and seventies, which is sustained in the eighties and nineties. The labor share then falls back to its late forties level in the first two decades of this century. (This calculation comes from NIPA Table 1.14, Line 4 divided by Line 3.)

It’s true that the typical worker has seen their share of the pie fall, but this is mostly from upward redistribution within the wage distribution. A much larger share of wage income is going to high-end earners, such as CEOS and other top execs, Wall Street types, well-situated STEM workers and protected professionals like doctors and dentists.

This upward redistribution is a huge issue, but we should be clear that most of the story on the before-tax side was highly paid workers pocketing more, not an increase in the profit share. On the after-tax side, because the corporate tax rate has fallen sharply, corporations are taking home a larger share of the pie.

I was a bit surprised to see a piece on Marketplace radio telling listeners:

“In 1947, U.S. workers got about two-thirds of the income from their labors. ‘Now, they’re getting something that is just a little bit over half. And so they’re getting less of the pie,’ said Erica Groshen, who used to head the Bureau of Labor Statistics and is now at Cornell.”

I was surprised because it’s not true. There have been ups and downs in the labor share of income over this period, but there is no downward trend. In 1947, it was 67.7 percent of net value-added in the corporate sector. In 2023, it was 67.8 percent of net value in the corporate sector. Here’s the picture.

Source: NIPA Table 1.14 and author’s calculation.

As can be seen, there is some rise in the labor share in the sixties and seventies, which is sustained in the eighties and nineties. The labor share then falls back to its late forties level in the first two decades of this century. (This calculation comes from NIPA Table 1.14, Line 4 divided by Line 3.)

It’s true that the typical worker has seen their share of the pie fall, but this is mostly from upward redistribution within the wage distribution. A much larger share of wage income is going to high-end earners, such as CEOS and other top execs, Wall Street types, well-situated STEM workers and protected professionals like doctors and dentists.

This upward redistribution is a huge issue, but we should be clear that most of the story on the before-tax side was highly paid workers pocketing more, not an increase in the profit share. On the after-tax side, because the corporate tax rate has fallen sharply, corporations are taking home a larger share of the pie.

Read More Leer más Join the discussion Participa en la discusión

It is much more acceptable in policy circles to talk about ways to make tax and transfer policy more progressive than ways to structure the market to prevent the distribution of income from being so unequal in the first place. I always harp on this failure, since it seems much easier to keep rich people from getting so rich in the first place than to try to tax away their money once they have it.

Unfortunately, there is little place in policy circles for this sort of discussion. We can speculate on the reason for the lack of interest but there can be little doubt that we could structure the market in ways that generate much less inequality.

There would be far fewer great fortunes in a financial sector that is subject to financial transactions tax similar to the sales taxes that people pay when they buy clothes and food in most states. We would have many fewer top executives earning millions and tens of millions a year if our corporate governance structure was not so corrupt.

Our doctors and other high-end professionals would earn paychecks much more like their counterparts in Europe and Canada if the free traders applied the same logic to their services as they do to trade in manufactured goods. And Mark Zuckerberg and Elon Musk’s stakes in Meta and Twitter would be worth much less if they didn’t enjoy the special protection against defamation suits that we give social media platforms with Section 230.

Then there is my favorite: government-granted patent and copyright monopolies. Large segments of the economy, most importantly prescription drugs and computer software, are almost completely dependent on this form of government intervention. Many of the country’s great fortunes, most notably centibillionaire Bill Gates, depend on these monopolies. More recently we created at least five Moderna billionaires by allowing the company to have control of a vaccine that the government paid to develop.

The proponents of these government-granted monopolies always argue that they provide incentives to innovate and do creative work. That is true, but also not the issue. The question is whether these monopolies are the best way to provide incentives. They are not the only way.

This is most clear in the case of prescription drugs. The U.S. government already spends well over $50 billion a year supporting biomedical research through the National Institutes of Health (NIH) and other government agencies. Few question the value of this research, and in fact the pharmaceutical industry is its biggest proponent. Obviously, valuable research can be supported by direct public funding, outside of the patent system.

However, most of NIH’s funding goes to support basic research, with the instances where it funds the development and testing of a new drug being exceptions. That is by design, NIH deliberately leaves the downstream work to be done by the industry. This does not have to be the case. There is no intrinsic reason that later stage development and testing cannot also be supported by public funding, instead of government-granted patent monopolies, as was the case with the Moderna vaccine.

We are not about to switch from patent monopoly supported system to a publicly funded system overnight, but we can try to find situations where we can experiment with alternative funding mechanisms and compare the outcomes side by side.[1] We actually have a very good opportunity for such a test with Covid boosters.

Drs. Peter Hotez and Maria Elena Bottazzi, along with their colleagues at Baylor College of Medicine and Texas Children Hospital, developed a Covid vaccine, Corbevax. This vaccine has now been administered to well over 100 million people in India and Indonesia, protecting them against serious illness and death from Covid.

Corbevax was developed on an open-source model. This means that the process for producing the vaccine, as well as the data on safety and effectiveness, is entirely open and available to anyone. That means anyone in the world with the necessary manufacturing facilities can produce the vaccine. As a result, the vaccine is cheap, selling for around $2.50 a dose in India and Indonesia.

It would be desirable to have the Corbevax vaccine available in the United States. While it would likely cost somewhat more here, due to higher costs for labor and other items, we’re probably talking around $5 a shot. That compares to over $100 a shot for boosters of Moderna and Pfizer, by far the dominant vaccines in the U.S. (Most people don’t see this price tag, since insurers or the government are picking up much or all of the tab for the boosters, but we do ultimately pay this cost through one pocket or another.)

In addition to the far lower price tag, Corbevax also has the benefit of not being an mRNA vaccine. Instead, it uses a much older protein-based technology. Many of the people that still have not gotten a Covid vaccine are distrustful of mRNA technology. Whether or not these fears are well-grounded, they are keeping people from getting a vaccine which could protect them against Covid. At least some of these people may take advantage of the opportunity to get a vaccine that is not based on mRNA technology.

The FDA Obstacle

The reason that Corbevax is not available to people in the United States is that the Food and Drug Administration (FDA) will not allow it to be distributed here. The FDA is demanding that to get approved, the vaccine go through a full clinical trial to demonstrate its safety and effectiveness.

As it well knows, a full clinical trial at this point would be extremely difficult and expensive.[2] Since the overwhelming majority of people in the country have either already been vaccinated and/or been infected, it would be necessary to have an extremely large sample, likely hundreds of thousands of people, to demonstrate the effectiveness of Corbevax at this point. Note, this is entirely an issue of establishing effectiveness. At this point, there is little question that the vaccine is safe, with over a hundred million doses given and very few instances of adverse effects.

The alternative to a full clinical trial is a bridging study. This is designed to show that the Corbevax boosters give patients target levels of antibodies against the latest strain of Covid. This is the same process that Moderna and Pfizer go through when they have gotten their boosters approved. The FDA has resisted allowing Corbevax to be approved through this channel claiming that it is a fundamentally different technology.

That is true if the comparison is with the mRNA vaccines, but the FDA has given approval to a Novavax Covid vaccine, which uses a similar protein-based technology. (The Novavax vaccine is not widely available due to manufacturing problems.) There seems little downside in approving the Corbevax vaccine, if it can meet the FDA’s standards for determining effectiveness in a bridging study.

The FDA’s Stubborness Is a Big Deal

It would be great if a cheap non-mRNA booster were widely available. As noted before, some people resist getting the vaccine out of fear of the mRNA technology. This will give people a non-mRNA option. There are also people who have bad reactions to the mRNA vaccines (I am definitely in that category – knocks me out for at least a day), who would definitely prefer a non-mRNA option.

But the biggest issue here is the prevention of a serious test of alternatives to the patent monopoly system of financing drug and vaccine development. We pursue this route for developing drugs and vaccines because the pharmaceutical industry works hard to stifle any consideration of alternatives. This is a huge issue not only for public health but also as an economic matter.

As a public health matter, it is entirely this system of government-granted patent monopolies that creates the problem of expensive drugs. It is rare that a drug is actually expensive to produce and manufacture. Drugs are expensive because we give drug companies monopolies over an item that is essential for people’s health, or even their life.

To take a couple of recent examples, the retail price for Imatinib, a leukemia drug, is over $2,500 per prescription. The generic version sells for $13.40, less than one percent of the patent-protected price. The patent protected price for the prostate cancer drug Xtandi is $125 a capsule. A generic version is available at $7.50 a capsule or 6 percent of the patent-protected price.

The most dramatic case of patent monopolies being an obstacle to saving lives was in AIDS pandemic. Initially, the only treatment for AIDS was AZT, which slowed the advance of the disease, but did not cure it and generally lost effectiveness over time. In the early 1990s, the drug companies developed a triple cocktail of drugs that proved effective in keeping AIDS under control and allowing patients to live normal lives. They were selling it for around $15,000 a year.

That was expensive even in the United States, but it was a tab that insurers or the government could afford, even if most patients would have trouble paying it out of pocket. However, this sum was totally out of reach in Sub-Saharan Africa, where the per capita income for many countries was less than $1,000 a year. While the drug companies clearly incurred substantial expenses in developing the drugs, once they were developed, they were relatively cheap to produce.

This was proven when Cipla, a huge Indian generic manufacturer, agreed to make the drugs available at a cost of $1 a day. As a result, millions of lives were saved since this was a price that even low-income countries and international aid organizations could afford to pay.

Patent Monopolies on Prescription Drugs are a Huge Economic Issue

Even beyond their enormous health consequences, patent monopolies on drugs have enormous economic consequences. We will spend close to $650 billion this year on prescription drugs. We would likely be paying less than $100 billion if these drugs were sold in a free market without patent monopolies or related protections. The difference of more than $500 billion a year comes to almost $4,000 a year for an average family. It is more than half the size of the military budget. It is real money by almost any standard.

And, it goes into the pockets of the drug companies, making their top executives, their shareholders, and some highly employees very wealthy. This redistribution of income from the rest of us to a relatively small clique of people in the pharmaceutical industry has nothing to do with the free market. It is the result of a government policy on granting monopolies and related protections.

This massive upward redistribution could perhaps be justified if it were the only way to finance the sort of breakthroughs we have seen in recent decades that have radically and improved people’s lives. But as I have argued, there is good reason to think that we could pay for the development of new drugs and vaccines through alternative mechanisms.

That is why the FDA’s role in blocking Corbevax is such a big deal. This would be a very clear way to demonstrate to the public that we don’t need patent monopolies to provide incentives for developing new drugs and vaccines.

We could look to have direct funding to support the development of drugs and vaccines for other diseases, where the final product was also available on an open-source basis and sold as a cheap generic. The industry could continue with its patent-monopoly supported research, they would just have the risk that whatever they ended up developing may be competing with a generic that is every bit as good and selling for less than one percent of the price they want to charge.

This mechanism for funding would also remove the enormous incentive to lie that patent monopolies create. When drug companies can sell drugs at markups of many thousand percent, they have a powerful incentive to push their drugs as widely as possible, as was the case with the opioid crisis.

Also, we could finance research that is is not dependent on finding a patentable product. In many cases, nutrition or environmental factors may play an important role in health. As it is now structured, the pharmaceutical industry has no incentive to research this possibility, since they won’t stand to earn back their research costs by finding treatments along these lines.

Corbevax: A Foot in the Door

There is a huge amount at stake in a move away from the patent monopoly system of financing the development of prescription drugs. With all the problems of the current system, it has led to many important breakthroughs. If we are to go a different route, we need evidence that it can be equally effective.

The Corbevax vaccine provides one such example. If it were widely distributed and people could see the benefits, then we might be able to build the case for more support and experimentation in this direction. That sounds like a great path if the goal is to improve public health and reduce inequality. However, this likely sounds very bad from the perspective of the pharmaceutical industry, and apparently also the FDA.

[1] Two decades ago, Doctors Without Borders launched its Drugs for Neglected Diseases Initiative. Working on an open-source model, this project has developed thirteen treatments that have benefitted hundreds of millions of people, spending less than what the pharmaceutical industry claims it costs them to develop a single drug.

[2] There were clinical trials done in India to demonstrate the safety and effectiveness of Corbevax.

It is much more acceptable in policy circles to talk about ways to make tax and transfer policy more progressive than ways to structure the market to prevent the distribution of income from being so unequal in the first place. I always harp on this failure, since it seems much easier to keep rich people from getting so rich in the first place than to try to tax away their money once they have it.

Unfortunately, there is little place in policy circles for this sort of discussion. We can speculate on the reason for the lack of interest but there can be little doubt that we could structure the market in ways that generate much less inequality.

There would be far fewer great fortunes in a financial sector that is subject to financial transactions tax similar to the sales taxes that people pay when they buy clothes and food in most states. We would have many fewer top executives earning millions and tens of millions a year if our corporate governance structure was not so corrupt.

Our doctors and other high-end professionals would earn paychecks much more like their counterparts in Europe and Canada if the free traders applied the same logic to their services as they do to trade in manufactured goods. And Mark Zuckerberg and Elon Musk’s stakes in Meta and Twitter would be worth much less if they didn’t enjoy the special protection against defamation suits that we give social media platforms with Section 230.

Then there is my favorite: government-granted patent and copyright monopolies. Large segments of the economy, most importantly prescription drugs and computer software, are almost completely dependent on this form of government intervention. Many of the country’s great fortunes, most notably centibillionaire Bill Gates, depend on these monopolies. More recently we created at least five Moderna billionaires by allowing the company to have control of a vaccine that the government paid to develop.

The proponents of these government-granted monopolies always argue that they provide incentives to innovate and do creative work. That is true, but also not the issue. The question is whether these monopolies are the best way to provide incentives. They are not the only way.

This is most clear in the case of prescription drugs. The U.S. government already spends well over $50 billion a year supporting biomedical research through the National Institutes of Health (NIH) and other government agencies. Few question the value of this research, and in fact the pharmaceutical industry is its biggest proponent. Obviously, valuable research can be supported by direct public funding, outside of the patent system.

However, most of NIH’s funding goes to support basic research, with the instances where it funds the development and testing of a new drug being exceptions. That is by design, NIH deliberately leaves the downstream work to be done by the industry. This does not have to be the case. There is no intrinsic reason that later stage development and testing cannot also be supported by public funding, instead of government-granted patent monopolies, as was the case with the Moderna vaccine.

We are not about to switch from patent monopoly supported system to a publicly funded system overnight, but we can try to find situations where we can experiment with alternative funding mechanisms and compare the outcomes side by side.[1] We actually have a very good opportunity for such a test with Covid boosters.

Drs. Peter Hotez and Maria Elena Bottazzi, along with their colleagues at Baylor College of Medicine and Texas Children Hospital, developed a Covid vaccine, Corbevax. This vaccine has now been administered to well over 100 million people in India and Indonesia, protecting them against serious illness and death from Covid.

Corbevax was developed on an open-source model. This means that the process for producing the vaccine, as well as the data on safety and effectiveness, is entirely open and available to anyone. That means anyone in the world with the necessary manufacturing facilities can produce the vaccine. As a result, the vaccine is cheap, selling for around $2.50 a dose in India and Indonesia.

It would be desirable to have the Corbevax vaccine available in the United States. While it would likely cost somewhat more here, due to higher costs for labor and other items, we’re probably talking around $5 a shot. That compares to over $100 a shot for boosters of Moderna and Pfizer, by far the dominant vaccines in the U.S. (Most people don’t see this price tag, since insurers or the government are picking up much or all of the tab for the boosters, but we do ultimately pay this cost through one pocket or another.)

In addition to the far lower price tag, Corbevax also has the benefit of not being an mRNA vaccine. Instead, it uses a much older protein-based technology. Many of the people that still have not gotten a Covid vaccine are distrustful of mRNA technology. Whether or not these fears are well-grounded, they are keeping people from getting a vaccine which could protect them against Covid. At least some of these people may take advantage of the opportunity to get a vaccine that is not based on mRNA technology.

The FDA Obstacle

The reason that Corbevax is not available to people in the United States is that the Food and Drug Administration (FDA) will not allow it to be distributed here. The FDA is demanding that to get approved, the vaccine go through a full clinical trial to demonstrate its safety and effectiveness.

As it well knows, a full clinical trial at this point would be extremely difficult and expensive.[2] Since the overwhelming majority of people in the country have either already been vaccinated and/or been infected, it would be necessary to have an extremely large sample, likely hundreds of thousands of people, to demonstrate the effectiveness of Corbevax at this point. Note, this is entirely an issue of establishing effectiveness. At this point, there is little question that the vaccine is safe, with over a hundred million doses given and very few instances of adverse effects.

The alternative to a full clinical trial is a bridging study. This is designed to show that the Corbevax boosters give patients target levels of antibodies against the latest strain of Covid. This is the same process that Moderna and Pfizer go through when they have gotten their boosters approved. The FDA has resisted allowing Corbevax to be approved through this channel claiming that it is a fundamentally different technology.

That is true if the comparison is with the mRNA vaccines, but the FDA has given approval to a Novavax Covid vaccine, which uses a similar protein-based technology. (The Novavax vaccine is not widely available due to manufacturing problems.) There seems little downside in approving the Corbevax vaccine, if it can meet the FDA’s standards for determining effectiveness in a bridging study.

The FDA’s Stubborness Is a Big Deal

It would be great if a cheap non-mRNA booster were widely available. As noted before, some people resist getting the vaccine out of fear of the mRNA technology. This will give people a non-mRNA option. There are also people who have bad reactions to the mRNA vaccines (I am definitely in that category – knocks me out for at least a day), who would definitely prefer a non-mRNA option.

But the biggest issue here is the prevention of a serious test of alternatives to the patent monopoly system of financing drug and vaccine development. We pursue this route for developing drugs and vaccines because the pharmaceutical industry works hard to stifle any consideration of alternatives. This is a huge issue not only for public health but also as an economic matter.

As a public health matter, it is entirely this system of government-granted patent monopolies that creates the problem of expensive drugs. It is rare that a drug is actually expensive to produce and manufacture. Drugs are expensive because we give drug companies monopolies over an item that is essential for people’s health, or even their life.

To take a couple of recent examples, the retail price for Imatinib, a leukemia drug, is over $2,500 per prescription. The generic version sells for $13.40, less than one percent of the patent-protected price. The patent protected price for the prostate cancer drug Xtandi is $125 a capsule. A generic version is available at $7.50 a capsule or 6 percent of the patent-protected price.

The most dramatic case of patent monopolies being an obstacle to saving lives was in AIDS pandemic. Initially, the only treatment for AIDS was AZT, which slowed the advance of the disease, but did not cure it and generally lost effectiveness over time. In the early 1990s, the drug companies developed a triple cocktail of drugs that proved effective in keeping AIDS under control and allowing patients to live normal lives. They were selling it for around $15,000 a year.

That was expensive even in the United States, but it was a tab that insurers or the government could afford, even if most patients would have trouble paying it out of pocket. However, this sum was totally out of reach in Sub-Saharan Africa, where the per capita income for many countries was less than $1,000 a year. While the drug companies clearly incurred substantial expenses in developing the drugs, once they were developed, they were relatively cheap to produce.

This was proven when Cipla, a huge Indian generic manufacturer, agreed to make the drugs available at a cost of $1 a day. As a result, millions of lives were saved since this was a price that even low-income countries and international aid organizations could afford to pay.

Patent Monopolies on Prescription Drugs are a Huge Economic Issue

Even beyond their enormous health consequences, patent monopolies on drugs have enormous economic consequences. We will spend close to $650 billion this year on prescription drugs. We would likely be paying less than $100 billion if these drugs were sold in a free market without patent monopolies or related protections. The difference of more than $500 billion a year comes to almost $4,000 a year for an average family. It is more than half the size of the military budget. It is real money by almost any standard.

And, it goes into the pockets of the drug companies, making their top executives, their shareholders, and some highly employees very wealthy. This redistribution of income from the rest of us to a relatively small clique of people in the pharmaceutical industry has nothing to do with the free market. It is the result of a government policy on granting monopolies and related protections.

This massive upward redistribution could perhaps be justified if it were the only way to finance the sort of breakthroughs we have seen in recent decades that have radically and improved people’s lives. But as I have argued, there is good reason to think that we could pay for the development of new drugs and vaccines through alternative mechanisms.

That is why the FDA’s role in blocking Corbevax is such a big deal. This would be a very clear way to demonstrate to the public that we don’t need patent monopolies to provide incentives for developing new drugs and vaccines.

We could look to have direct funding to support the development of drugs and vaccines for other diseases, where the final product was also available on an open-source basis and sold as a cheap generic. The industry could continue with its patent-monopoly supported research, they would just have the risk that whatever they ended up developing may be competing with a generic that is every bit as good and selling for less than one percent of the price they want to charge.

This mechanism for funding would also remove the enormous incentive to lie that patent monopolies create. When drug companies can sell drugs at markups of many thousand percent, they have a powerful incentive to push their drugs as widely as possible, as was the case with the opioid crisis.

Also, we could finance research that is is not dependent on finding a patentable product. In many cases, nutrition or environmental factors may play an important role in health. As it is now structured, the pharmaceutical industry has no incentive to research this possibility, since they won’t stand to earn back their research costs by finding treatments along these lines.

Corbevax: A Foot in the Door

There is a huge amount at stake in a move away from the patent monopoly system of financing the development of prescription drugs. With all the problems of the current system, it has led to many important breakthroughs. If we are to go a different route, we need evidence that it can be equally effective.

The Corbevax vaccine provides one such example. If it were widely distributed and people could see the benefits, then we might be able to build the case for more support and experimentation in this direction. That sounds like a great path if the goal is to improve public health and reduce inequality. However, this likely sounds very bad from the perspective of the pharmaceutical industry, and apparently also the FDA.

[1] Two decades ago, Doctors Without Borders launched its Drugs for Neglected Diseases Initiative. Working on an open-source model, this project has developed thirteen treatments that have benefitted hundreds of millions of people, spending less than what the pharmaceutical industry claims it costs them to develop a single drug.

[2] There were clinical trials done in India to demonstrate the safety and effectiveness of Corbevax.

Read More Leer más Join the discussion Participa en la discusión

The New York Times did a classic “the economy is awful” story by highlighting the fact that 1.3 million homeowners might not be moving because of the large gap between current mortgage rates and the rate they would have to pay on a new mortgage. While this is clearly a problem, the flip side is that millions of people were able to refinance their mortgages at an extraordinarily low rate from the start of the pandemic in March 2020 until the Fed began raising rates in March of 2022.

According to the New York Fed, more than 14 million homeowners refinanced their homes in this period. This is saving these families thousands of dollars a year in interest payments. Perhaps I missed it, but I don’t recall seeing any pieces on how these homeowners are much better off today as a result of these savings. These savings are not picked up in our standard measures of income. Also, according to advanced economic theory, 14 million is a larger number than 1.3 million.

The piece also hugely exaggerated the likely duration of this sort of lock-in story telling readers:

“But today’s challenge may be more lasting. That’s because 30-year mortgage rates get locked in for, well, 30 years, and because rates below 3 percent are unlikely to be seen again anytime soon.”

The piece puts the current gap between the market rate for new mortgages and the rates on existing mortgages at 3.2 percent, with current mortgage rates around 6.7 percent. Part of the recent rise in mortgage rates is due to a run-up in interest rates on long-term Treasury bonds. The 10-year rate now stands close to 4.4 percent, as opposed to a bit less than 3.0 percent before the pandemic.

However, part of the run-up stems from an unusually large gap between mortgage rates and the interest rate on Treasury bonds. Usually this is around 1.75 percentage points. It currently is around 2.3 percentage points.

We are likely to see improvements on both fronts in the near future. The Fed is likely to lower interest rates at some point this year and Treasury yields will fall in anticipation of rate cuts. (The Treasury rate had been under 3.8 percent as recently as December.)

It is not entirely clear why the gap between mortgage rates and Treasury rates has widened so much, but it is reasonable to think that it will not persist indefinitely. If we see Treasury rates fall under 4.0 percent and the gap between mortgage rates and Treasury rates return to something like its long-term average, then it is very plausible that we will see mortgage rates below 6.0 percent in the not distant future.

That will still be higher than the 3.0 percent rate that many homeowners were able to lock in during the pandemic but would mean a considerably smaller gap than we now see. In any case, it is highly unlikely that anything like the current gap will persist for thirty years or anything close to it.

The New York Times did a classic “the economy is awful” story by highlighting the fact that 1.3 million homeowners might not be moving because of the large gap between current mortgage rates and the rate they would have to pay on a new mortgage. While this is clearly a problem, the flip side is that millions of people were able to refinance their mortgages at an extraordinarily low rate from the start of the pandemic in March 2020 until the Fed began raising rates in March of 2022.

According to the New York Fed, more than 14 million homeowners refinanced their homes in this period. This is saving these families thousands of dollars a year in interest payments. Perhaps I missed it, but I don’t recall seeing any pieces on how these homeowners are much better off today as a result of these savings. These savings are not picked up in our standard measures of income. Also, according to advanced economic theory, 14 million is a larger number than 1.3 million.

The piece also hugely exaggerated the likely duration of this sort of lock-in story telling readers:

“But today’s challenge may be more lasting. That’s because 30-year mortgage rates get locked in for, well, 30 years, and because rates below 3 percent are unlikely to be seen again anytime soon.”

The piece puts the current gap between the market rate for new mortgages and the rates on existing mortgages at 3.2 percent, with current mortgage rates around 6.7 percent. Part of the recent rise in mortgage rates is due to a run-up in interest rates on long-term Treasury bonds. The 10-year rate now stands close to 4.4 percent, as opposed to a bit less than 3.0 percent before the pandemic.

However, part of the run-up stems from an unusually large gap between mortgage rates and the interest rate on Treasury bonds. Usually this is around 1.75 percentage points. It currently is around 2.3 percentage points.

We are likely to see improvements on both fronts in the near future. The Fed is likely to lower interest rates at some point this year and Treasury yields will fall in anticipation of rate cuts. (The Treasury rate had been under 3.8 percent as recently as December.)

It is not entirely clear why the gap between mortgage rates and Treasury rates has widened so much, but it is reasonable to think that it will not persist indefinitely. If we see Treasury rates fall under 4.0 percent and the gap between mortgage rates and Treasury rates return to something like its long-term average, then it is very plausible that we will see mortgage rates below 6.0 percent in the not distant future.

That will still be higher than the 3.0 percent rate that many homeowners were able to lock in during the pandemic but would mean a considerably smaller gap than we now see. In any case, it is highly unlikely that anything like the current gap will persist for thirty years or anything close to it.

Read More Leer más Join the discussion Participa en la discusión

The higher than expected March CPI released on Wednesday freaked everyone out and got the markets convinced we will see fewer, if any, interest rate cuts this year. I have never been a Fed tea leaf reader, and am not about to change professions now, but it will be bad news if the Fed puts off rate cuts that can revitalize the housing market.

The big concern posed by the CPI, following higher-than-expected inflation numbers in January and February, is whether inflation is reaccelerating. We know that rental inflation is still high as an outcome of the surge in working from home at the start of the pandemic.

But we can be very confident that it will slow sharply over the course of the year due to the much slower inflation rate shown in indexes (including the BLS index) measuring rents in units that change hands. This means that rental inflation will not be an ongoing problem that the Fed has to worry about.

However, the recent data have shown an uptick in inflation, even pulling out rent. This is ostensibly the cause for concern.

There are two important points to be made about this uptick. First, it is not unusual to see large jumps, and falls, in CPI inflation excluding rent. Rent is a huge factor in the index, and since the pace of rental inflation changes slowly, it anchors the overall rate. Inflation is much more erratic when rent is excluded as shown below.

Note that there were many points at which inflation in the non-shelter CPI crossed 2.0 percent even in the low-inflation decade preceding the pandemic. In fact, year-over-year inflation in this index hit 2.1 percent in January of 2020, just before the pandemic started. It was at 2.5 percent in July of 2018. So a somewhat above-target reading for the non-shelter CPI should not be a major cause for concern by itself.

However, there is the question of whether the recent uptick reflects underlying trends. Here the story points in the opposite direction.

The day after the CPI report came out, we got a much more benign reading on the Producer Price Index (PPI). The overall figure for the month was 0.2 percent (0.154 to be more precise), with the core also at 0.2 percent. There are differences in coverage and methodology between the CPI and PPI, but inflation in the indexes still track each other closely.

The figure below shows the PPI for services, the PPI for goods, and the CPI.

What is perhaps most striking is how closely the CPI follows the PPI for services. That probably shouldn’t be surprising, since services account for almost two-thirds of the CPI. (It is important to note that the PPI does not include rent, so these are services minus rent.)

When the CPI goes substantially above or below the service component of the PPI it is following movements in the goods component. As can be seen the CPI has been well above the service component in the PPI since May of 2022. The cause here is the supply chain problems that sent goods inflation sky-rocketing a bit more than a year earlier.

The good news in this picture is that the goods component of the PPI has been far below the service CPI for a bit over a year, and for part of this period was even negative. This is just another way of showing the widely noted fact that the prices of supply chain goods have stabilized and in many cases are even falling. This looks likely to continue for the near-term future, especially if we don’t have a policy of blocking cheaper imports with higher tariffs as some presidential candidates are advocating.

The Wage Story

There is another part of the longer-term inflation picture that needs to be included, the slowing of wage growth. Our various wage indices show somewhat different figures for wage growth, but they tell basically the same story. Wage growth accelerated sharply as the economy reopened in the second half of 2020 and especially 2021 and 2022, as employers had to compete to hire and retain workers.

We saw record rates of quits, as workers left jobs that didn’t pay enough, offer advancement opportunities, had unsafe workplaces, or where the boss was a jerk. This is a great story, as workers saw gains in wages that outpaced inflation and workplace satisfaction hit a record high. The gains in wages were especially large for those at the bottom of the wage distribution.

While that is a very bright picture, we could not sustain nominal wage gains of the sort we were seeing in 2021 and the first half of 2022, and still hit the Fed’s 2.0 percent inflation target. Wage growth peaked at roughly 6.0 percent, 2.5 percentage points higher than the rates we were seeing before the pandemic.

To be clear, wages were not driving inflation. There was a shift from wages to profits at the start of the pandemic. It doesn’t make sense to say that wages are the cause of inflation when the profit share is increasing. But it is true that given current rates of productivity growth, we cannot have 6.0 percent wage growth and sustain anything close to a 2.0 percent rate of inflation. (FWIW, I am not a fan of the Fed’s 2.0 percent inflation target, but the Fed is.)

However, wage growth has slowed sharply over the last two years, getting close to its pre-pandemic pace. Again, there are differences by indices, but the pace of wage growth has fallen by roughly 2.0 percentage points, leaving it 0.5 percentage points above its pre-pandemic pace.

One index, the Indeed Wage Tracker, has fallen back to its 2019 rate of wage growth. This index is noteworthy because it measures wages in job postings for new hires. In this sense it can be thought of as being analogous to the new tenant rent indexes that measure the rents of units that turn over.

Just as most people don’t move every month, most people don’t change jobs every month, but we expect the rents of units that don’t turn over to roughly follow the rents of units that do change hands. In the same way, it is reasonable to think that wage patterns of workers who stay in their jobs will roughly follow wage patterns for newly hired workers. The Indeed Wage Tracker is telling us that wage growth has fallen back to a non-inflationary pace. This may take some time to show up in the other wage series, but we can be pretty confident of the direction of change.

Profit Shares and Productivity

There are two other reasons we can be reasonably confident inflation is now under control. The first is that the rise in profit shares at the start of the pandemic has not gone away. In fact, profit shares increased somewhat in the fourth quarter, indicating we are going in the wrong direction.

It is not clear why profit shares continue to rise, and not fall back towards pre-pandemic levels. (Yeah, corporations are greedy, but they have always been greedy.) The increase during the supply-chain crisis was understandable, companies have much more market power when supply is constrained. But unless conditions of competition were permanently altered by the pandemic, it’s hard to see why they would stay elevated, and we certainly should not expect them to continue to rise.

In any case, the rise in the profit share in the fourth quarter, suggests that a lower pace of inflation would be consistent with the wage growth we are now seeing, if the profit share were to remain stable. If the profit share were to fall back towards its pre-pandemic level (which was already well above its level at the start of the century), we could sustain considerably lower inflation with the current pace of wage growth.

In other words, there seems little basis for believing that the current rate of wage growth is inconsistent with the Fed’s 2.0 percent inflation target. In this respect, the Biden administration is on exactly the right track in going after abuses of market power that allow for higher margins, such as attempting to block the merger of the nation’s two largest supermarket chains, Albertson’s and Safeway. Similarly, cracking down on drug companies abusing their government-granted patent monopolies will also have the effect of reducing profit margins.

The other big wildcard in this story is productivity growth. Productivity growth soared in the last three quarters of 2023, averaging 3.7 percent over this period. Productivity growth is notoriously erratic and the data are subject to large revisions. We also have to note that growth was horrible in 2022, actually falling for the year. So, it is far too early to claim we are on a faster growth path. Nonetheless, the recent data are encouraging and it looks like we will have respectable numbers again for the first quarter, although not above 3.0 percent.

Given advances in AI and other technologies, it hardly seems absurd to think we may be seeing a productivity uptick. We are clearly at the very beginning of the uses of many of these technologies, so there will be many gains that we will see down the road.

If we can sustain a faster pace of productivity growth, then we can have faster nominal wage growth and still hit the Fed’s 2.0 percent inflation target. To be clear, I am not talking about a wildly rapid pace of growth, if we can just sustain a 2.0 percent rate, well below the rates we saw in the upturn from 1995 to 2005 and the long Golden Age from 1947 to 1973, then 4.0 percent wage growth would be consistent with 2.0 percent inflation, even after a period in which profit margins shrank somewhat.

Time to Declare Victory and Lower Rates

The long and short here is that it is really time for the Fed to declare victory in its war on inflation and start lowering interest rates. One problem that seems to be delaying rate cuts is that the economy remains strong, leaving Chair Powell and other Fed officials to talk about the situation as a one-sided choice. They see a risk of inflation if they lower rates too much or too soon, but there is little basis for concern about a recession or rising unemployment.

However, that leaves other negative effects of high interest rates out of the equation, most notably their impact on the housing market. The number of existing homes being sold in the last year is down by almost a third from its 2020-21 pace. This means that millions of people who would otherwise be looking to move are being kept in place by the Fed’s high interest rate policy.

Higher interest rates are also a drain on people’s budgets insofar as they have credit card debt or other forms of short-term debt. And it makes it more expensive to buy new or used cars. The rise in interest rates also creates stress on the financial system. This stress led to the failure of Silicon Valley Bank last year, along with several other smaller banks. With luck we won’t see another major round of bank failures this year, but higher rates unambiguously increase the risk.

In short, even if the economy does not need lower rates to sustain a healthy growth path right now, there is a real cost to keeping rates high. It’s time for the Fed to change course.

The higher than expected March CPI released on Wednesday freaked everyone out and got the markets convinced we will see fewer, if any, interest rate cuts this year. I have never been a Fed tea leaf reader, and am not about to change professions now, but it will be bad news if the Fed puts off rate cuts that can revitalize the housing market.

The big concern posed by the CPI, following higher-than-expected inflation numbers in January and February, is whether inflation is reaccelerating. We know that rental inflation is still high as an outcome of the surge in working from home at the start of the pandemic.

But we can be very confident that it will slow sharply over the course of the year due to the much slower inflation rate shown in indexes (including the BLS index) measuring rents in units that change hands. This means that rental inflation will not be an ongoing problem that the Fed has to worry about.

However, the recent data have shown an uptick in inflation, even pulling out rent. This is ostensibly the cause for concern.

There are two important points to be made about this uptick. First, it is not unusual to see large jumps, and falls, in CPI inflation excluding rent. Rent is a huge factor in the index, and since the pace of rental inflation changes slowly, it anchors the overall rate. Inflation is much more erratic when rent is excluded as shown below.

Note that there were many points at which inflation in the non-shelter CPI crossed 2.0 percent even in the low-inflation decade preceding the pandemic. In fact, year-over-year inflation in this index hit 2.1 percent in January of 2020, just before the pandemic started. It was at 2.5 percent in July of 2018. So a somewhat above-target reading for the non-shelter CPI should not be a major cause for concern by itself.

However, there is the question of whether the recent uptick reflects underlying trends. Here the story points in the opposite direction.

The day after the CPI report came out, we got a much more benign reading on the Producer Price Index (PPI). The overall figure for the month was 0.2 percent (0.154 to be more precise), with the core also at 0.2 percent. There are differences in coverage and methodology between the CPI and PPI, but inflation in the indexes still track each other closely.

The figure below shows the PPI for services, the PPI for goods, and the CPI.

What is perhaps most striking is how closely the CPI follows the PPI for services. That probably shouldn’t be surprising, since services account for almost two-thirds of the CPI. (It is important to note that the PPI does not include rent, so these are services minus rent.)

When the CPI goes substantially above or below the service component of the PPI it is following movements in the goods component. As can be seen the CPI has been well above the service component in the PPI since May of 2022. The cause here is the supply chain problems that sent goods inflation sky-rocketing a bit more than a year earlier.

The good news in this picture is that the goods component of the PPI has been far below the service CPI for a bit over a year, and for part of this period was even negative. This is just another way of showing the widely noted fact that the prices of supply chain goods have stabilized and in many cases are even falling. This looks likely to continue for the near-term future, especially if we don’t have a policy of blocking cheaper imports with higher tariffs as some presidential candidates are advocating.

The Wage Story

There is another part of the longer-term inflation picture that needs to be included, the slowing of wage growth. Our various wage indices show somewhat different figures for wage growth, but they tell basically the same story. Wage growth accelerated sharply as the economy reopened in the second half of 2020 and especially 2021 and 2022, as employers had to compete to hire and retain workers.

We saw record rates of quits, as workers left jobs that didn’t pay enough, offer advancement opportunities, had unsafe workplaces, or where the boss was a jerk. This is a great story, as workers saw gains in wages that outpaced inflation and workplace satisfaction hit a record high. The gains in wages were especially large for those at the bottom of the wage distribution.

While that is a very bright picture, we could not sustain nominal wage gains of the sort we were seeing in 2021 and the first half of 2022, and still hit the Fed’s 2.0 percent inflation target. Wage growth peaked at roughly 6.0 percent, 2.5 percentage points higher than the rates we were seeing before the pandemic.

To be clear, wages were not driving inflation. There was a shift from wages to profits at the start of the pandemic. It doesn’t make sense to say that wages are the cause of inflation when the profit share is increasing. But it is true that given current rates of productivity growth, we cannot have 6.0 percent wage growth and sustain anything close to a 2.0 percent rate of inflation. (FWIW, I am not a fan of the Fed’s 2.0 percent inflation target, but the Fed is.)

However, wage growth has slowed sharply over the last two years, getting close to its pre-pandemic pace. Again, there are differences by indices, but the pace of wage growth has fallen by roughly 2.0 percentage points, leaving it 0.5 percentage points above its pre-pandemic pace.

One index, the Indeed Wage Tracker, has fallen back to its 2019 rate of wage growth. This index is noteworthy because it measures wages in job postings for new hires. In this sense it can be thought of as being analogous to the new tenant rent indexes that measure the rents of units that turn over.

Just as most people don’t move every month, most people don’t change jobs every month, but we expect the rents of units that don’t turn over to roughly follow the rents of units that do change hands. In the same way, it is reasonable to think that wage patterns of workers who stay in their jobs will roughly follow wage patterns for newly hired workers. The Indeed Wage Tracker is telling us that wage growth has fallen back to a non-inflationary pace. This may take some time to show up in the other wage series, but we can be pretty confident of the direction of change.

Profit Shares and Productivity

There are two other reasons we can be reasonably confident inflation is now under control. The first is that the rise in profit shares at the start of the pandemic has not gone away. In fact, profit shares increased somewhat in the fourth quarter, indicating we are going in the wrong direction.

It is not clear why profit shares continue to rise, and not fall back towards pre-pandemic levels. (Yeah, corporations are greedy, but they have always been greedy.) The increase during the supply-chain crisis was understandable, companies have much more market power when supply is constrained. But unless conditions of competition were permanently altered by the pandemic, it’s hard to see why they would stay elevated, and we certainly should not expect them to continue to rise.

In any case, the rise in the profit share in the fourth quarter, suggests that a lower pace of inflation would be consistent with the wage growth we are now seeing, if the profit share were to remain stable. If the profit share were to fall back towards its pre-pandemic level (which was already well above its level at the start of the century), we could sustain considerably lower inflation with the current pace of wage growth.

In other words, there seems little basis for believing that the current rate of wage growth is inconsistent with the Fed’s 2.0 percent inflation target. In this respect, the Biden administration is on exactly the right track in going after abuses of market power that allow for higher margins, such as attempting to block the merger of the nation’s two largest supermarket chains, Albertson’s and Safeway. Similarly, cracking down on drug companies abusing their government-granted patent monopolies will also have the effect of reducing profit margins.

The other big wildcard in this story is productivity growth. Productivity growth soared in the last three quarters of 2023, averaging 3.7 percent over this period. Productivity growth is notoriously erratic and the data are subject to large revisions. We also have to note that growth was horrible in 2022, actually falling for the year. So, it is far too early to claim we are on a faster growth path. Nonetheless, the recent data are encouraging and it looks like we will have respectable numbers again for the first quarter, although not above 3.0 percent.

Given advances in AI and other technologies, it hardly seems absurd to think we may be seeing a productivity uptick. We are clearly at the very beginning of the uses of many of these technologies, so there will be many gains that we will see down the road.

If we can sustain a faster pace of productivity growth, then we can have faster nominal wage growth and still hit the Fed’s 2.0 percent inflation target. To be clear, I am not talking about a wildly rapid pace of growth, if we can just sustain a 2.0 percent rate, well below the rates we saw in the upturn from 1995 to 2005 and the long Golden Age from 1947 to 1973, then 4.0 percent wage growth would be consistent with 2.0 percent inflation, even after a period in which profit margins shrank somewhat.

Time to Declare Victory and Lower Rates

The long and short here is that it is really time for the Fed to declare victory in its war on inflation and start lowering interest rates. One problem that seems to be delaying rate cuts is that the economy remains strong, leaving Chair Powell and other Fed officials to talk about the situation as a one-sided choice. They see a risk of inflation if they lower rates too much or too soon, but there is little basis for concern about a recession or rising unemployment.

However, that leaves other negative effects of high interest rates out of the equation, most notably their impact on the housing market. The number of existing homes being sold in the last year is down by almost a third from its 2020-21 pace. This means that millions of people who would otherwise be looking to move are being kept in place by the Fed’s high interest rate policy.

Higher interest rates are also a drain on people’s budgets insofar as they have credit card debt or other forms of short-term debt. And it makes it more expensive to buy new or used cars. The rise in interest rates also creates stress on the financial system. This stress led to the failure of Silicon Valley Bank last year, along with several other smaller banks. With luck we won’t see another major round of bank failures this year, but higher rates unambiguously increase the risk.

In short, even if the economy does not need lower rates to sustain a healthy growth path right now, there is a real cost to keeping rates high. It’s time for the Fed to change course.

Read More Leer más Join the discussion Participa en la discusión

The inflation hawks took March’s CPI as cause for celebration, inflation may not be dead yet. There is no doubt that it was a disappointing report for those hoping we could put the pandemic inflation behind us, but there still is not much basis for thinking the Fed needs to get out the nukes and start shooting big-time.

The key point to remember is that this inflation continues to be driven overwhelmingly by rent. We know that rental inflation will be falling because we have data on marketed units, the ones that change hands, that show sharply lower rental inflation and in some cases, such as the BLS index for new tenants, actually deflation.

The CPI rental indexes will follow the index for new tenants, but with a lag. That lag is proving longer than had generally been expected, but there is no reason to question the basic logic. If people who change apartments are seeing lower rental inflation, it is pretty hard to tell a story where this doesn’t eventually show up in lower rental inflation for people who stay in the same unit.

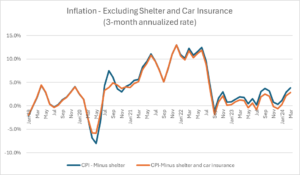

If we just look at the inflation rate excluding shelter, we have been skating close to, or even under, the Fed’s 2.0 percent target for most of 2023. The figure below shows annualized rates over the prior three months from 2019.

Source: Bureau of Labor Statistics and author’s calculations.

There definitely has been some acceleration in this measure in the last few months, but hardly an extraordinary one. We saw even larger upticks in inflation by this measure in the past, for example twice in 2019. Rent is typically a stabilizing factor in the overall inflation rate, precisely because the rate of rental inflation changes slowly.

There is another item that has played a big role in pushing inflation higher in recent years, auto insurance. The story is that premiums have risen sharply in recent years because of higher payouts in claims. (Profits have risen some as well, but we know payouts are most of the story from comparing the CPI measure which picks up gross payments, with the measure in the PCE deflator, which pulls out claims.)

Some of the story with premiums is higher costs due to higher prices for auto repairs, but much of it is simply more claims. Auto theft shot up in the pandemic but is now coming down. More long-term, people are seeing more damage due to climate-related events such as floods and hurricanes. That will be an ongoing problem.

To be clear, higher auto insurance premiums are a big deal in the sense that people have to bear these costs out of their pockets, however it is not part of a conventional inflation picture. The Fed will not be lowering auto insurance premiums by raising interest rates. The solution to climate-related damage is to try to limit climate change, but if that is off the agenda for political reasons, then people will just have to get used to higher-priced auto insurance, among other things.

Anyhow, if we pull auto insurance out of the story, in addition to rent, inflation was well below the Fed’s target for most of 2023 and actually negative at several points. We still get the acceleration in recent months to a 2.9 percent annualized rate as of March, but this hardly seems like something worth getting terribly excited over given the past behavior of this index.

In short, there is still plenty of reason for believing that the pandemic inflation is behind us. For now, the March report gave the inflation hawks some fresh meat, but a more careful look suggests that it doesn’t change the basic picture of inflation being largely under control.

The inflation hawks took March’s CPI as cause for celebration, inflation may not be dead yet. There is no doubt that it was a disappointing report for those hoping we could put the pandemic inflation behind us, but there still is not much basis for thinking the Fed needs to get out the nukes and start shooting big-time.

The key point to remember is that this inflation continues to be driven overwhelmingly by rent. We know that rental inflation will be falling because we have data on marketed units, the ones that change hands, that show sharply lower rental inflation and in some cases, such as the BLS index for new tenants, actually deflation.

The CPI rental indexes will follow the index for new tenants, but with a lag. That lag is proving longer than had generally been expected, but there is no reason to question the basic logic. If people who change apartments are seeing lower rental inflation, it is pretty hard to tell a story where this doesn’t eventually show up in lower rental inflation for people who stay in the same unit.

If we just look at the inflation rate excluding shelter, we have been skating close to, or even under, the Fed’s 2.0 percent target for most of 2023. The figure below shows annualized rates over the prior three months from 2019.

Source: Bureau of Labor Statistics and author’s calculations.

There definitely has been some acceleration in this measure in the last few months, but hardly an extraordinary one. We saw even larger upticks in inflation by this measure in the past, for example twice in 2019. Rent is typically a stabilizing factor in the overall inflation rate, precisely because the rate of rental inflation changes slowly.

There is another item that has played a big role in pushing inflation higher in recent years, auto insurance. The story is that premiums have risen sharply in recent years because of higher payouts in claims. (Profits have risen some as well, but we know payouts are most of the story from comparing the CPI measure which picks up gross payments, with the measure in the PCE deflator, which pulls out claims.)

Some of the story with premiums is higher costs due to higher prices for auto repairs, but much of it is simply more claims. Auto theft shot up in the pandemic but is now coming down. More long-term, people are seeing more damage due to climate-related events such as floods and hurricanes. That will be an ongoing problem.

To be clear, higher auto insurance premiums are a big deal in the sense that people have to bear these costs out of their pockets, however it is not part of a conventional inflation picture. The Fed will not be lowering auto insurance premiums by raising interest rates. The solution to climate-related damage is to try to limit climate change, but if that is off the agenda for political reasons, then people will just have to get used to higher-priced auto insurance, among other things.

Anyhow, if we pull auto insurance out of the story, in addition to rent, inflation was well below the Fed’s target for most of 2023 and actually negative at several points. We still get the acceleration in recent months to a 2.9 percent annualized rate as of March, but this hardly seems like something worth getting terribly excited over given the past behavior of this index.

In short, there is still plenty of reason for believing that the pandemic inflation is behind us. For now, the March report gave the inflation hawks some fresh meat, but a more careful look suggests that it doesn’t change the basic picture of inflation being largely under control.

Read More Leer más Join the discussion Participa en la discusión

It is a bit bizarre that the NYT decided to frame the March Consumer Price Index data as raising a question about the Fed’s ability to cut interest rates this year. The subhead is:

“The surprisingly stubborn reading raised doubts about when — and even whether — the Federal Reserve will be able to start cutting interest rates this year.”

The Fed can cut interest rates any time it wants. Higher inflation data, like the March report, make it less likely that it will choose to cut rates, but the Fed still clearly has the option to do so.

This distinction is important since people should realize that the Fed is making policy choices. It has to weigh the risk of inflation compared to the benefits of lower rates, most notably lower interest rates on mortgages and car loans.

People can agree that the Fed is making the right call if it decides to put off any rate cuts, but they should recognize that it is not forced to delay cuts. It has chosen to do so.

It is a bit bizarre that the NYT decided to frame the March Consumer Price Index data as raising a question about the Fed’s ability to cut interest rates this year. The subhead is:

“The surprisingly stubborn reading raised doubts about when — and even whether — the Federal Reserve will be able to start cutting interest rates this year.”

The Fed can cut interest rates any time it wants. Higher inflation data, like the March report, make it less likely that it will choose to cut rates, but the Fed still clearly has the option to do so.

This distinction is important since people should realize that the Fed is making policy choices. It has to weigh the risk of inflation compared to the benefits of lower rates, most notably lower interest rates on mortgages and car loans.

People can agree that the Fed is making the right call if it decides to put off any rate cuts, but they should recognize that it is not forced to delay cuts. It has chosen to do so.

Read More Leer más Join the discussion Participa en la discusión

The New York Times is apparently finding it difficult to be honest with its readers about the burden of student loan debt. It ran a major column telling readers that the burden of student loan debt is discouraging young people from becoming priests or nuns.

The whole premise of this column rests on a lie, that student debt should be a major burden to people interested in pursuing low-paying careers that might serve a higher purpose. The reason this is a lie is that income-driven repayment plan that President Biden put in place should allow people working in low-paying occupations to face little or no burden from their student debt.